vs. 401(k): Key Differences & Comparison")

The 403(b) vs 401(k) question is really about where you work, not just which retirement account looks better on paper. A 401(k) is usually offered by private, for-profit companies. A 403(b) plan is usually offered by public schools, universities, hospitals, churches, and other tax-exempt organizations. The difference between 401(k) and 403(b) matters because both can build serious retirement wealth, but they don’t always offer the same investments, fees, protections, or catch-up opportunities.

401(k) vs. 403(b): The Side-by-Side Comparison

Feature | 401(k) Plan | 403(b) Plan |

|---|---|---|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

The plans look similar because they are. Both may offer pre-tax contributions, Roth contributions, tax-deferred growth, employer matching, loans, hardship withdrawals, and required minimum distribution rules. But the details inside the plan can be very different.

Interactive Tool: The 2026 Maximum Contribution Calculator

To estimate your maximum 2026 contribution, start with your age:

- Under 50: $24,500

- Age 50 to 59: $24,500 + $8,000 = $32,500

- Age 60 to 63: $24,500 + $11,250 = $35,750

- Age 64+: $24,500 + $8,000 = $32,500

The SECURE 2.0 higher catch-up for ages 60 through 63 remains $11,250 for 2026.

For some 403(b) participants, the number may be even higher because of the 15-year rule. That special rule can allow up to an extra $3,000 per year, with a $15,000 lifetime maximum, if the employee qualifies and the plan permits it.

2026 Maximum Contribution Calculator

Use this calculator to estimate your maximum 2026 retirement plan contribution based on age, catch-up eligibility, and the optional 403(b) 15-year rule. The calculator applies the standard 2026 elective deferral limit, age-based catch-up amounts, and the special age 60 to 63 catch-up amount.

Under 50: $24,500

Age 50 to 59: $24,500 + $8,000 = $32,500

Age 60 to 63: $24,500 + $11,250 = $35,750

Age 64+: $24,500 + $8,000 = $32,500

Optional 403(b) 15-Year Rule: Up to $3,000 per year, subject to a $15,000 lifetime maximum and plan eligibility

Note: This calculator is for planning only. Actual limits, plan rules, catch-up ordering, payroll rules, employer contributions, and 403(b) 15-year rule eligibility can vary. Confirm your limit with your plan administrator or tax professional.

2026 Limits & The SECURE 2.0 Catch-Up Rules

The 403(b) max contribution 2026 starts with the same base limit as a 401(k): $24,500. That limit applies across employee elective deferrals to 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan.

The 403(b) 2026 contribution limits become more interesting when catch-up rules apply. Workers age 50 and older can generally add $8,000. Workers aged 60 to 63 may qualify for the larger $11,250 catch-up instead.

The 403(b) exclusive feature is the 15-year rule. Long-tenured employees of certain qualified organizations may contribute up to $3,000 extra per year if they meet the service and prior-contribution requirements. This rule is valuable, but it isn’t automatic. Your employer’s plan must allow it, and the calculation can be tricky.

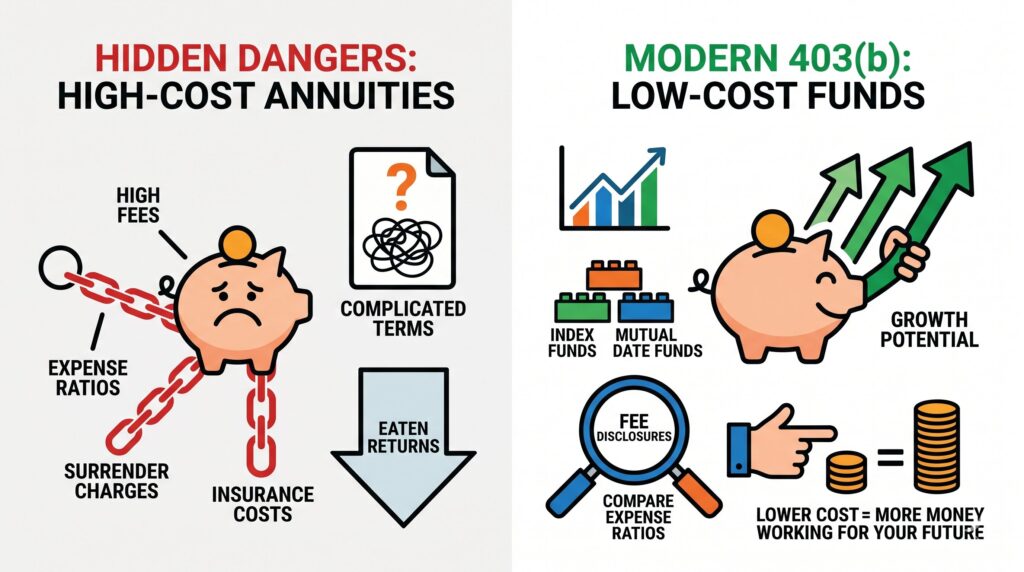

The Hidden Danger in 403(b) Plans: High Fees & Annuities

The biggest danger in some 403(b) plans isn’t the contribution limit. It’s the investment menu. Many 403(b) plans, especially in school systems, have historically offered annuity products. Some annuities can be useful in the right situation, but others may carry high expense ratios, surrender charges, insurance fees, and complicated contract terms. A teacher or nurse may think they’re simply saving for retirement, only to discover that too much of their return is being eaten by costs.

That doesn’t mean every 403(b) is bad. Many modern 403(b) plans now offer low-cost mutual funds, index funds, and target-date funds. The key is to read the fee disclosures, compare expense ratios, and avoid assuming every option on the plan menu is equally efficient.

A simple rule helps: if two funds give you similar market exposure, the lower-cost option often leaves more money working for your future.

Conclusion

Whether you have a 401(k) or a 403(b), the first rule is the same: contribute enough to capture the full employer match if you can. That match is part of your compensation, and skipping it can mean leaving retirement money behind. After that, focus on three things: contribution limits, investment costs, and tax strategy. A 403(b) plan can be excellent if it has low-cost options and useful catch-up rules. A 401(k) can be excellent if it offers a strong match and diversified funds. The account label matters, but the quality of the plan matters more.