Contribution Limits: 2026 IRS Maximums & Rules")

The 403(b) 2026 contribution limits are higher than many workers realize, especially if you’re age 50 or older. The SECURE 2.0 Act changed the math for older savers, and the 403(b) max contribution 2026 now depends heavily on your age, your employer match, and whether you qualify for special catch-up rules. For teachers, university employees, hospital workers, nonprofit staff, and church employees, understanding these limits can turn a confusing HR form into a real retirement strategy.

Interactive Tool: The 2026 Paycheck Contribution Calculator

To turn the annual maximum into a paycheck amount, divide your target contribution by your remaining pay periods.

Example: You’re under 50 and paid twice a month.

- Annual target: $24,500

- Pay periods: 24

- Per-paycheck contribution: $1,020.83

If you’re age 61 and want to max out the $35,750 limit:

- Annual target: $35,750

- Pay periods: 24

- Per-paycheck contribution: $1,489.58

This is where retirement planning becomes practical. A limit on paper doesn’t help unless your payroll election is set correctly. If your HR portal takes one or two pay cycles to process changes, waiting until late December can make it harder to max out by year-end.

2026 Paycheck Contribution Calculator

Use this calculator to turn an annual retirement contribution target into a per-paycheck amount. Enter your annual target, amount already contributed, remaining pay periods, and optional payroll processing delay.

Remaining Contribution Needed = Annual Target − Already Contributed

Effective Pay Periods = Remaining Pay Periods − Payroll Processing Delay

Per-Paycheck Contribution = Remaining Contribution Needed ÷ Effective Pay Periods

Note: This calculator is for planning purposes only. Actual retirement contribution limits, catch-up rules, payroll deadlines, employer match rules, and plan limits may vary. Confirm your election with your HR or payroll provider.

The Employer Match & The Annual Additions Limit

The standard 403(b) contribution limits apply to the money you contribute from your paycheck. But the IRS also limits the combined amount that can go into your account from all sources. For 2026, the annual additions limit is $72,000, or 100% of includible compensation if lower. This includes your employee contributions, employer matching contributions, and other employer contributions.

Here’s the distinction:

- Your employee deferral limit: $24,500

- Your employer match: added separately

- Combined plan cap: $72,000

Example: If you contribute $24,500 and your employer contributes $8,000, your total annual additions are $32,500. That is below the $72,000 cap. Most employees won’t hit the combined cap, but high earners, medical professionals, university executives, and people with generous employer contributions should pay attention.

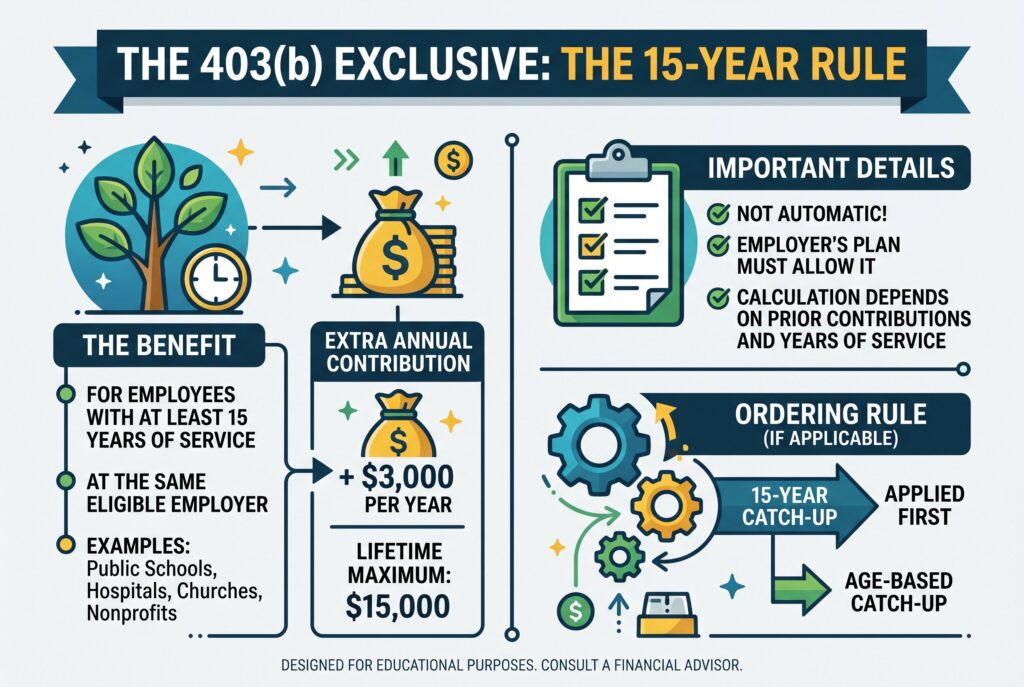

The 403(b) Exclusive: The 15-Year Rule

The 403(b) plan has one special feature that 401(k) plans don’t: the 15-year rule. If you’ve worked for the same eligible employer for at least 15 years, you may be allowed to contribute an extra $3,000 per year. The lifetime maximum is $15,000. This rule often applies to long-tenured employees of public schools, hospitals, churches, and certain nonprofits. But this benefit isn’t automatic. Your employer’s plan must allow it, and the calculation depends on prior contributions and years of service.

There is also an ordering rule. If you qualify for both the 15-year catch-up and the age-based catch-up, the 15-year catch-up is generally applied first. That matters because it affects how contributions are classified and tracked.

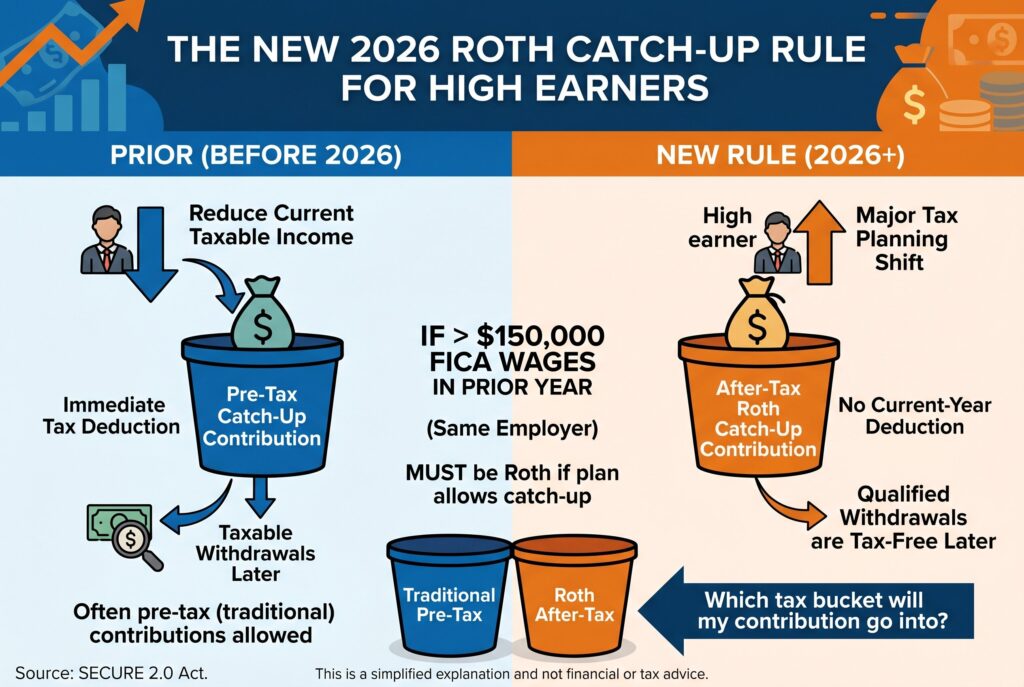

The New 2026 Roth Catch-Up Rule for High Earners

Starting in 2026, certain high earners must make catch-up contributions as Roth contributions. If you had more than $150,000 in FICA wages from the same employer in the prior year, your catch-up contributions must go into a Roth account if your plan allows catch-up contributions. This is a major tax planning shift.

Before, a high earner could often use catch-up contributions to reduce current taxable income. Under the new rule, those catch-up dollars may need to be after-tax Roth contributions instead. You don’t get the same current-year deduction, but qualified Roth withdrawals can be tax-free later. That means the question isn’t only “How much can I contribute?” It’s also “Which tax bucket will my contribution go into?”

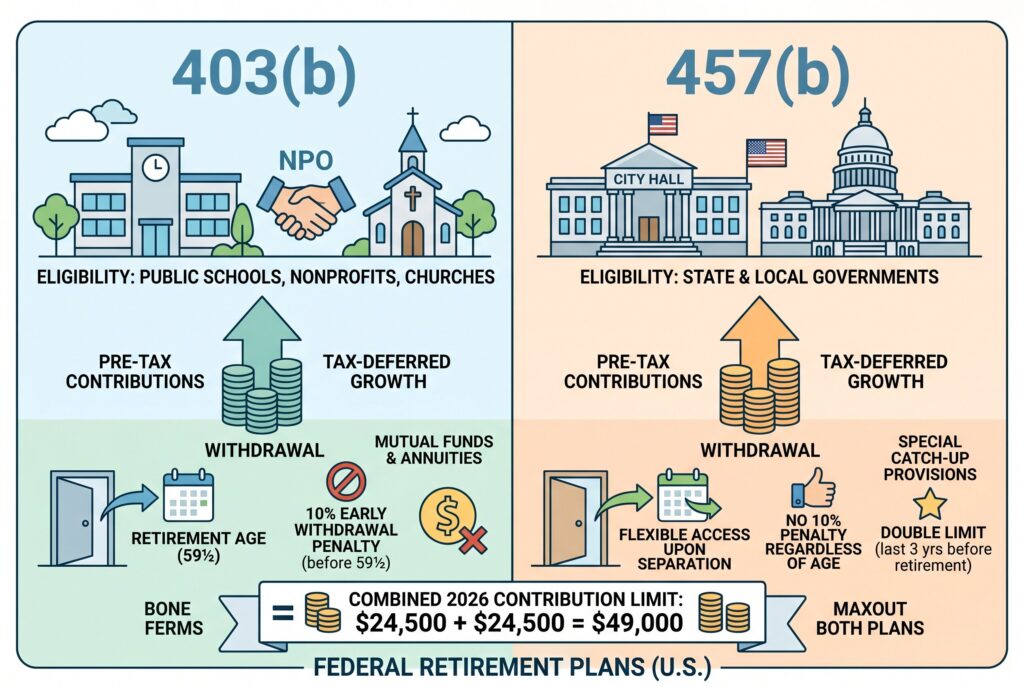

Can You Max Out Both a 403(b) and a 457(b)?

Yes, many public employees with access to both a 403(b) and a governmental 457(b) can contribute the maximum to both plans. This is one of the most powerful opportunities for university employees, public school administrators, and government workers.

For 2026, that may mean:

- $24,500 into a 403(b)

- $24,500 into a 457(b)

That is $49,000 before catch-up contributions. Older workers may be able to contribute even more depending on plan rules and catch-up eligibility. The key is that 403(b) and 457(b) limits can be separate. But payroll systems, employer rules, and plan documents still matter, so confirm with HR before assuming both are available.

Frequently Asked Questions

What Is a 403(b) Plan?

A 403(b) retirement plan is an employer-sponsored retirement account for employees of certain public schools, universities, churches, hospitals, and tax-exempt organizations. It works much like a 401(k): you contribute through payroll, choose investments from the plan menu, and receive tax advantages.

Can I Withdraw from 403(b) While Still Employed?

Sometimes, but access is limited. You may be able to withdraw under specific hardship rules, after age 59½, through certain plan loans, or after another qualifying event. If you take an early distribution without an exception, income taxes and a 10% penalty may apply.

What Happens if I Over Contribute?

Contact HR or your plan administrator as soon as possible. Excess deferrals generally need to be corrected by the tax deadline to avoid double taxation. Don’t wait until you file your return if you already know your payroll elections were too high.

Do Roth 403(b) Contributions Have a Separate Limit?

No. Roth and pre-tax 403(b) contributions share the same employee deferral limit. You can split contributions between both, but the combined amount still counts toward the same annual cap.

Conclusion

The smartest 403(b) strategy begins with a simple action: log into your HR portal and check your current payroll election. The IRS limits are annual, but your contributions happen one paycheck at a time. If your goal is to max out by December 31, calculate the exact dollar amount per pay period now. Then review your age-based catch-up eligibility, employer match, Roth catch-up requirement, and whether a 457(b) is also available. A 403(b) isn’t just a retirement account. Used well, it’s a disciplined system for turning every paycheck into future financial freedom.