")

If you’ve been pitched indexed universal life on social media or by a high-energy agent, you’ve probably heard the same story. They call it a tax-free wealth strategy, a rich person’s Roth, or a secret retirement hack that lets you avoid market crashes while still growing your money. That’s exactly why so many people search why IUL is a bad investment after the sales pitch wears off. The product sounds simple at first, but the fine print is where the real story begins.

The truth is that IUL meaning gets distorted all the time. An IUL account isn’t a normal investment account. It’s an insurance contract first. If it’s sold carelessly, underfunded, or compared unfairly to stock market investing, it can become one of the most disappointing financial products a buyer ever owns. That doesn’t mean every indexed universal life policy is automatically terrible. It means the structure matters, the funding matters, and the sales framing matters even more.

The Big Lie: Is an IUL Account Actually an Investment?

What is an IUL? An indexed universal life policy is a form of permanent life insurance with cash value that grows based on a formula tied to a market index. But the policy doesn’t directly invest your money in the market. That distinction is crucial. The insurer credits interest using an index method, while the contract itself remains a life insurance product with a death benefit, internal charges, and complex moving parts.

That’s why calling an IUL account an investment in the same way you’d describe a brokerage account, Roth IRA, or 401(k) is misleading. The primary engine inside the contract is still insurance. The cash value component matters, but it operates inside a product designed around mortality costs, policy expenses, and insurer-controlled crediting rules.

So before getting into the criticism, that’s the reality check. Indexed universal life isn’t just a market-growth tool with a nice wrapper. It’s a permanent insurance chassis with a market-linked crediting formula attached.

10 Reasons Why IUL Is a Bad Investment If Sold Incorrectly

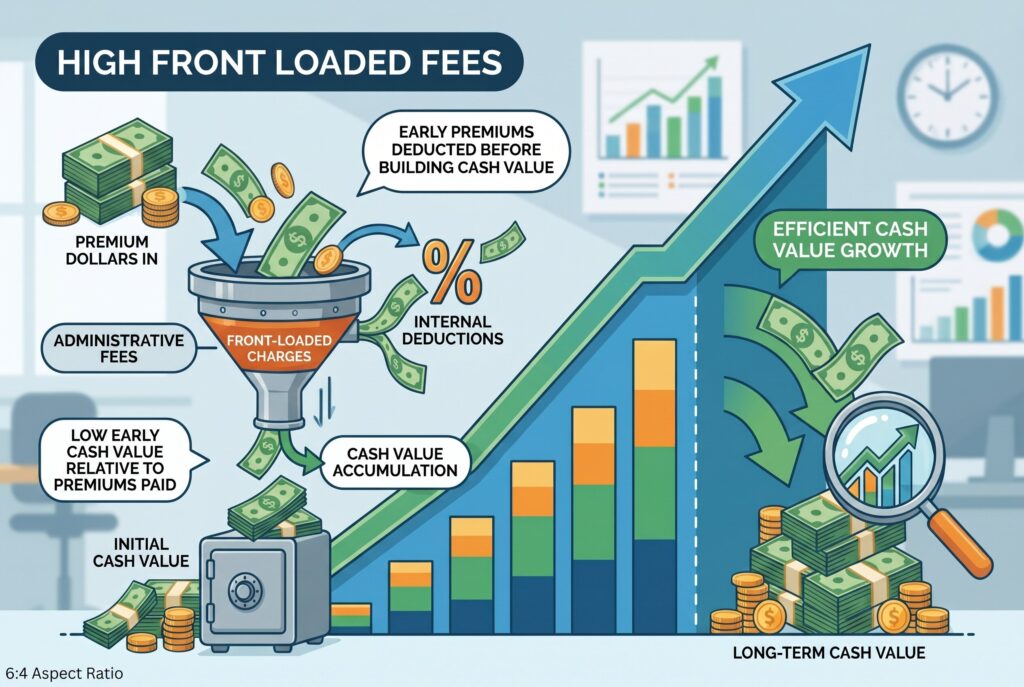

1. High Front Loaded Fees

The first problem is cost drag, especially early on. In many policies, premium dollars don’t flow cleanly into cash value right away. Charges, administrative expenses, and other internal deductions can eat up early contributions before the policy begins to feel efficient. This is one reason buyers are often shocked when the early cash value looks far lower than the amount they paid in.

2. The Cost of Insurance Rises As You Age

The internal cost of insurance doesn’t stay flat forever. As the insured person gets older, the cost of keeping that death benefit in force generally rises. If the policy’s growth underperforms or the funding level is too weak, those rising costs can begin draining the cash value in a way buyers didn’t expect. This is one of the biggest hidden dangers in poorly structured IULs.

3. Surrender Charges Can Trap Your Money

A lot of people don’t realize how expensive it can be to exit early. Surrender charges may last many years, which means the policyholder can’t easily get out without taking a painful hit. So even if you realize the contract wasn’t a good fit, your money may feel trapped right when you most want flexibility.

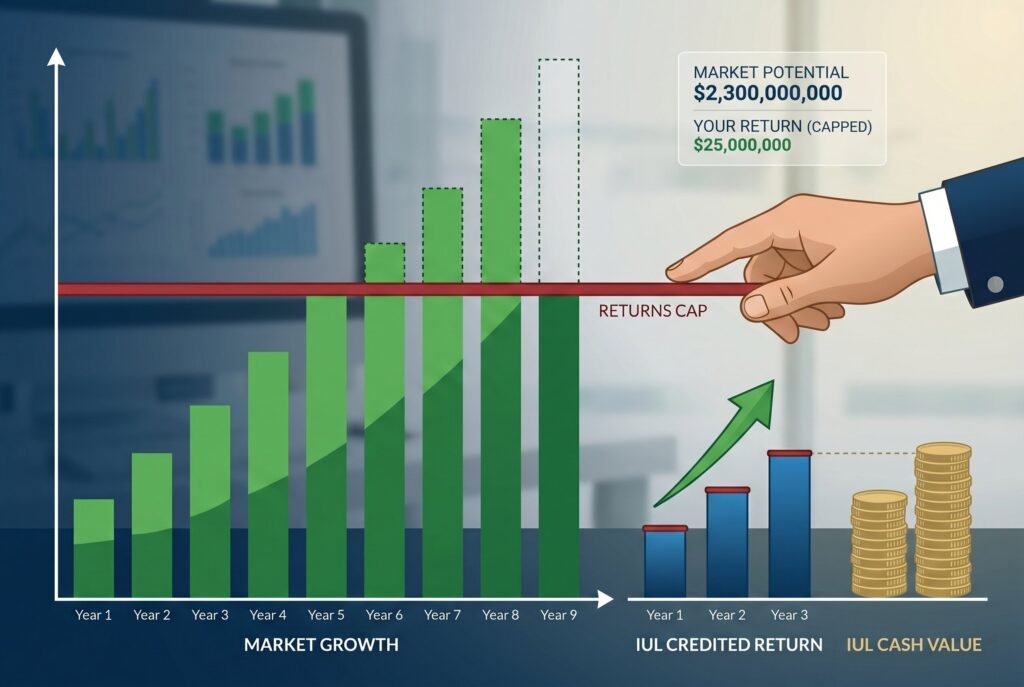

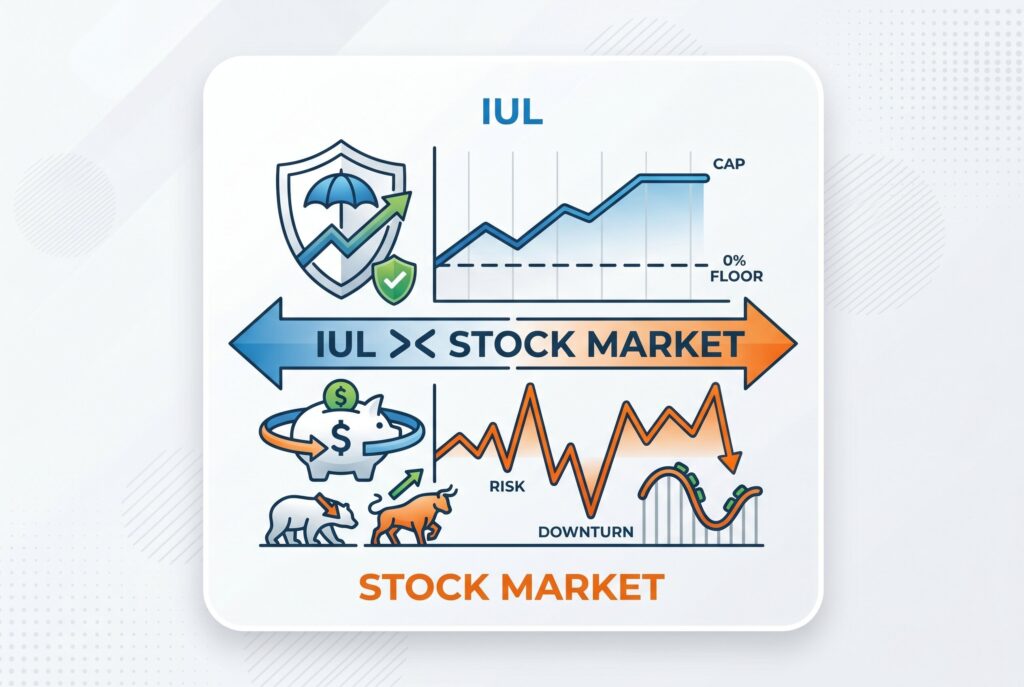

4. Caps Limit the Upside

This is one of the easiest ways the sales pitch goes off the rails. Agents often talk about market-linked growth, but they don’t emphasize that the upside is limited. If the market has a very strong year, your credited return may still be capped well below that. So if the index rises sharply, your IUL cash value may capture only part of the gain. That changes the compounding story dramatically over time.

5. The 0% Floor Still Has a Cost

The floor sounds comforting because it’s usually framed as “you can’t lose when the market is down.” But the floor doesn’t mean you get full market economics without downside. You’re giving up things too, especially uncapped upside and the dividend component of stock market returns. Over long periods, that tradeoff matters more than many buyers realize.

6. Participation Rates and Caps Can Change

Many people assume the rules they see in the illustration are permanent. They usually aren’t. Participation rates, caps, and other index-crediting features can change over time within the policy’s terms. That means the insurer has control over key growth levers after you buy the contract. Even if the policy looks good at issue, future performance can become less favorable if those crediting terms tighten.

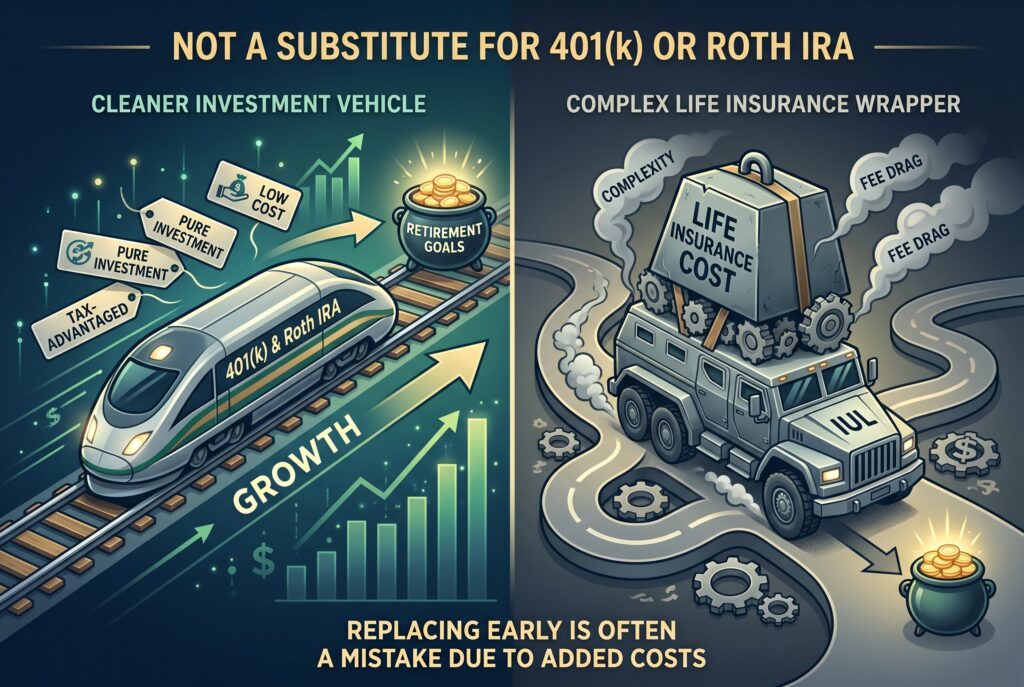

7. It Doesn’t Replace a 401(k) or Roth IRA

This is where a lot of bad advice enters the conversation. IUL is often marketed as a superior alternative to traditional retirement accounts, but that comparison usually ignores the obvious. Standard retirement accounts don’t come with life insurance costs. They’re cleaner vehicles for pure investing. For most people, replacing a 401(k), IRA, or Roth strategy with IUL too early is a mistake. The insurance wrapper adds complexity and drag that simple tax-advantaged investing doesn’t.

8. Agent Illustrations Can Be Too Optimistic

Illustrations are one of the most dangerous parts of the sale. A projected return stream can make the policy look smooth and powerful over decades, but those numbers depend on assumptions that may not hold. When the illustration leans too optimistic, buyers end up expecting cash value performance that real policies may never deliver. This is one reason skepticism around indexed universal life has grown so much.

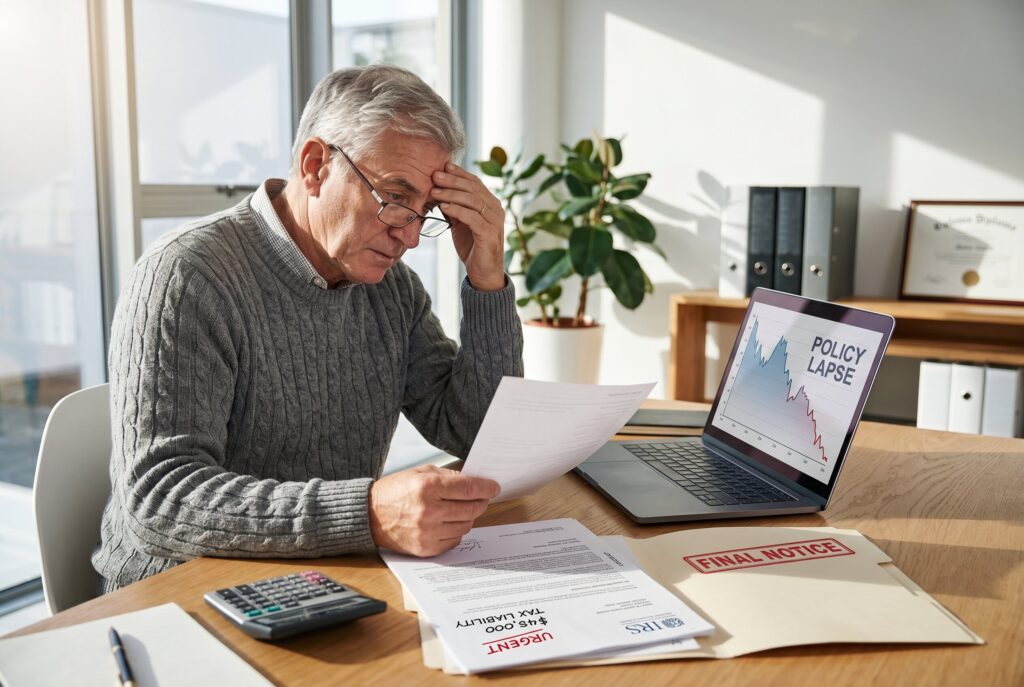

9. Policy Lapse Risk Can Create a Tax Disaster

This is one of the least understood but most painful risks. If the policy is poorly funded, heavily borrowed against, or weakened by years of mediocre performance and rising insurance costs, it can lapse. When that happens after large policy loans or years of tax-deferred buildup, the tax consequences can be ugly. This isn’t a small footnote. It’s a serious structural risk.

10. Complexity Makes It Easy to Mismanage

Unlike a low-cost index fund or straightforward term policy, an IUL requires active attention. It needs reviews, ongoing funding awareness, and a realistic understanding of policy mechanics. Complexity alone isn’t always bad, but complexity plus aggressive sales framing is a dangerous combination. A product this opaque is easy to misunderstand and easy to own badly.

See the Math: IUL vs the Stock Market

The most important comparison isn’t emotional. It’s mathematical. When you compare IUL with the stock market directly, the problem usually comes from asymmetry. In strong years, caps limit how much upside you get. In weak years, the floor helps, but fees and insurance costs still exist. Over long periods, that can produce a much different compounding path than simply owning low-cost equity investments directly. That’s the heart of why IUL is a bad investment for many people who were expecting stock-like growth with none of the downside. That doesn’t mean the floor has no value. It means the buyer has to be honest about what they’re giving up in exchange for it.

The Plot Twist: When Is an IUL Actually Good?

This is where the conversation gets more nuanced. An IUL can be much better when it’s structured as a max funded IUL rather than a minimally funded one. What is a max funded IUL? It usually means pushing premiums as high as possible within IRS limits so the policy has more cash value efficiency and relatively less insurance drag. In that design, the owner is trying to minimize the damage from internal costs and maximize the long-term utility of the tax-advantaged cash bucket.

This is why some people still defend indexed universal life. If it’s overfunded properly, used by a high-income person who has already maxed more straightforward tax-advantaged accounts, and treated as a specialized supplemental bucket rather than a stock-market replacement, it can make sense. That’s a much narrower use case than the social media pitch suggests.

Conclusion

For many people, the honest answer is no. If you’re still building your financial base, carrying expensive debt, or haven’t used simpler retirement vehicles well, IUL is usually not the place to start. It’s too complex, too expensive, and too easy to buy for the wrong reasons.

But for a smaller group, especially high earners or advanced planners who understand the design tradeoffs and fund the policy aggressively, a max funded IUL can sometimes serve as a niche tool. Even then, it should be approached with caution, stress-tested assumptions, and no illusions about what it really is.

That’s the final point. Indexed universal life isn’t automatically evil, and it isn’t automatically smart. It’s bad when it’s sold as something it isn’t. It gets better only when the buyer understands the costs, the limits, and the role it should actually play.