While Still Employed? 2026 Rules")

Can I withdraw from 403(b) while still employed? Yes, but the better answer is: only in limited situations, and almost never casually. A 403(b) is built for retirement, so the IRS generally wants that money left alone until later in life. Still, real life doesn’t always wait for retirement. Medical bills happen. Jobs become unstable. Families face emergencies. In 2026, there are legal ways to access 403(b) money while still working, but every path has rules, taxes, and long-term tradeoffs.

Interactive Tool: The 2026 Withdrawal vs. Loan Simulator

Before taking a taxable withdrawal, compare it with a 403(b) loan.

Imagine you need $20,000.

If you take a withdrawal before 59½ and no exception applies, you may owe:

- Federal income tax

- Possible state income tax

- 10% early withdrawal penalty

- Lost future investment growth

If you’re in the 24% federal bracket, the federal tax and penalty alone could reach 34%, or $6,800 on a $20,000 withdrawal.

A 403(b) loan may avoid immediate tax and penalty if repaid properly. But it still reduces the amount invested, and failure to repay can turn the balance into a taxable distribution. The real question isn’t only “Can I access the money?” It’s “Which option damages my future the least?”

2026 Withdrawal vs. Loan Simulator

Compare the estimated cost of a taxable retirement plan withdrawal with a 403(b) loan. Enter the amount needed, tax rates, early withdrawal penalty, expected investment return, and loan repayment assumptions to see which option may damage your future the least.

Withdrawal Inputs

403(b) Loan Inputs

Withdrawal Tax and Penalty Cost = Amount Needed × (Federal Tax Rate + State Tax Rate + Penalty Rate)

Lost Future Growth = Amount Needed × ((1 + Expected Return)Years − 1)

Total Withdrawal Cost = Tax and Penalty Cost + Lost Future Growth

Estimated Loan Interest = Amount Needed × Loan Interest Rate × Loan Term

Total Loan Cost = Estimated Loan Interest + Loan Fees + Repayment Failure Risk Cost

Note: This simulator is educational and simplified. Actual 403(b) withdrawals and loans may involve plan rules, loan limits, repayment schedules, employment status, tax reporting, default treatment, and exceptions to the 10% penalty. Consider speaking with a qualified tax or financial professional before making a decision.

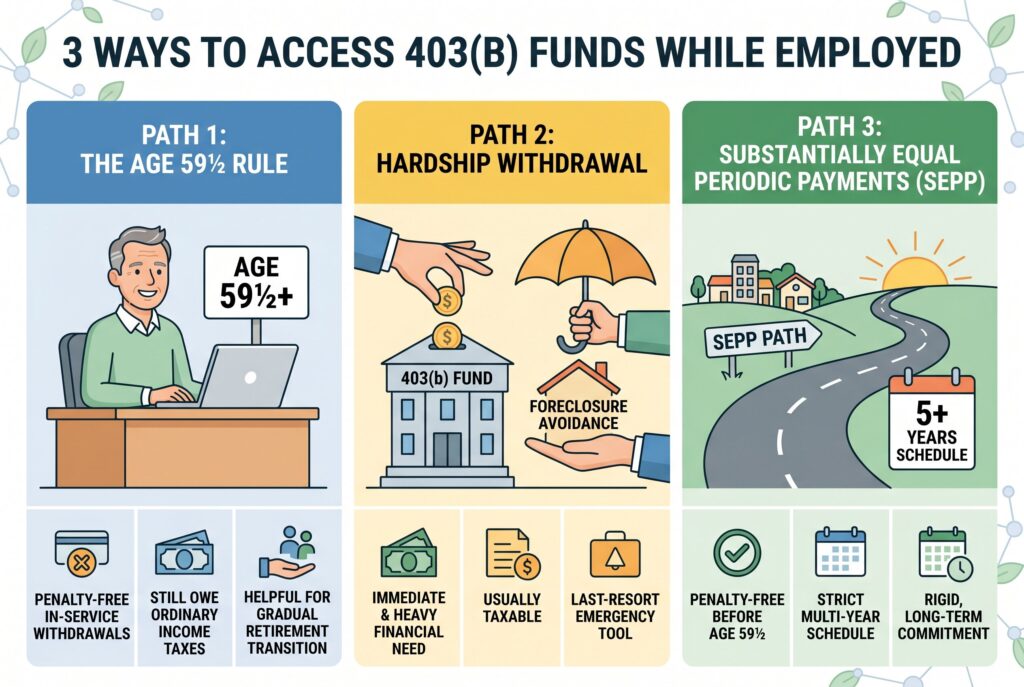

The 3 Ways to Access 403(b) Funds While Employed

Path 1: The Age 59½ Rule

Once you reach age 59½, many 403(b) plans allow penalty-free in-service withdrawals. You may still owe ordinary income taxes on withdrawals from a traditional pre-tax 403(b), but the 10% early withdrawal penalty usually no longer applies.

This can help older workers transition toward retirement gradually. For example, someone still employed at 61 may use a partial withdrawal to reduce work hours, pay off debt, or cover healthcare costs. Still, “penalty-free” doesn’t mean “tax-free.” Large withdrawals can push you into a higher tax bracket, affect deductions, or create unexpected tax pressure.

Path 2: 403(b) Hardship Withdrawal

A 403(b) hardship withdrawal may be available if you have an immediate and heavy financial need. Common hardship reasons may include unreimbursed medical expenses, costs to avoid eviction or foreclosure, certain tuition expenses, funeral costs, or repairs after certain casualty losses. The important catch: hardship withdrawals are still usually taxable. In some cases, the 10% penalty may also apply unless a separate penalty exception covers your situation.

Hardship withdrawals should be treated as a last-resort emergency tool. Once money leaves the retirement account, it loses future tax-deferred growth. You aren’t just spending today’s dollars; you’re spending the compounding those dollars could have created.

Path 3: Substantially Equal Periodic Payments

Substantially Equal Periodic Payments, also called SEPP or Rule 72(t), allow penalty-free distributions before age 59½ if you follow a strict multi-year schedule. This route can work for early retirees or people with carefully planned income needs, but it’s rigid. You generally must continue the payments for at least five years or until age 59½, whichever is longer. If you break the rules, penalties may apply retroactively. SEPP isn’t a quick cash fix. It’s a long-term distribution commitment.

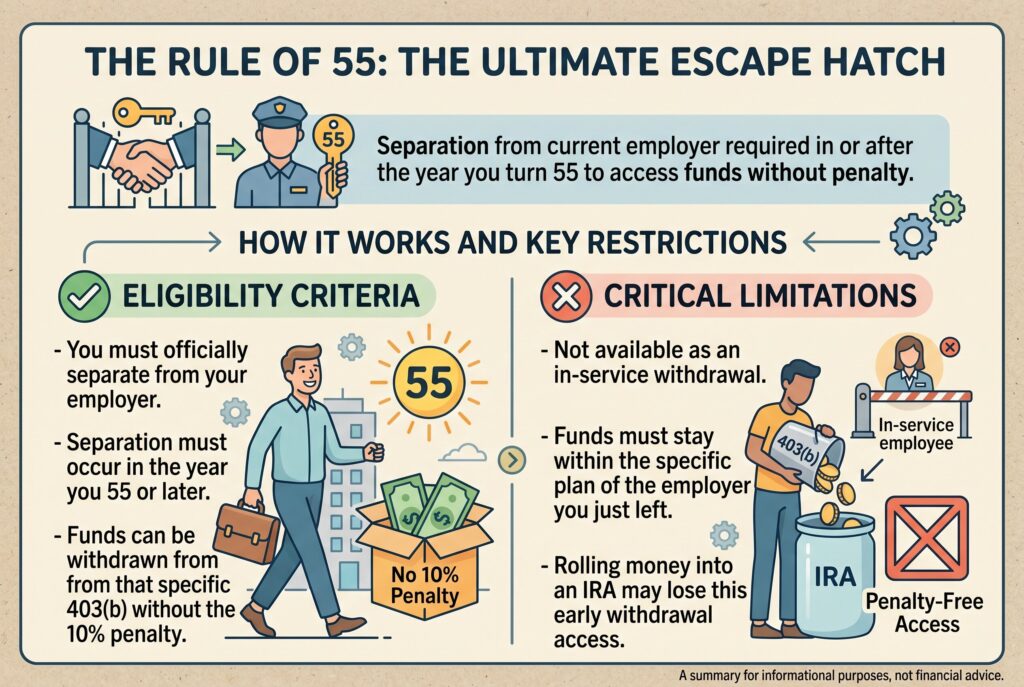

The Rule of 55: The Ultimate Escape Hatch

The rule of 55 can be powerful, but it’s often misunderstood. If you leave your job in or after the year you turn 55, you may be able to take money from that specific employer’s 403(b) without the 10% early withdrawal penalty. But this isn’t an in-service withdrawal. You must separate from the employer first. If you are still working for that employer, the rule of 55 generally doesn’t apply. Also, the rule usually applies only to the plan of the employer you just left. If you roll the money into an IRA, you may lose that specific rule-of-55 access.

403(b) Loans: The Smarter Alternative?

403(b) loans can be a better option than a taxable withdrawal if your plan allows them. Generally, you may be able to borrow up to 50% of your vested account balance, with a maximum loan of $50,000. The loan is typically repaid through payroll deductions, and the interest goes back into your own account.

The advantage is that a properly handled loan isn’t taxed and doesn’t trigger the 10% early withdrawal penalty. The catch is job risk. If you quit, are laid off, or are fired before repaying the loan, the remaining balance may become a taxable distribution. If you’re under 59½, the 10% penalty may also apply. A loan may be smarter than a withdrawal, but it isn’t harmless.

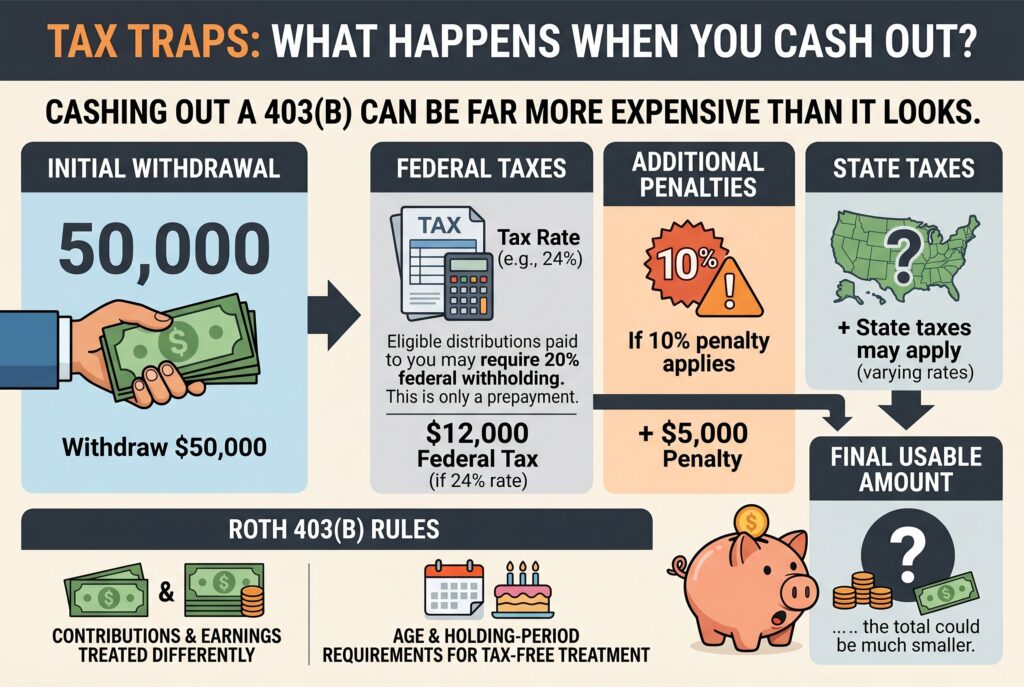

Tax Traps: What Happens When You Cash Out?

Cashing out a 403(b) can be far more expensive than it looks. If your distribution is eligible for rollover but is paid directly to you, the plan may be required to withhold 20% for federal taxes. That withholding isn’t necessarily the full tax you owe. It’s only a prepayment.

For example, if you withdraw $50,000 and your actual federal tax rate is 24%, you may owe $12,000 in federal tax. If the 10% penalty applies, that adds $5,000. State taxes may add more. So a $50,000 withdrawal may feel like emergency relief, but the final usable amount could be much smaller. Roth 403(b) withdrawals have their own rules. Contributions and earnings may be treated differently, and qualified tax-free treatment usually requires meeting age and holding-period requirements.

Conclusion

A 403(b) can be a lifeline in a crisis, but it shouldn’t be the first place you turn. Before taking an in-service withdrawal, review savings, budgeting changes, payment plans, personal loans, home equity options, or a 403(b) loan. Then call HR or your plan administrator and ask exactly what your plan allows: hardship withdrawals, age 59½ in-service withdrawals, loans, SEPP access, and rollover rules. The core lesson is simple: access is possible, but every dollar withdrawn today may be a dollar that isn’t compounding for tomorrow. Use the escape hatch only when the cost is clear and the need is real.