on W-2 Meaning: Are Employer Pick Up Contributions Taxable?")

If you’ve noticed 414(h) on W-2 paperwork and had no idea what it meant, you aren’t alone. Box 14 is one of the most confusing parts of the form, especially for public employees. The good news is that employer pick up contributions usually mean you’re getting a current tax advantage, not a surprise tax problem. In simple terms, the money is being treated as if your employer paid it into your retirement plan for tax purposes, even though it’s still coming out of your paycheck.

That’s why this code matters. It often lowers your federal taxable wages today while helping you build retirement savings for later. But there’s one important catch. Federal treatment and state treatment don’t always match, and that’s where many taxpayers get tripped up.

What Does 414(h) Mean on Your W-2 (Box 14)?

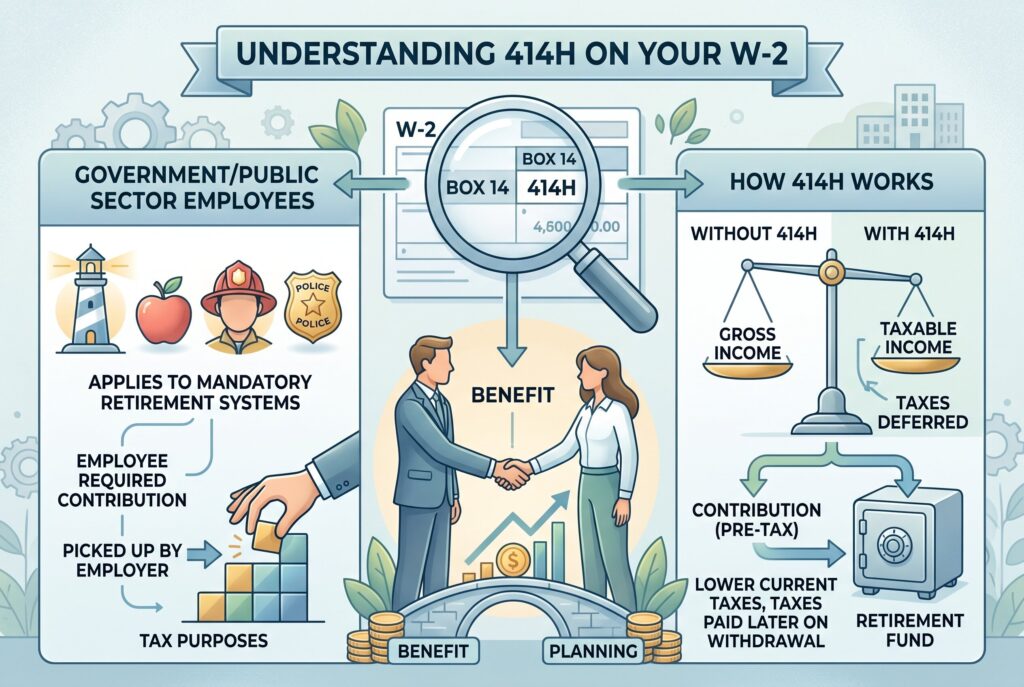

What is 414(h) on W-2? Section 414(h) is an IRS rule that applies mainly to government and public-sector retirement systems. If you see W-2 box 14 414(h), it usually means your required retirement contributions were “picked up” by your employer for tax purposes. That doesn’t mean the employer gave you extra money out of nowhere. It means the contribution is being treated differently under the tax rules than a normal after-tax payroll deduction.

This setup is common for teachers, police officers, firefighters, state workers, municipal employees, and other government workers who participate in public retirement systems. In many of these plans, the employee doesn’t have the same kind of optional salary deferral choice you might see in a 401(k). Instead, the contribution is mandatory, and the employer formally “picks up” the amount under the tax code. That’s why 414(h) on W-2 is closely tied to employer pick up contributions. The code signals a retirement contribution arrangement, not random extra income or a separate taxable fringe benefit.

Are 414(h) Contributions Taxable? The Pre Tax Advantage

This is the question most people really care about. Are 414(h) contributions taxable? At the federal level, the answer is usually no for current income tax purposes. A 414(h) retirement plan contribution is generally treated as pre-tax for federal income tax. That means you don’t pay federal income tax on that money in the year it goes into the plan. Instead, the tax is deferred until you withdraw the money in retirement.

That’s why people often ask is 414(h) pre tax. In most normal public employee situations, yes, it functions as a pre-tax benefit for federal income tax. But that doesn’t mean every tax layer works the same way. The IRS draws a difference between federal income tax treatment and some payroll tax issues, and state tax treatment can differ too. For ordinary taxpayers, the most important practical point is this: your Box 1 wages on the W-2 are often already reduced by these picked-up contributions for federal purposes, which means you’re seeing the tax benefit now.

The State Tax Catch

This is where things become less intuitive. Some states may still tax these contributions in the year they’re made, even while federal income tax is deferred. New York is one of the clearest examples people run into during filing season. In some public employee situations, the 414(h) amount gets added back on the state return even though it was excluded from federal taxable wages. So the cleanest way to think about it is this: federally deferred doesn’t always mean state deferred. That’s why public employees should pay close attention to their own state rules instead of assuming the federal result applies everywhere.

See Your Savings: How 414(h) Lowers Your Box 1 Wages

One of the most practical ways to understand 414(h) is to look at Box 1 on your W-2. Box 1 shows your federal taxable wages, not your gross pay before every deduction. If your retirement contributions qualify as employer pick up contributions under 414(h), those amounts are usually already excluded from Box 1 for federal income tax purposes. That means the number in Box 1 is lower than it otherwise would have been, which reduces your current federal taxable income.

Here’s the simple logic. Imagine you earned $70,000 in salary and contributed $4,000 through a qualifying 414(h) arrangement. Your Box 1 wages may be closer to $66,000 instead of the full $70,000 for federal income tax purposes. You didn’t lose the money. It went into retirement savings. But you also didn’t pay federal income tax on that $4,000 this year. That’s the immediate benefit of a 414(h) retirement plan arrangement. It reduces taxable income now and pushes the tax event into the future, when distributions are taken.

414(h) vs. 401(k) and 403(b): What Is the Difference?

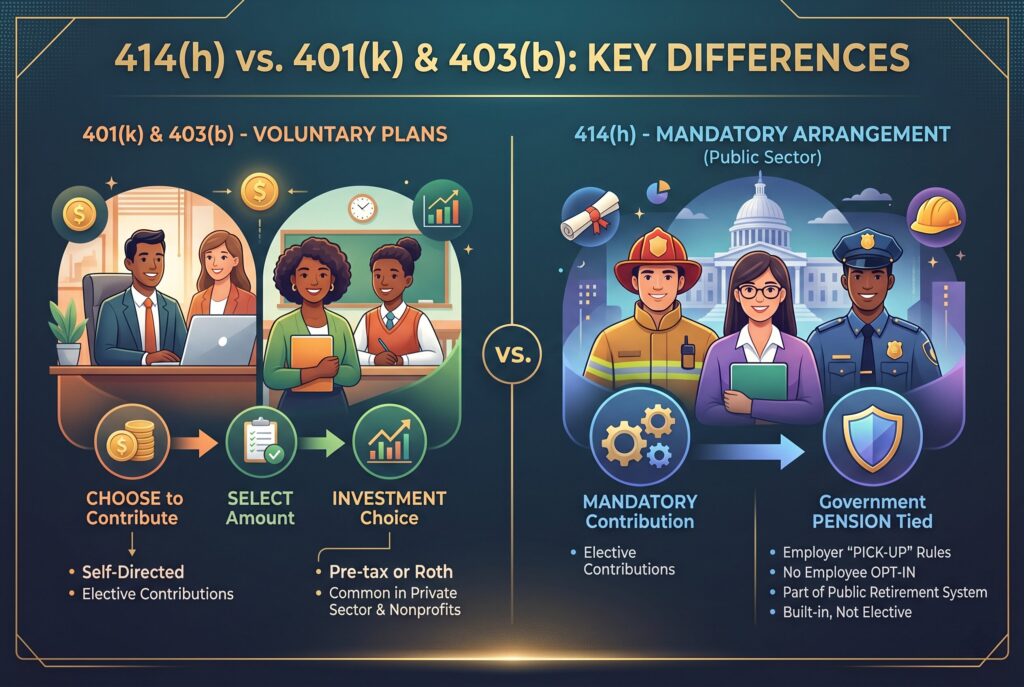

A lot of people assume 414(h) is just another version of a 401(k), but that isn’t quite right. A 401(k) is typically a voluntary retirement plan. You choose whether to contribute, how much to contribute, and sometimes whether to use traditional pre-tax or Roth after-tax treatment. A 403(b) works similarly for many nonprofit and school employees.

A 414(h) arrangement is different because it is often tied to a government pension system and is usually mandatory rather than voluntary. That’s one of the biggest differences in the 414(h) vs 401(k) comparison. In many cases, the employee doesn’t opt in and doesn’t choose a contribution percentage the way a private-sector worker might with a 401(k). The contribution is built into the public retirement system and handled through employer pick up rules.

So while all of these plans relate to retirement savings, they don’t operate the same way. A 414(h) is usually more closely tied to a pension-style public employment structure than to the self-directed elective model most people associate with a 401(k).

How to Report 414(h) on Your Tax Return (Form 1040)

For most federal filers, the actual tax filing step is easier than the W-2 box makes it seem. If you’re using common tax software, the safest approach is to enter the W-2 exactly as shown, including the Box 14 description and amount. Because the 414(h) amount is generally already excluded from Box 1 wages for federal income tax purposes, you usually don’t take a separate federal deduction for it on Form 1040. In other words, the federal benefit has already been baked into the wage number the software uses.

Where things get more complicated is state filing. If your state requires an addback, you may need to enter the Box 14 code correctly so the state software handles it the right way. This is one reason some taxpayers get confused. They assume the Box 14 amount means they need to manually subtract something on the federal return, when in reality the opposite issue often shows up at the state level. So the best practical rule is simple. Enter the W-2 exactly as it appears, then pay close attention to any state-specific prompts in your tax software.

Conclusion

Seeing 414(h) on W-2 forms can look intimidating, but in most cases it points to a useful public employee benefit rather than a problem. The code usually means your retirement contributions are being handled as employers pick up contributions, which generally reduces your federal taxable income now and defers taxation until retirement withdrawals begin.

The most important takeaway is this: 414(h) is usually good for your current federal tax bill, but state treatment may be different. That’s why it’s smart to review your own state rules carefully, especially if you work in a state known to add these amounts back for state income tax purposes. If your return feels unclear, a CPA or knowledgeable tax preparer can help make sure your public pension benefits are being reported correctly.

Related Articles

414(h) vs 403(b): Which Government Retirement Plan Is Better?