an IRA? Account Differences Explained")

Is a 403(b) an IRA? No, and the difference matters more than it may seem. Retirement planning can feel like alphabet soup, especially for teachers, hospital workers, university employees, and nonprofit staff who may hear about a 403(b) plan, a Traditional IRA, and a Roth IRA all in the same benefits season. They’re all retirement accounts, but they aren’t the same tool. A 403(b) is tied to your employer. An IRA belongs to you as an individual.

Side-by-Side: 403(b) vs. IRA

| Feature | 403(b) Plan | Individual Retirement Account |

| Who opens it? | Your employer | You |

| Who is eligible? | Public sector and 501(c)(3) employees | Anyone with earned income |

| 2026 contribution limit | $24,500 if under 50 | $7,500 if under 50 |

| Employer match? | Often possible | No |

| Investment choices | Limited to employer plan menu | Broad brokerage menu |

| Payroll deduction? | Yes | No, usually manual or bank transfer |

| Best advantage | High limits and automation | Control and flexibility |

This is why comparing a 403(b) and an IRA isn’t really about choosing “the better account.” It’s about knowing which job each account does best.

Interactive Tool: 403(b) vs. IRA Savings Prioritization Calculator

A simple savings priority framework looks like this:

- First, contribute enough to your 403(b) to capture the full employer match. That match is part of your compensation, and skipping it’s like refusing free retirement money.

- Second, consider funding an IRA if your 403(b) has expensive investments, limited fund choices, or no employer match.

- Third, return to the 403(b) if you still have extra cash to invest and want to take advantage of the much higher 403(b) contribution limits.

Example: If your employer matches 50% of the first 6% of salary, start there. Then compare your IRA investment options against your 403(b) menu. If the IRA gives you lower-cost index funds and more control, it may deserve the next dollar.

403(b) vs. IRA Savings Prioritization Calculator

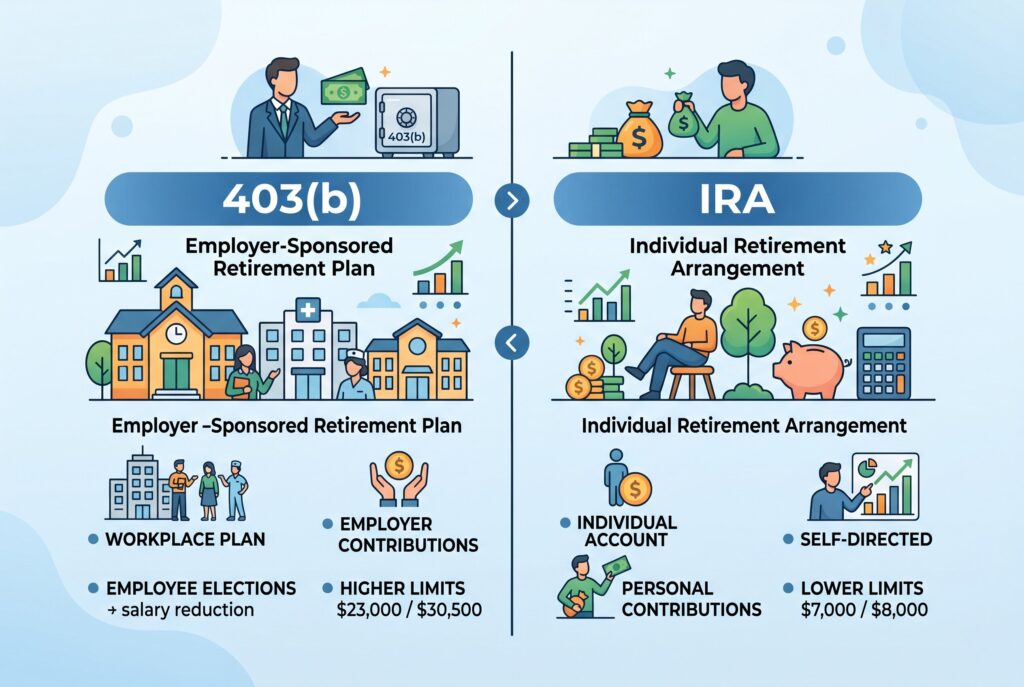

What Is a 403(b) Plan?

A 403(b) plan is a workplace retirement account for employees of certain public schools, universities, churches, hospitals, charities, and nonprofits. It works much like a 401(k), but it’s designed for tax-exempt and public-sector employers.

The 2026 advantage is contribution power. The 403(b) max contribution 2026 is $24,500 for workers under age 50. Older workers may be able to contribute more through catch-up rules, including higher limits for certain age groups. Another major advantage is automation. Contributions usually come directly from your paycheck before you have the chance to spend the money. That makes a 403(b) useful for people who want retirement saving to happen quietly in the background.

A 403(b) may also offer an employer match. If your employer contributes money when you contribute, that can make the 403(b) the first account to fund.

What Is an IRA?

An IRA is an Individual Retirement Account. Unlike a 403(b), it isn’t connected to your employer. You open it yourself, choose the provider, select the investments, and control the account.

The biggest advantage is investment freedom. A 403(b) might limit you to a short list of mutual funds or annuities. An IRA can usually hold stocks, ETFs, mutual funds, bonds, and other publicly available investments, depending on the brokerage.

That flexibility can also mean lower fees. If your workplace 403(b) has expensive products, an IRA may let you build a cleaner, cheaper portfolio. The tradeoff is the lower contribution limit. For 2026, the IRA limit is much smaller than the 403(b) limit. So an IRA gives you control, but a 403(b) gives you more contribution capacity.

The Teacher’s Trap: Watch Out for 403(b) Fees

Many public school teachers and nonprofit workers are offered 403(b) plans that include variable annuities, fixed annuities, or high-fee investment products. Some annuities may be appropriate for specific needs, but others can come with surrender charges, insurance costs, and management fees that quietly reduce long-term growth.

This is one of the biggest reasons an IRA can be attractive. If your 403(b) has no employer match and the investment options are expensive, funding an IRA first may be a smarter move. The goal isn’t to avoid every 403(b). The goal is to read the menu. Look for low-cost index funds, target-date funds, and transparent expense ratios. If the plan is packed with confusing products and high fees, slow down before contributing beyond the match.

Can You Contribute to a 403(b) and an IRA in the Same Year?

Yes. Contributing to a 403(b) doesn’t legally stop you from opening and funding an IRA in the same year. This is one of the most important planning points. A 403(b) and an IRA can coexist. You may use the 403(b) for employer match and high contribution limits, while using the IRA for flexibility and broader investment choices.

The tax caveat is income. If your income is too high, your ability to deduct Traditional IRA contributions may be limited. Your ability to contribute directly to a Roth IRA may also phase out. But those rules affect tax treatment and Roth eligibility, not whether the accounts can exist together.

Conclusion

A 403(b) isn’t an IRA. A 403(b) is your workplace retirement engine. An IRA is your personal retirement account. The smartest savers often use both. A practical 2026 order of operations is simple: get the 403(b) employer match first, then consider maximizing an IRA for better control and investment choice, then return to the 403(b) if you have extra cash and want to reach higher annual savings limits.

The account name matters less than the strategy. Use the 403(b) for scale. Use the IRA for control. Use both to build a retirement plan that doesn’t depend on one account doing everything.

Related Articles

Can I Withdraw From a 403(b) While Still Employed? 2026 Rules