A max funded IUL gets pitched as a tax free wealth strategy all over the internet, but most people still don’t understand what that phrase actually means. That’s the problem. A lot of buyers hear the upside first and the mechanics later. They hear about tax free loans, downside protection, and a growing IUL account, but they don’t hear enough about policy design, internal charges, and why this strategy only works in a narrow set of situations.

The truth is that a max funded IUL isn’t just a normal IUL policy with bigger premiums. It’s a specific design strategy. If it’s built correctly, it can shift an index universal life insurance policy away from pure death benefit focus and toward more efficient cash value accumulation. If it’s built badly, it can become an expensive and disappointing IUL investment that never lives up to the illustration.

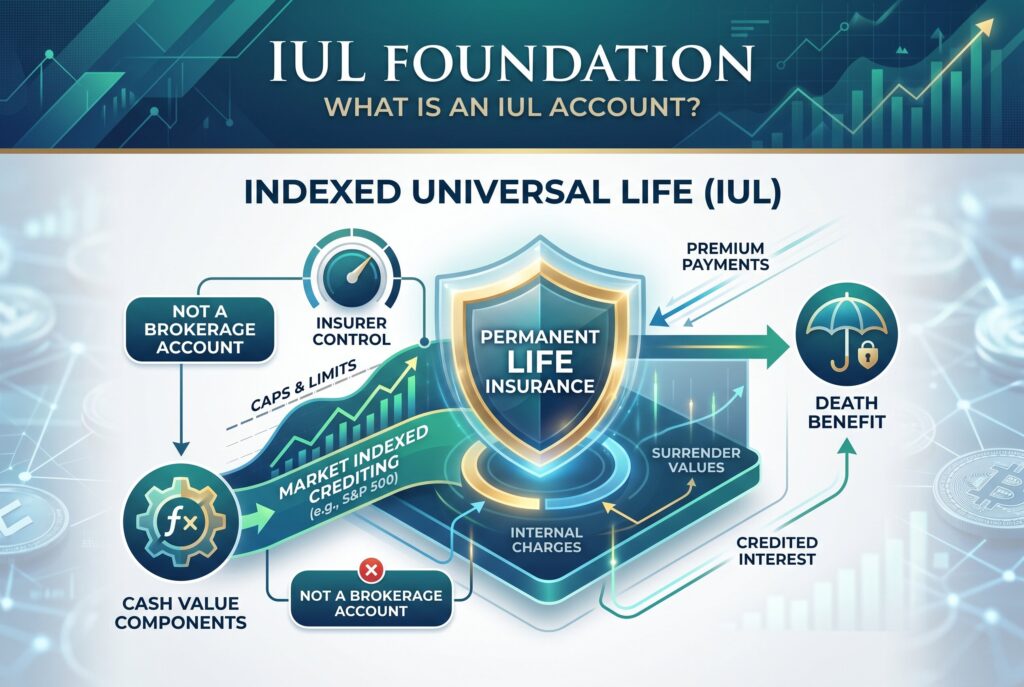

The Foundation: What Is an IUL Account?

Before getting into max funding, it helps to define what is an IUL in the first place. An indexed universal life policy is a form of permanent life insurance with cash value growth linked to a market index, such as the S and P 500, without directly investing the cash value in the stock market itself. That’s the core IUL meaning. It’s still life insurance first, not a brokerage account. The policy has a death benefit, internal insurance charges, and a cash value component that earns credited interest based on a formula tied to index performance.

That distinction matters because many people misunderstand the IUL account as though it were a direct stock market vehicle with a safety wrapper. It isn’t. The insurer controls key design features such as caps, participation rates, and other crediting mechanics. That means the growth potential is shaped by insurer rules, not just market performance. So when people search what is an IUL, the simplest honest answer is this: it’s a permanent life insurance policy with market linked crediting and cash value, not a standard investment account.

The Strategy: What Is a Max Funded IUL?

What is a max funded IUL? A max funded IUL is a policy designed so that the policyholder pays as much premium as possible under IRS rules while keeping the death benefit as low as legally allowed for the strategy. The goal is to minimize pure insurance drag and maximize the cash value side of the contract. In other words, instead of buying a life insurance policy and casually building some cash value around it, the owner is deliberately pushing the IUL policy toward cash accumulation efficiency.

This is where Section 7702 rules and MEC risk matter. If the contract is funded too aggressively without proper design, it can cross into modified endowment contract territory and lose the tax treatment buyers usually want. So max funding isn’t just “put as much in as possible.” It means funding up to the edge of the rules while keeping the structure compliant. That’s also why a max funded design and a standard design can behave very differently. A lightly funded policy tends to feel dominated by insurance costs. A max funded structure tries to overwhelm those costs with stronger premium support.

How It Works: The Mechanics of Tax Free Growth

This is the part that makes the strategy attractive. Inside a properly structured IUL insurance policy, cash value generally grows tax deferred. That means gains inside the contract aren’t taxed each year the way a taxable brokerage account might be. Then, if the policy stays in force and is handled properly, the owner may be able to access cash through policy loans in a tax advantaged way. That is why some people describe it as a life insurance retirement plan or a rich man’s Roth, even though that nickname can oversimplify what’s really happening.

The appeal is obvious. If the cash value compounds over time and the policy remains healthy, the owner can potentially borrow against the policy without triggering ordinary income tax the way a direct withdrawal from a traditional retirement account would. But that benefit comes with conditions. The policy has to be structured correctly, funded adequately, and maintained carefully. That’s the hidden catch behind the tax free wealth strategy language. The tax advantage is real only if the contract doesn’t lapse and the loan strategy doesn’t destabilize the policy later.

The Math: Gross Returns vs. Net Returns

This is where many articles get weak, because they talk about growth and ignore the friction. A max funded IUL may credit interest based on index performance, but the gross credited result isn’t the same as the net experience the owner actually gets. Internal costs, premium loads, and expense charges all play an important role, while the cost of insurance matters just as much, especially since it typically increases with age and adds more pressure over time.

This is why two policies that sound similar in a sales presentation can produce very different outcomes over time. The design determines whether the contract has enough cash value efficiency to overcome those internal costs. That’s also why the phrase max funded matters so much. It isn’t marketing fluff. It points to the main economic issue inside the product.

A standard funding design may leave too much of the early cash flow exposed to insurance drag. A max funded design tries to reduce that drag by making the death benefit as lean as possible and the cash accumulation as strong as possible. But even then, it still won’t behave like a pure investment account. It’s an insurance contract with investment-like features, not the other way around.

The Risks: When a Max Funded IUL Fails

This strategy can still fail, and that’s the part buyers need to understand before falling in love with the idea. If the market stays flat for a long stretch, the credited returns may be too modest to offset ongoing policy costs as comfortably as the original illustration implied. If the owner stops paying premiums too early, the contract may not have enough internal momentum to sustain itself. If too much is borrowed and the policy weakens, lapse risk becomes a serious danger. And if the policy lapses after years of tax deferred buildup and loans, the tax consequences can be brutal.

This is what separates a max funded IUL from a set it and forget it retirement account. It requires ongoing attention. It needs reviews. It needs realistic assumptions. It needs funding discipline.

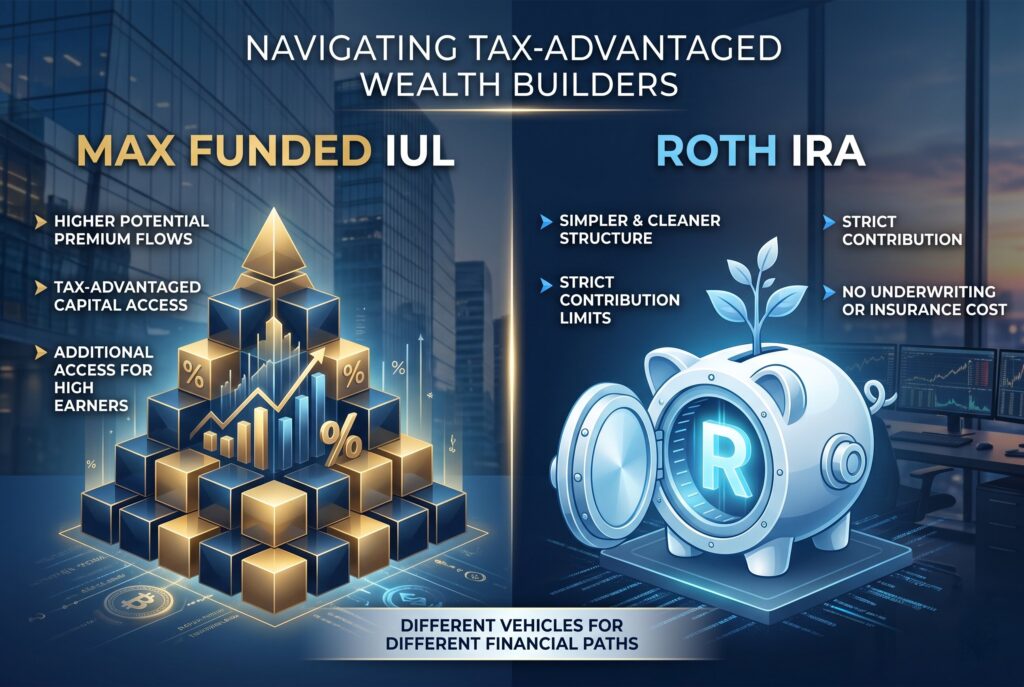

Max Funded IUL vs. Roth IRA

A Roth IRA is usually simpler, cleaner, and more transparent. It also has strict contribution limits and income restrictions. That’s where max funded IUL enters the conversation. For higher earners who have already used more straightforward tax advantaged vehicles well, an indexed universal life structure may offer another place to build tax advantaged access to capital.

But that doesn’t make it “better” in a universal sense. It makes it different. A Roth IRA doesn’t come with underwriting, rising insurance costs, or policy lapse risk. A max funded IUL can accept much larger premium flows, but it also comes with more complexity and more room for design mistakes.

Conclusion

A max funded IUL isn’t a beginner product and it isn’t a shortcut. It’s a specialized strategy that can make sense for high earners who have already maxed other tax advantaged accounts, want permanent life insurance, and can commit to funding and monitoring the policy properly.

For everyone else, especially those who still need simple retirement savings, liquidity, or low cost investing, it may be too complex and too easy to misuse. That’s the honest bottom line. A max-funded IUL can be powerful, but only when the design is tight, the assumptions are realistic, and the buyer understands that the real engine isn’t hype. It’s structure.