One small checkbox on a beneficiary form can completely change how your family’s money gets distributed. That’s why the difference between per stirpes vs per capita matters so much. Both terms decide who receives assets when a beneficiary dies before the person leaving the money behind, but they don’t lead to the same result. If you choose the wrong one, your family may end up with an outcome you never intended.

The good news is that the core difference is simpler than the Latin wording makes it sound. Per stirpes protects a family branch. Per capita rewards the surviving named beneficiaries. Once you understand that one distinction clearly, the rest of the decision gets much easier.

The Quick Answer: What Is the Core Difference?

The fastest way to understand per stirpes vs per capita is this: Per stirpes passes a deceased beneficiary’s share down to that person’s descendants. Per capita gives the money only to the surviving beneficiaries at the same level.

That means per stirpes is usually the more protective option if you want grandchildren or later descendants to stay included automatically. Per capita is usually better if you want the surviving named people to divide everything among themselves without preserving a deceased person’s branch.

So when people ask which one is better, the honest answer is that neither is universally better. The better choice depends on your goal. Do you want to protect bloodlines across generations, or do you want surviving beneficiaries to split the estate equally in the moment?

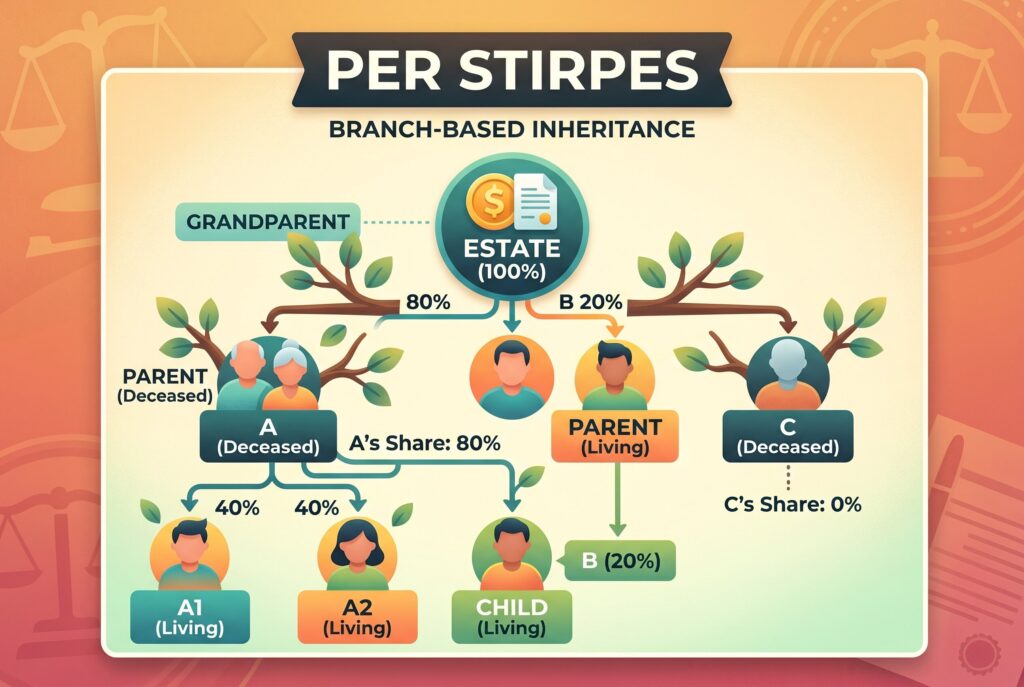

What Does Per Stirpes Mean? Protecting the Bloodline

Per stirpes meaning comes from Latin roots often translated as by branch, by roots, or by class. In plain English, it means that if a beneficiary dies before you do, that beneficiary’s descendants step into their place and inherit that share. That is the simplest per stirpes definition.

This is why per stirpes is often described as a way to protect the bloodline. The share doesn’t disappear just because one beneficiary is gone. Instead, it keeps moving down that branch of the family tree.

For example, if you leave assets to your three children and one of them dies before you, their children can inherit that share under a per stirpes arrangement. That makes it especially useful for people who want to be sure grandchildren aren’t accidentally cut out after a tragedy. This is also why the phrase what per stirpes means usually leads back to the same practical answer. It means the inheritance follows the family branch downward instead of stopping with the first named generation.

What Does Per Capita Mean? The Surviving Beneficiary Approach

Per capita means by the head. In inheritance terms, it means the estate is divided equally among the surviving beneficiaries at the same level. If one of those beneficiaries dies before you, that person’s share is absorbed by the remaining living beneficiaries rather than flowing automatically to that deceased person’s children. This is where the difference between per capita vs per stirpes becomes very real.

With per capita, the focus is on who is alive among the named beneficiaries when the distribution happens. It doesn’t automatically preserve a deceased person’s branch. That’s why grandchildren may receive nothing under a per capita structure unless they’re specifically named.

This doesn’t make per capita wrong. It just reflects a different intent. Some people want all surviving beneficiaries at the same generational level to share equally. If that is your real goal, per capita can be the better fit.

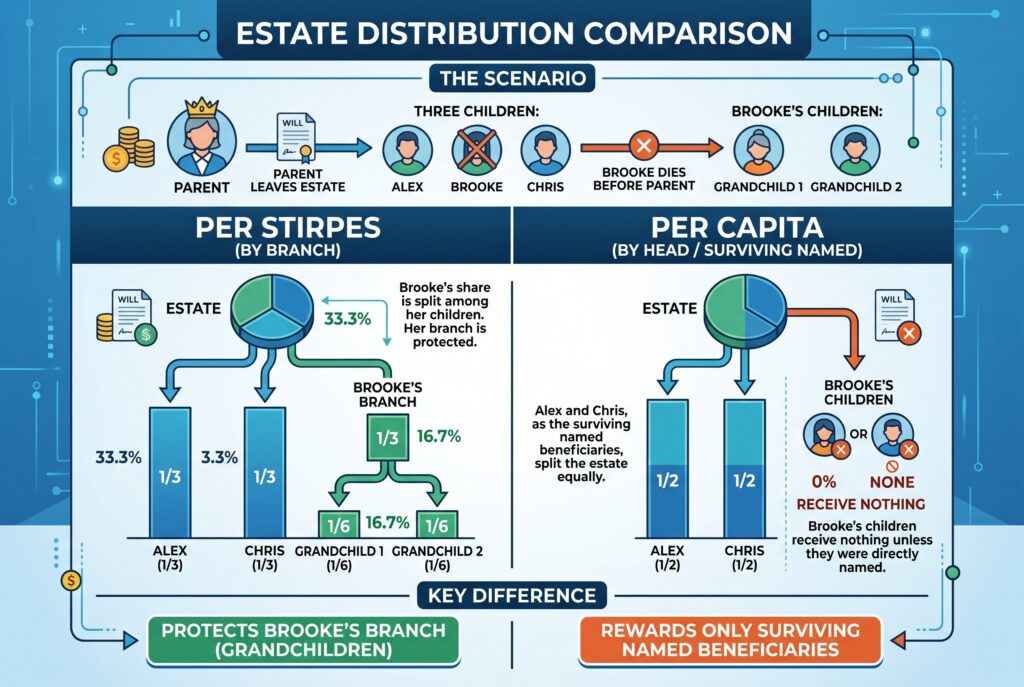

See the Math: A Simple Family Example

A real example makes the difference much easier to see. Imagine a parent leaves an estate to three children: Alex, Brooke, and Chris. Each child would normally receive one third. Now imagine Brooke dies before the parent, and Brooke has two children of her own.

Under per stirpes, Alex still receives one third, Chris still receives one third, and Brooke’s one third is split equally between Brooke’s two children. Each grandchild gets one sixth of the total estate.

Under per capita, Alex and Chris, as the surviving named beneficiaries, would usually split the estate equally between themselves. Brooke’s children would receive nothing unless they were directly named. That is the whole issue in one example. Per stirpes protects Brooke’s branch. Per capita rewards the surviving named beneficiaries only.

Beyond the Will: High Net Worth Beneficiary Designations

One of the most important practical points is that per stirpes and per capita also matter on beneficiary designations for non probate assets. That includes accounts and policies like brokerage accounts with transfer on death features, retirement plans such as 403(b)s, and life insurance or IUL policies. In many cases, the beneficiary form controls that asset even if your will says something different.

This is where a lot of families get surprised. They carefully update a will but forget an older beneficiary form sitting on a retirement account or insurance policy. Then the money moves according to the form, not according to what the family thought the will would accomplish. That’s why the choice between per stirpes vs per capita isn’t abstract legal theory. It’s a practical paperwork issue. The wording on those forms can override the broader story written elsewhere.

The Tax Traps of Generational Wealth Transfer

The inheritance mechanics may be simple, but the tax consequences can be more complicated depending on the type of asset.

For example, if a grandchild inherits part of a pre tax retirement account through a per stirpes designation, that beneficiary may be subject to withdrawal rules that create taxable income over time. The files specifically highlight the IRS 10 year rule concern for inherited retirement assets, which matters because a younger beneficiary could end up recognizing taxable distributions during peak earning years.

That doesn’t mean per stirpes is a bad choice. It means the transfer structure and the tax consequences are two separate questions. One determines who gets the money. The other determines how painful the tax treatment may be after they get it. That is especially important for higher net worth families with retirement accounts, insurance products, and multiple generations involved.

Conclusion

Per stirpes is usually the safer choice if your main goal is to make sure grandchildren or later descendants aren’t accidentally disinherited because one beneficiary dies early. It preserves the branch. Per capita is usually better if your real goal is equal distribution among the surviving named beneficiaries at the same level, without carrying a deceased person’s share down to that branch.

That is the simplest decision framework. If you care most about generational continuity, per stirpes often makes more sense. If you care most about equal treatment among living beneficiaries right now, per capita may fit better.

The most important thing isn’t to leave the choice to chance or assume the paperwork will work the way you “probably meant.” Review your beneficiary forms and estate documents carefully, because one unchecked box can reshape your family’s financial future.