If you’re researching an indexed universal life policy in 2026, you’re probably looking for more than a basic definition. You want to know whether this is actually a smart long-term financial tool or just a product that sounds better in a sales pitch than it performs in real life. That’s exactly why understanding indexed universal life matters. It sits at the intersection of permanent life insurance, cash value accumulation, and market-linked crediting, which makes it appealing but also easy to misunderstand.

The truth is that an IUL isn’t a magic wealth solution, and it also isn’t automatically a bad idea. It’s a specialized tool. When it’s designed properly and funded carefully, it can be powerful. When it’s underfunded, misunderstood, or sold with unrealistic expectations, it can disappoint badly. That’s why the real question isn’t whether index universal life insurance is good or bad in the abstract. It’s whether it fits your financial situation, risk tolerance, and long-term cash flow.

What Is an IUL? Understanding the Basics of Indexed Universal Life

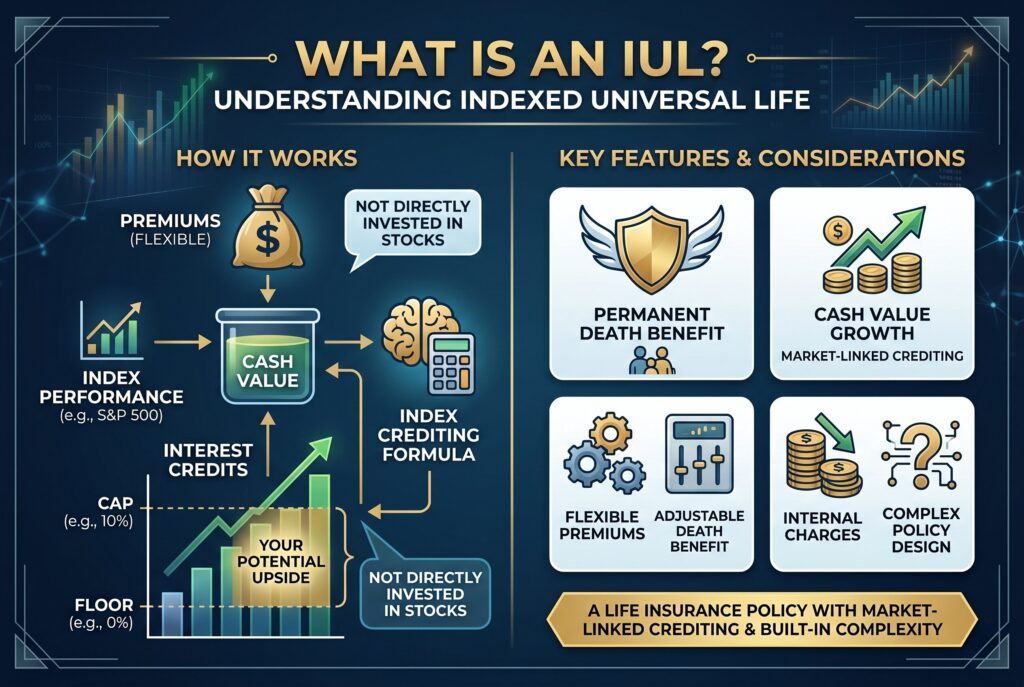

What is an IUL? IUL meaning, in simple terms, is a permanent life insurance policy with cash value growth tied to the performance of a market index, such as the S&P 500, without directly investing your cash value in the stock market itself. That distinction matters. The policy credits interest based on an index formula, but your money isn’t sitting inside index funds the way it would in a brokerage or retirement account.

This is what makes index universal life insurance so attractive to many buyers. It combines a death benefit, flexible premiums, and a cash value component with some upside exposure to index performance. But that upside comes with limits, and the product’s real-world performance depends heavily on design, funding, and internal charges. So if you’ve been asking what is an IUL or what is indexed universal life, the most accurate short answer is this: it’s a permanent life insurance policy with market-linked crediting and built-in complexity.

How an IUL Works: Floor, Cap, and Participation Rate

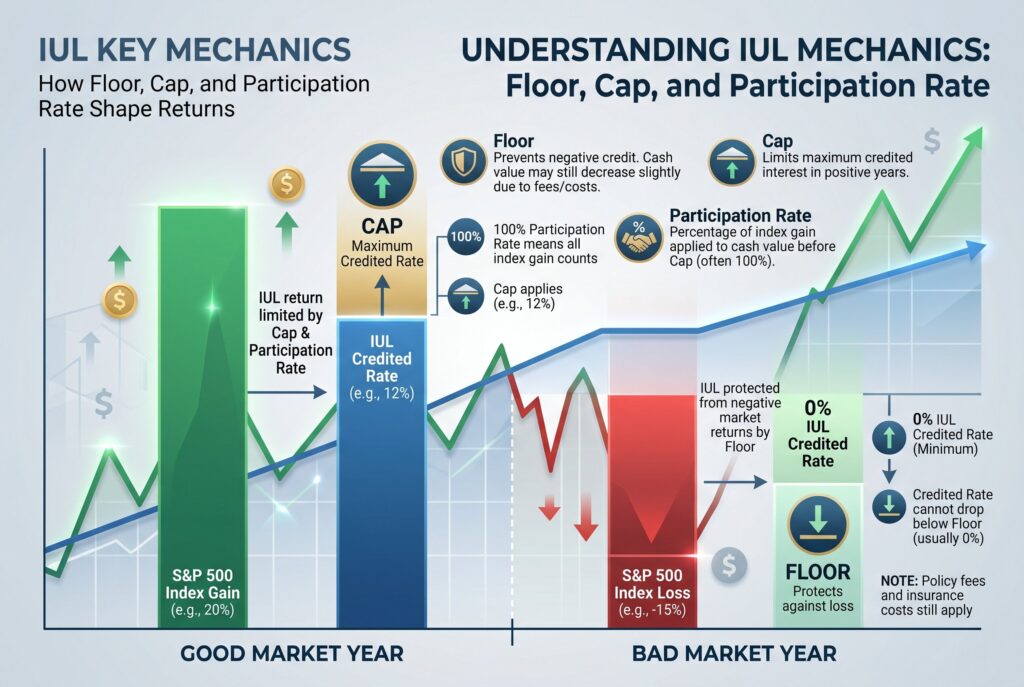

The Floor: Downside Protection

This is where IUL gets more technical, but these mechanics are the whole story. The floor is the protection feature. In many policies, the credited rate won’t drop below 0% in a bad market year. That doesn’t mean the policy has no risk. It means the index-crediting formula may prevent a negative credit from the market side. The policy can still lose ground in practical terms once fees and insurance costs are taken into account.

The Cap: Upside Limitation

The cap is the ceiling on how much upside you can receive. If the index rises sharply, the insurer may only credit you up to the cap. So even if the market performs extremely well, your IUL account doesn’t receive all of that growth.

The Participation Rate: Share of Gains

The participation rate is the percentage of the index gain your policy is allowed to capture before the cap is applied. If the participation rate is less than 100%, you only receive part of the index’s gain.

How These Features Work Together

These three features shape the policy’s cash value behavior. They are also the reason an IUL account can feel safer than direct market investing on the downside, while still being less powerful than direct investing on the upside. That tradeoff is the product’s core design.

The Max Funded IUL Strategy: How People Try to Optimize It

A max funded IUL is one of the most searched IUL topics for a reason. It reflects a strategy, not just a policy type. What is a max funded IUL? It usually means designing the policy so that you put in as much premium as possible within IRS rules without crossing into Modified Endowment Contract territory. The goal is to minimize the relative drag of insurance costs and maximize cash value growth potential.

This matters because many poorly designed IUL policies fail for a simple reason: not enough money goes in relative to the costs. A max funded structure tries to solve that. Instead of treating the policy like a lightly funded death benefit contract, the owner leans harder into the cash value side. That doesn’t make it risk free. It just makes it more efficient. The idea is that if someone is going to use IUL as a long-term accumulation tool, the policy usually needs stronger funding discipline from the start.

The Hard Truth: Why Many People Say IUL Is a Bad Investment

This is the skepticism section, and it matters. Why IUL is a bad investment is a common search because many people encounter these products after hearing optimistic claims about tax-free income, market upside, and downside protection. The problem is that those claims can sound cleaner than the reality.

Cost Complexity

One major issue is cost. IULs come with multiple layers of charges, including insurance costs, administrative fees, and other internal deductions. These costs often increase as you age, which can put pressure on the policy, especially if growth underperforms or the policy isn’t sufficiently funded.

Illustration Risk

Another concern is illustration risk. Buyers may rely too heavily on hypothetical projections without fully understanding that future performance is not guaranteed. Caps and participation rates can change over time, and extended periods of modest returns can make the policy perform far below initial expectations.

That’s also why people search for 10 reasons why IUL is a bad investment. The skepticism usually comes from some combination of high fees, unrealistic sales illustrations, lapse risk, loan misuse, or the realization that simpler strategies might have fit better. The fairest summary is this: IUL can be a bad investment when it’s sold as an investment substitute instead of what it really is, an insurance product with complex cash value mechanics.

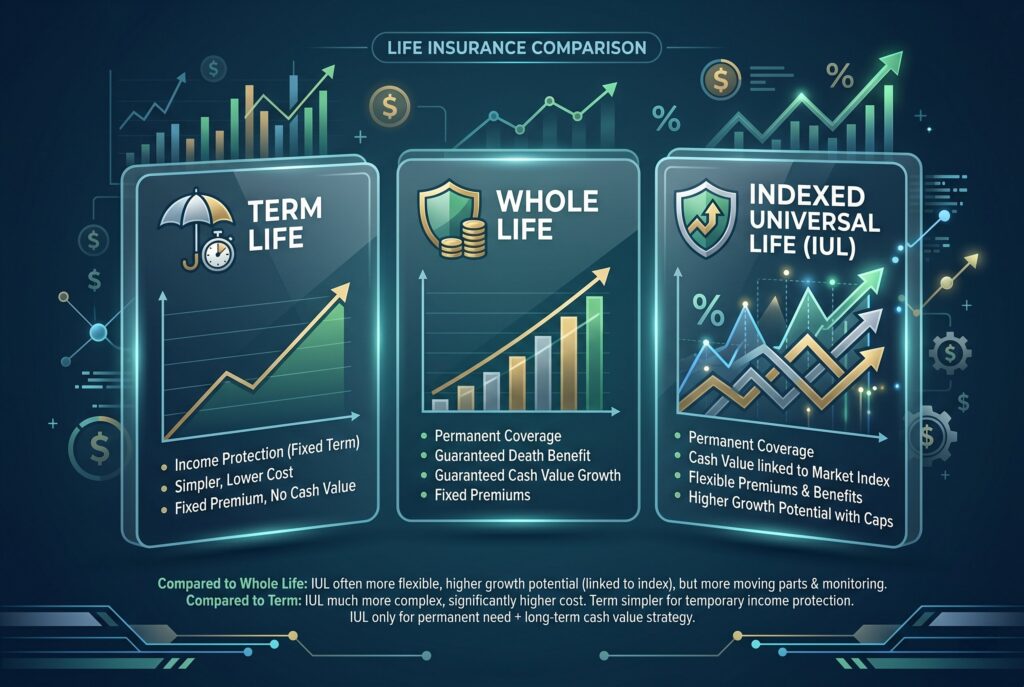

IUL vs Whole Life vs Term Life

Compared with whole life, IUL is usually more flexible. Premiums and death benefits can often be adjusted more easily, and the growth potential is tied to index crediting rather than fixed dividend or guaranteed-value structures. But that added flexibility also brings more moving parts and more monitoring risk.

Compared with term life, IUL is far more complex and much more expensive. The term is simpler, cleaner, and often better if you mainly need income protection for a certain number of years. IUL only makes sense if you want permanent coverage plus a long-term cash value strategy and can sustain the funding.

So the right comparison isn’t just IUL versus another insurance type. It’s also about purpose. Protection only, simplicity, flexibility, tax planning, and long-term affordability all matter.

In 2026, Is IUL Right for You?

In 2026, indexed universal life may fit you if you have high income, have already used more conventional tax-advantaged retirement accounts well, and want permanent coverage with downside-limited crediting potential. It may also appeal to people who like the idea of capital protection features in uncertain markets, even if that protection comes with capped upside.

But it’s usually a weaker fit for people who need short-term liquidity, who aren’t confident they can maintain premium funding, or who are still building basic financial stability. It’s also a poor fit for buyers who want a simple product with transparent long-term costs and little need for ongoing policy oversight. That’s the key suitability test. IUL isn’t a beginner’s product. It works best for disciplined, long-horizon buyers who understand the tradeoffs and can fund it properly.

Conclusion

An indexed universal life policy can be useful, but only when it’s understood clearly and designed carefully. It offers permanent life insurance, cash value potential, and downside-limited index crediting, but it also comes with caps, fees, insurer-controlled variables, and long-term management risk.

That’s why the smartest way to view IUL is as a strategic tool, not a shortcut. A max funded IUL can be far more effective than a weakly funded one, but even then it still needs careful review. Before signing anything, it’s worth stress-testing the illustration, examining the fee drag, and making sure the policy fits your real goals instead of a hypothetical sales narrative.