A lot of people search for an IUL account expecting something that works like a bank savings product. That’s where the confusion starts. An IUL account sounds like a standalone account you open, fund, and watch grow like a traditional savings or investment balance. But that mental model isn’t accurate. An IUL account is really the cash value component inside an index universal life insurance policy. It lives inside a permanent life insurance contract, not inside a normal bank account.

That difference matters because it changes everything about how the money works, how growth is credited, how risks show up, and what tradeoffs you’re actually making. If you understand that one point clearly, the rest of the product becomes much easier to evaluate.

What Is an IUL Account? Beyond the Marketing Jargon

What is an IUL account? In plain English, an IUL account is the cash value portion of a permanent life insurance policy whose credited growth is linked to the performance of a market index. It isn’t a separate savings account, and it isn’t a brokerage account where your money is directly invested into stocks or mutual funds. It’s part of a life insurance contract. That’s the cleanest way to understand IUL meaning.

When people ask what is an IUL or what is an IUL account, the honest answer is that they’re talking about index universal life insurance, a policy that combines a death benefit with a cash value feature. The “account” language is convenient, but it can also be misleading because it makes the product sound simpler and more liquid than it really is.

This is also why an IUL account behaves very differently from a checking account, traditional savings account, or standard retirement plan. The policy has insurance charges, crediting rules, surrender schedules, and long-term design assumptions that ordinary deposit accounts don’t have.

How Does IUL Cash Value Actually Work?

The cash value inside an IUL grows through an index-crediting mechanism, not through direct stock ownership. That distinction is crucial. Your money isn’t being invested directly into the S and P 500 or another index. Instead, the insurer uses a formula that credits interest based on how a chosen index performs, subject to certain policy rules. The result is that the cash value may grow when the index performs well, but the owner doesn’t receive the raw market return the way a direct investor would.

This is what gives IUL growth potential its appeal and its limits at the same time. On the appealing side, the product is often marketed as offering some downside protection. On the limiting side, the policy owner gives up the full upside of direct market participation and takes on insurer-controlled crediting rules. That’s why cash value in an IUL should be understood as insurance-based accumulation, not direct investing.

This also explains why an IUL savings account is a risky phrase if taken literally. The product may be used as a long-term cash value vehicle, but it isn’t a savings account in the ordinary sense and it doesn’t offer the same kind of simplicity, guarantees, or deposit protection.

The Mechanics of Growth: Caps, Floors, and Participation Rates

These three features drive most of the economic reality of the policy.

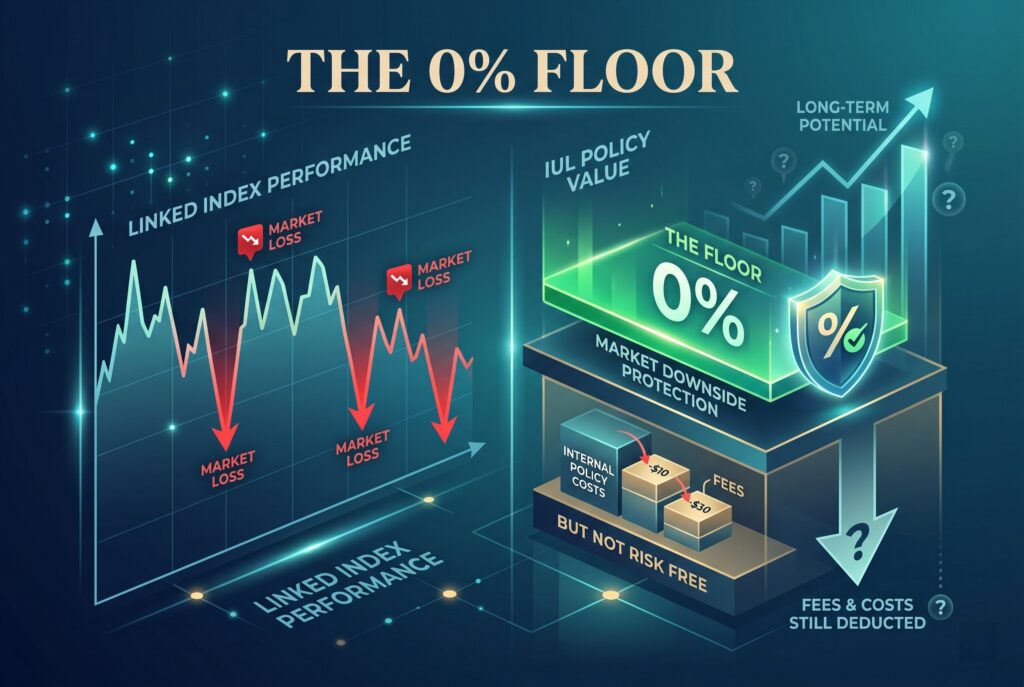

The 0% Floor

The floor is the downside protection feature. In many IUL designs, the credited rate won’t go below 0% when the linked index has a bad year. This is the part of the pitch many people find attractive because it suggests you don’t lose cash value due to direct market declines. But that doesn’t mean the policy is risk free. A 0% floor doesn’t erase internal policy costs, and it doesn’t guarantee strong long-term outcomes. It only limits the market-crediting downside inside the formula.

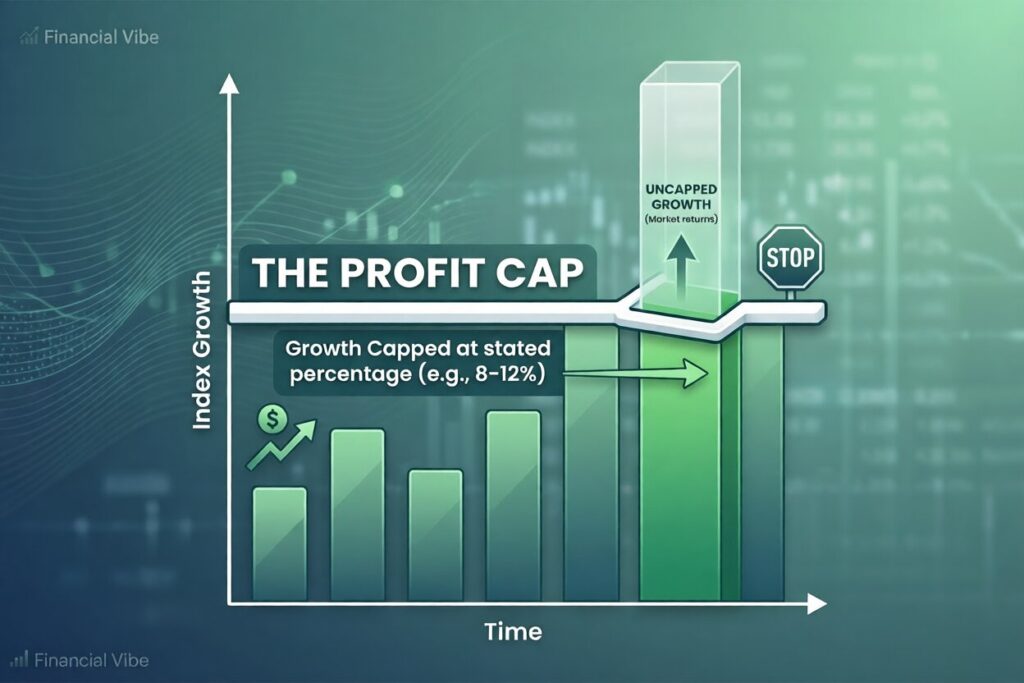

The Profit Cap

The cap is the ceiling on credited growth. If the linked index has a very strong year, your account may only receive growth up to the stated cap, often in a range such as 8% to 12% depending on product design and current insurer terms. This is a major reason IUL interest rates need to be understood carefully. A buyer may hear “market-linked growth” and picture direct equity compounding, but the cap prevents that outcome in strong years.

Participation Rate

The participation rate determines how much of the index movement your account is allowed to capture before the cap is applied. If participation is below 100%, you don’t even start from the full index return. You start from only a portion of it. Together, caps, floors, and participation rates define the real mechanics of IUL growth potential. They’re also why simple sales language often leaves out too much.

IUL Account vs. Traditional Savings: Which Is Better?

This comparison matters because the phrase IUL savings account naturally pushes people toward a savings-account mental model. A traditional savings account is simple. You deposit money, earn a stated rate, retain strong liquidity, and usually receive deposit insurance protection within legal limits. An IUL account doesn’t work like that. It’s a life insurance policy with a cash value feature, not a deposit product. It doesn’t offer FDIC-style bank protection, and the money inside the policy is subject to insurance costs, surrender charges, and long-term policy management issues.

So which is better depends on the purpose. If your goal is short-term liquidity, simplicity, and low-friction access to money, a traditional savings account is usually better. If your goal is long-term tax-deferred cash value accumulation inside a permanent insurance structure, and you fully understand the tradeoffs, an IUL may be relevant. But that’s a very different goal from ordinary saving. This is the core educational point many buyers miss: an IUL isn’t a bank alternative. It’s a long-horizon insurance strategy with a cash value component.

Key Risks and Considerations Before Opening an Account

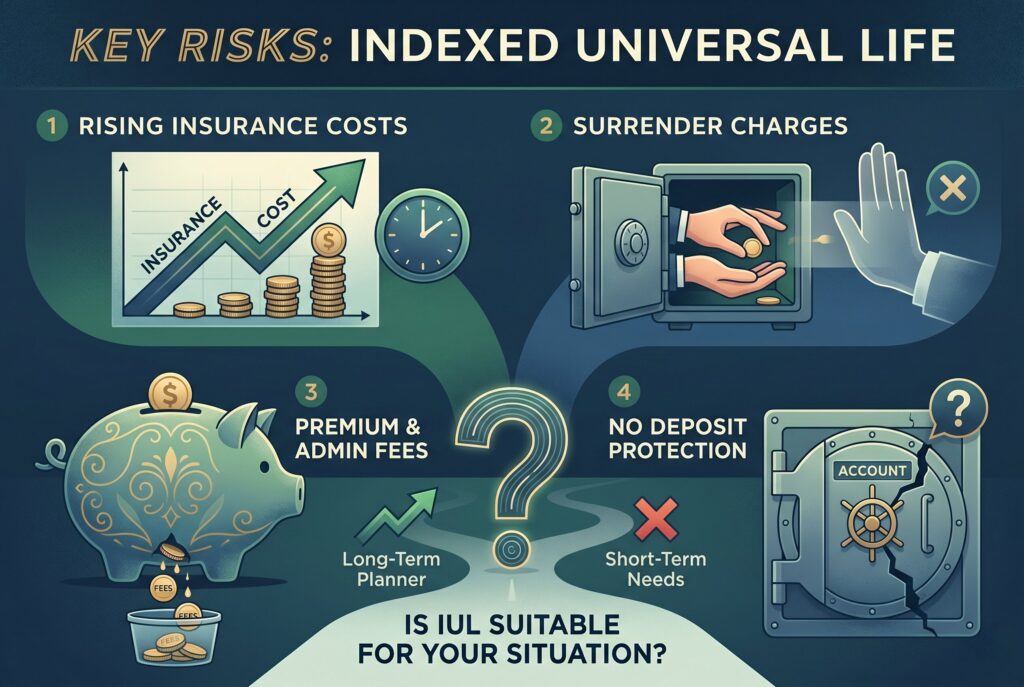

Before opening an IUL account, the biggest thing to understand is that the product can disappoint when people focus only on the growth story and ignore the cost structure.

Rising Cost of Insurance

One major issue is the rising cost of insurance over time. As the insured gets older, the internal insurance charges can increase, which places more pressure on policy performance.

Surrender Charges

Another issue is surrender charges. If you want out early, the cost of leaving can be painful.

Fees and Structural Misconceptions

Titan’s expat-focused analysis also highlights premium expense charges and makes the important point that this product lacks the deposit-style protection people often assume when they hear the word “account.”

Suitability and Strategic Fit

There is also the broader strategic issue of suitability. The product tends to make more sense for higher earners or long-term planners who have already used more straightforward retirement vehicles well and are looking for a specific kind of tax-deferred, insurance-based structure. It tends to make less sense for people who need short-term access, simpler products, or lower-cost accumulation tools. This is why opening the account isn’t really the hard part. Understanding whether you should open it’s the real decision.

Conclusion

An IUL account isn’t really an account in the everyday sense. It’s the cash value engine inside an index universal life insurance contract. That means the product should be judged as insurance-based accumulation, not as a normal savings product and not as a direct market investment.

For the right person, especially someone with a long time horizon, higher income, and a clear reason for using permanent life insurance alongside cash value growth, it may have a role. For the wrong person, it can be an expensive and misunderstood product that never feels as flexible or straightforward as expected. That’s the key takeaway. If you’re evaluating an IUL account, don’t ask only how the growth works. Ask what the policy really is, what the cash value is costing you, and whether the structure fits your broader financial strategy.