")

If you’ve ever opened your banking app and wondered why your account shows two different numbers, you’re asking exactly the right question. The confusion around ledger balance meaning usually starts when the ledger balance looks healthy, but the available balance says something else. That mismatch can feel random at first, but it isn’t. It comes from the way banks process money in stages instead of treating every transaction as instantly final.

Once you understand the difference, managing your account balance gets much easier. More importantly, you’re less likely to spend based on the wrong number and trigger overdraft fees by mistake.

What Is a Ledger Balance? The Simplest Definition

What is a ledger balance? Ledger balance is the official balance in your account at the end of the previous business day, after all cleared transactions have been processed and posted. In plain English, it’s the bank’s settled record of where your account stood once the day’s finished transactions were officially entered into the books. That’s why the meaning of “ledger balance” is different from “how much money can I use right now?” It reflects posted activity, not every real-time movement still floating through the system today.

This is the key idea to remember: ledger balance is more like a historical snapshot than a live spending guide. It shows the account after completed credits and debits have cleared, but it doesn’t always capture what’s still pending right now.

So if you’re asking what ledger balance is because your banking app looks inconsistent, the answer is that ledger balance is usually the more static, official number, while other balance types are trying to reflect what’s happening at the moment.

Ledger Balance vs Available Balance: The Core Difference

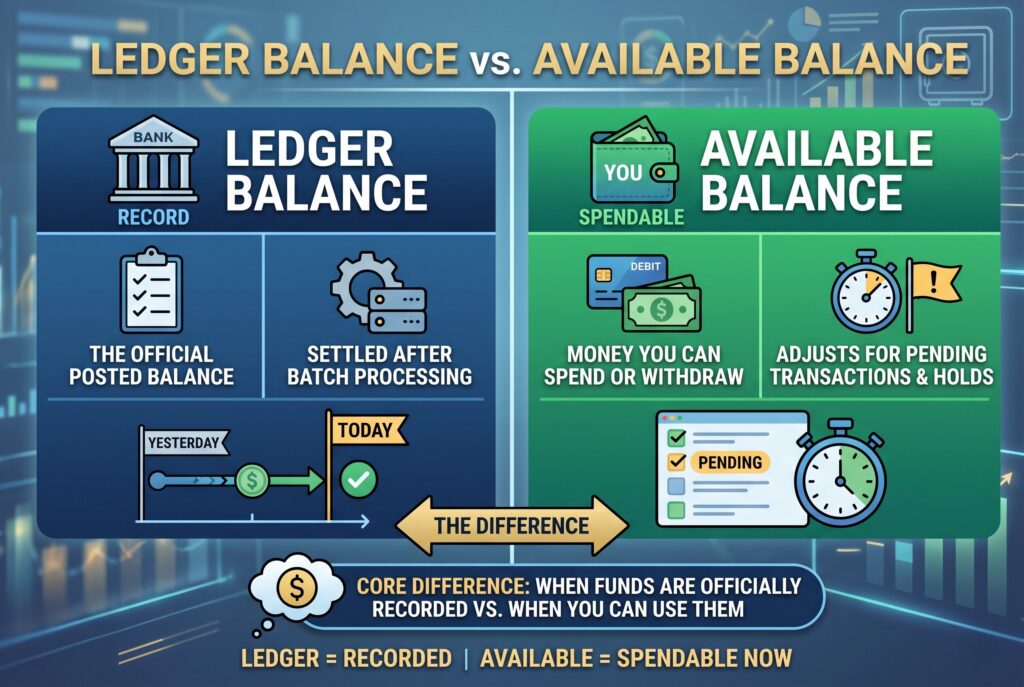

The fastest way to understand ledger balance vs available balance is to think of one number as settled and the other as spendable. Ledger balance is the official posted balance. It changes after the bank processes completed transactions in its batch cycle.

Available balance is the money you can actually withdraw, spend, or transfer right now. It adjusts more dynamically because it takes pending transactions, holds, and other short-term restrictions into account. That’s why these two numbers often don’t match.

A ledger balance may look higher because it hasn’t fully reflected a debit card hold yet. An available balance may look lower because the bank is already reserving money for pending activity. In everyday life, available balance is usually the number that matters more for spending decisions, while ledger balance is more about the bank’s official recordkeeping. So when people compare current balance vs available, they’re usually dealing with a similar confusion. But ledger balance adds another layer because it’s even more tied to posted transactions and prior-day processing.

Why Do These Two Numbers Often Not Match?

The gap between ledger balance and available balance usually comes down to timing. Banks don’t process everything instantly. Some transactions are authorized right away, but don’t settle until later. That delay creates the space where one number looks current and another looks restricted.

Pending Transactions

Pending transactions are one of the biggest reasons the numbers differ. If you use your debit card, the purchase may reduce your available balance immediately while the final posted transaction hasn’t hit your ledger balance yet. The money is effectively spoken for, but the official posting process isn’t finished.

Temporary Holds

Holds are another common reason. Hotels, gas stations, and car rental companies often place temporary holds that reduce your available balance before the exact final amount is settled. During that time, the ledger balance may still look stronger than the actual amount you can safely spend.

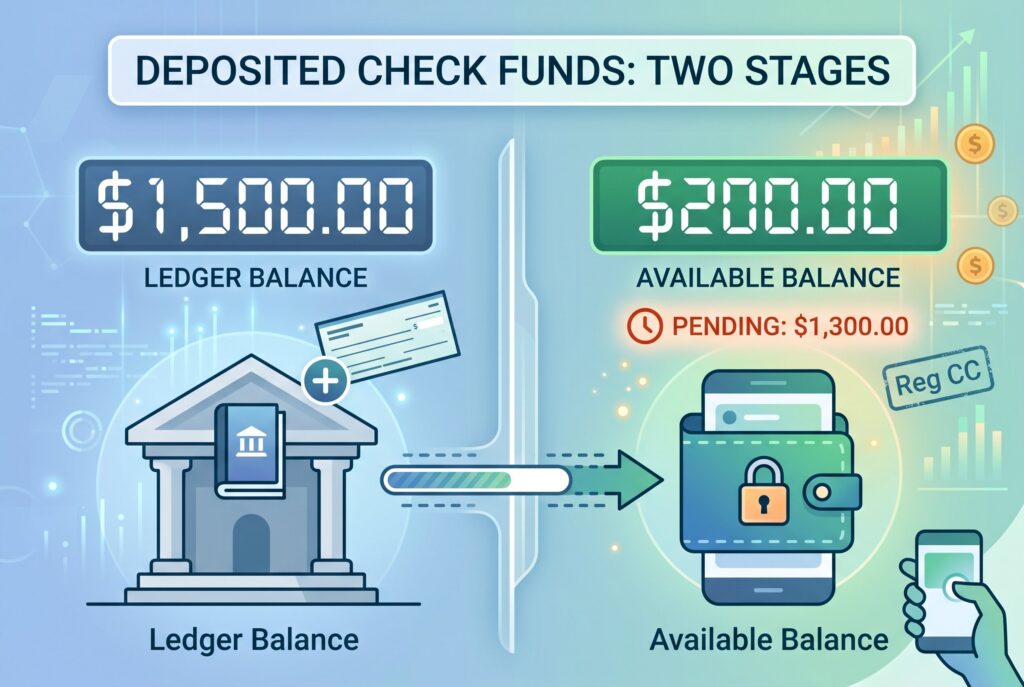

Check Deposits

Checks create another layer of confusion. A deposited check may appear in your ledger record before the full amount becomes available for immediate spending. Regulation CC affects this area, and banks may delay part of the funds until they’re more confident the check will clear. That means the ledger side and available side can temporarily tell two different stories about the same deposit. This is why people sometimes feel like the app is contradicting itself. It usually isn’t. It’s showing two different stages of the same money movement.

How to Calculate Ledger Balance

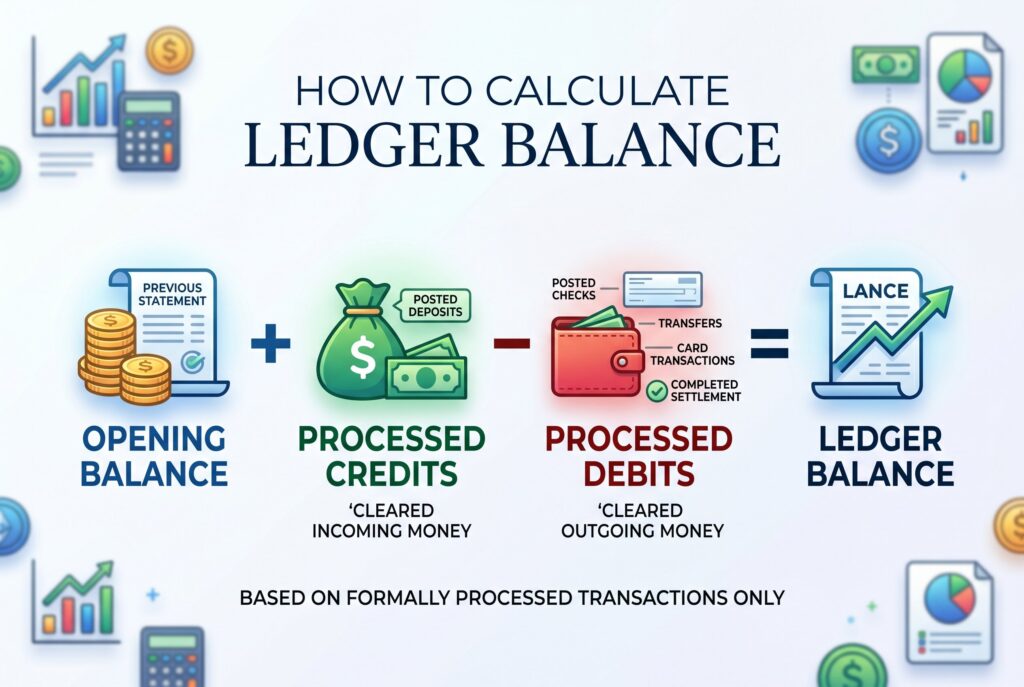

The basic ledger balance formula is simple: Ledger Balance = Opening Balance + Processed Credits − Processed Debits.

That formula matters because it shows how the bank is thinking about the account. The bank starts with the previous recorded balance. Then it adds cleared incoming money, such as posted deposits. Then it subtracts cleared outgoing money, such as posted checks, transfers, or card transactions that have completed settlement. What it doesn’t fully capture in real time are pending items that haven’t crossed the finish line yet.

This is one reason ledger balance feels more stable than available balance. It isn’t reacting to every authorization at the moment. It’s based on what has already been formally processed.

The Risk to Avoid: Overdraft Fees

This is where the topic becomes practical instead of theoretical. If you spend based only on ledger balance, you can trigger overdraft fees even when the ledger number still looks positive. That happens because available balance may already be lower once pending transactions or holds are accounted for.

This is sometimes called a technical overdraft problem. On paper, the settled number looks fine. But in real-time spending terms, the account may already be too tight. The safest rule is simple: use available balance as your day-to-day spending guide. Use ledger balance to understand what has officially been posted, but don’t rely on it alone when deciding whether you can safely make another purchase. That one habit can save a lot of frustration. Overdraft fees usually don’t happen because people can’t do math. They happen because the bank is tracking money in layers, and the customer is looking at the wrong layer.

Conclusion

Ledger represents the past, while Available reflects the present, that’s the simplest way to understand what a ledger balance means. Ledger balance shows the official posted record after cleared transactions. Available balance shows what you can safely use right now. Once you understand that difference, the app stops feeling inconsistent and starts making a lot more sense.

If you want to manage your money more safely, trust available balance for spending decisions, not just the ledger number. Setting low-balance alerts can help too. That way, you aren’t just watching your account balance. You’re managing it with the right lens.