")

If you’ve seen the phrase on a will, trust document, retirement account, or life insurance form and wondered what per stirpes means, you aren’t alone. Per stirpes meaning sounds intimidating because it’s Latin, but the core idea is actually simple. It’s a way to make sure an inheritance stays within a family branch if one beneficiary dies before the person leaves the assets behind. Instead of that share disappearing or being redistributed only among surviving named beneficiaries, it passes down to that beneficiary’s descendants.

The easiest way to think about it is this: per stirpes is designed to protect generational wealth transfer. It helps prevent a situation where grandchildren are unintentionally left out just because their parents died before the estate owner. That’s why this term shows up so often in estate planning and beneficiary designations.

A quick summary makes the concept easier to hold onto. Per stirpes means by branch, not just by surviving individuals. It’s the main alternative to per capita, which distributes assets differently. And it applies not only to wills, but also to many beneficiary forms tied to retirement accounts and insurance policies.

The Core Definition: What Is Per Stirpes?

What is per stirpes? Per stirpes means by branch or by roots. In plain English, if a primary beneficiary dies before the person who owns the asset, that beneficiary’s share passes equally to that person’s descendants rather than being absorbed only by the remaining named beneficiaries. That is the simplest stirpes definition and the clearest answer to what is per stirpes.

Here is why that matters. Imagine a parent names three children as beneficiaries. If one child dies before the parent, a per stirpes instruction means that the deceased child’s children step into that place and receive that share. The inheritance follows the family line down the tree.

This is what separates per stirpes from more casual assumptions people often make. A lot of families assume “my grandchildren will automatically get their parent’s share,” but that isn’t always what happens unless the documents clearly say so. That’s why using the right wording on estate documents and beneficiary forms matters so much.

Per Stirpes vs. Per Capita: Which Should You Choose?

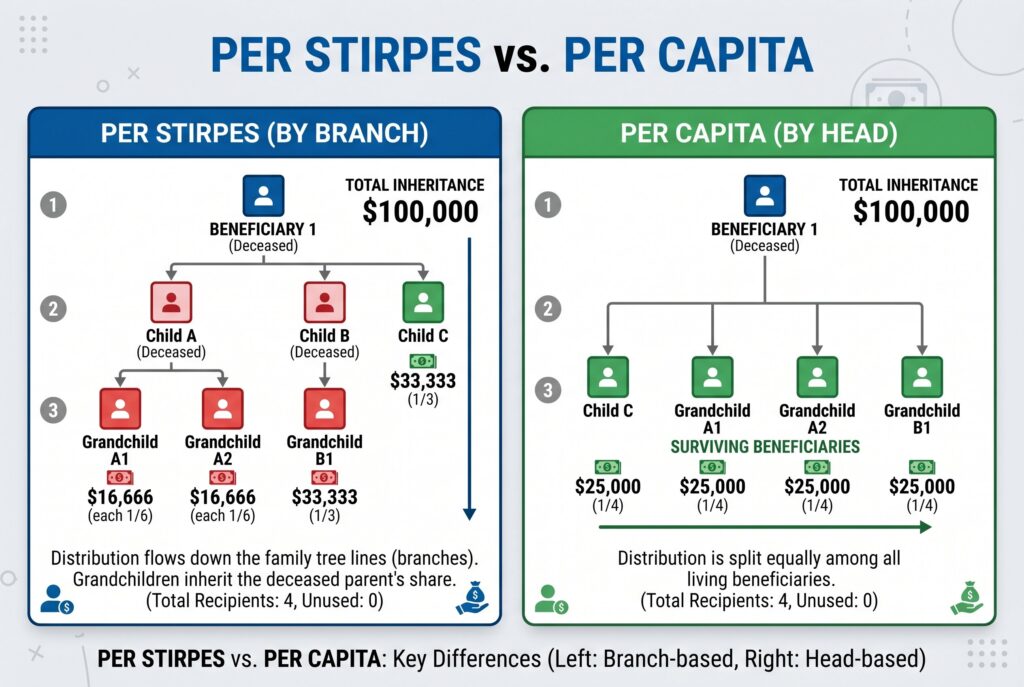

The most important comparison is per stirpes vs per capita. Per stirpes keeps the inheritance moving down a family branch. Per capita distributes assets only among the living beneficiaries at the same level, without preserving a deceased beneficiary’s branch in the same way.

In practical terms, per stirpes is usually chosen when someone wants each child’s family line protected. Per capita is often used when someone wants the surviving beneficiaries at the same generation level to split everything among themselves.

So if your main goal is to avoid accidental disinheritance of grandchildren, per stirpes is often the more protective choice. If your goal is to divide assets only among the surviving named people, per capita may better reflect that intention. That’s the real heart of per capita vs per stirpes. It isn’t just legal jargon. It reflects two different philosophies of family inheritance.

Real World Example: How a Per Stirpes Payout Works

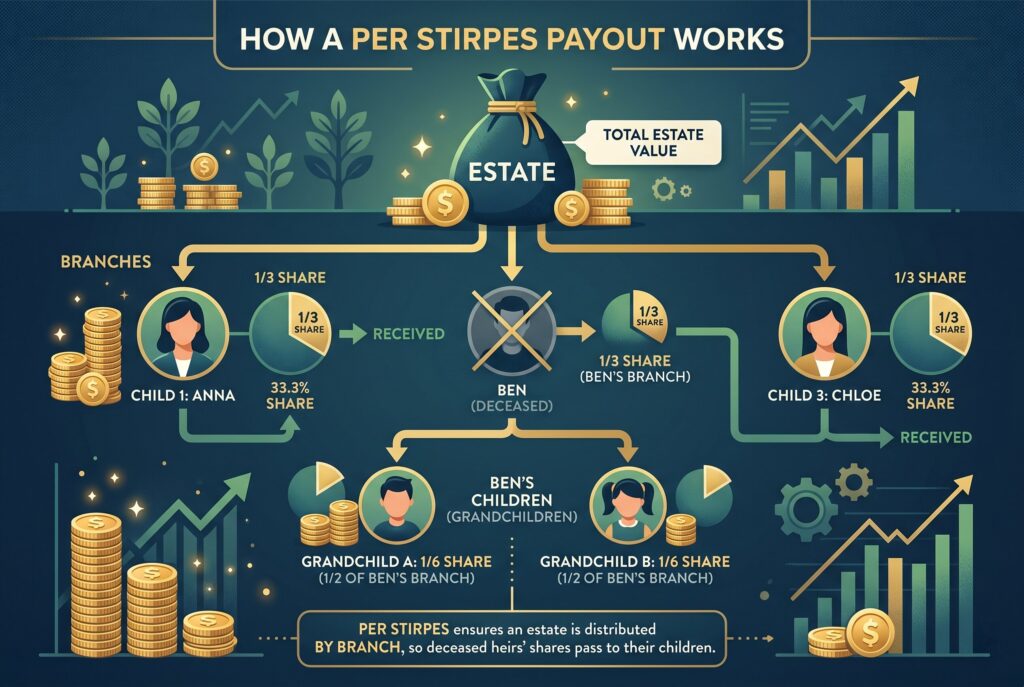

A simple scenario makes this much easier. Assume a parent leaves an estate to three children: Anna, Ben, and Chloe. Each child would normally receive one third. Now imagine Ben dies before the parent, but Ben has two children of his own.

If the estate is distributed per stirpes, Anna still receives one third, Chloe still receives one third, and Ben’s one third doesn’t disappear. Instead, Ben’s one third is split equally between Ben’s two children. That means each grandchild receives one sixth of the full estate.

This is why the phrase by branch is so useful. The estate doesn’t stop at Ben just because Ben is no longer alive. The branch continues. Without that structure, the result may be very different. Under a per capita approach, the surviving siblings might simply divide the estate between themselves, depending on the exact language and level of designation. That is exactly the kind of unintended outcome many people are trying to avoid.

Beyond the Will: Per Stirpes on Beneficiary Designations

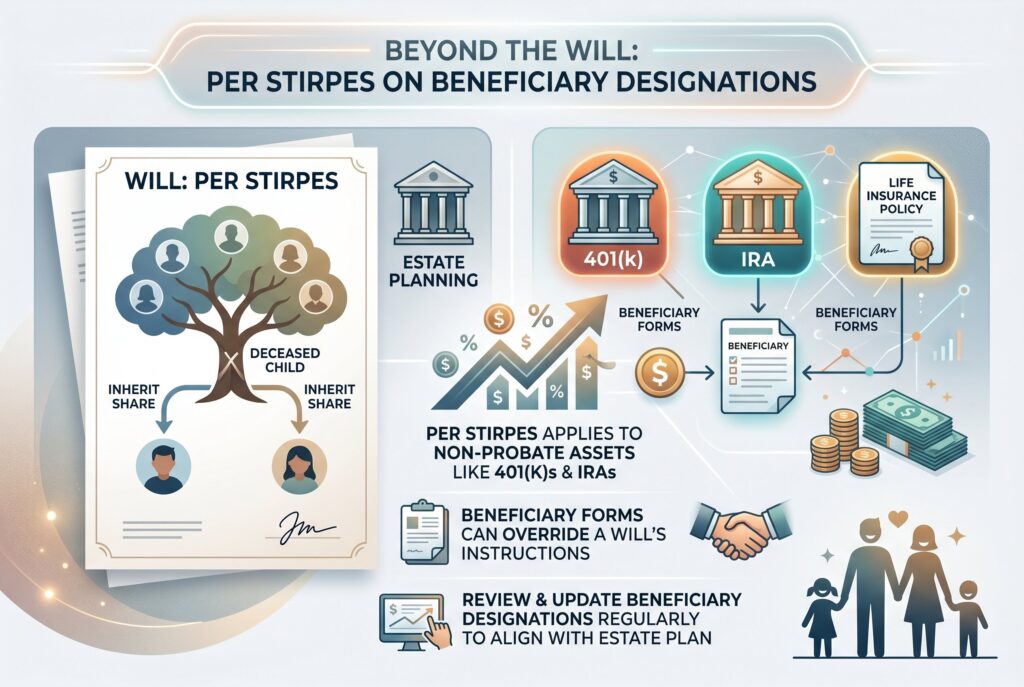

One of the biggest practical mistakes people make is assuming that per stirpes matters only in a will. It doesn’t. This term can also matter on beneficiary designation forms for non probate assets such as 401(k)s, IRAs, and life insurance policies. In many cases, those forms override what the will says, which is a detail that surprises a lot of families. If the beneficiary form says one thing and the will says another, the beneficiary form often controls that specific asset.

That makes the term far more important than a basic estate planning glossary item. It becomes a direct paperwork issue. When you’re updating your beneficiary form, the wording you choose can determine whether a deceased child’s children inherit that branch’s share or whether the money flows elsewhere. This is also why reviewing old beneficiary forms matters. People update their wills and forget their retirement accounts or life insurance. Then the family finds out too late that the transfer rules weren’t aligned.

The Hidden Tax Implications of a Per Stirpes Inheritance

The inheritance mechanics may be simple, but the tax consequences can be more complicated depending on the asset. For example, if a grandchild inherits part of an IRA per stirpes, that doesn’t mean the tax rules are the same as they would be for a surviving spouse. Different beneficiaries can face different distribution rules, and inherited retirement accounts may trigger more complicated timelines under current law.

That doesn’t mean per stirpes is a bad choice. It just means people should understand that “who receives the asset” and “how the asset is taxed” aren’t the same question. A will or beneficiary form can control the destination, but the tax treatment depends on the type of asset and the status of the beneficiary. This is one reason financial and estate planning decisions need to work together. The family tree logic may be emotionally clear, while the tax outcome may still require extra planning.

Conclusion

Per stirpes is one of those legal phrases that sounds harder than it is. In plain English, it means an inheritance follows the family branch if a beneficiary dies before the person leaving the assets. That simple rule can make a huge difference in whether grandchildren stay included in the transfer plan.

That is why per stirpes meaning matters so much in modern estate planning. It isn’t only about a will. It can shape how retirement accounts, insurance policies, and other beneficiary based assets move after death. When used thoughtfully, it helps make sure family wealth doesn’t accidentally skip the next generation.