Plan? 2026 Limits and Withdrawal Rules")

You just received a job offer from a government agency, public school, university, or nonprofit, and the benefits package mentions a 401(a) plan. If you are used to hearing about 401(k)s, the name can feel confusing. What Is a 401(a) Plan, and how is it different from other retirement accounts? Can you open one yourself? Are the contributions optional?

A 401(a) is an employer-sponsored retirement plan commonly used by public-sector, educational, and nonprofit employers. Unlike a 401(k), where employees usually decide how much to contribute, a 401(a) plan is largely controlled by the employer. The employer may decide who participates, how much employees must contribute, how much the employer contributes, and when those contributions become fully vested.

A 401(a) plan is an employer-sponsored money-purchase retirement plan offered mainly by government agencies, schools, universities, and nonprofits. Employers control the plan design, which may include mandatory employee contributions and specific vesting schedules. For 2026, the total defined contribution limit under Section 415(c) is $72,000.

How Does a 401(a) Plan Work? The Mandatory Rule

You can’t open a 401(a) plan on your own. It must be offered through your employer. That is the first major difference between a 401(a) plan and an IRA. Many 401(a) plans are built around mandatory or employer-directed contributions. For example, a public university might require eligible employees to contribute 8% of pay while the employer contributes 5%. In another plan, the employer may contribute without requiring employee contributions at all.

Common 401(a) plan designs include employer-only contributions, mandatory employee contributions, irrevocable employee election contributions, and after-tax employee contributions. The exact rules depend on the employer’s plan document, so two workers at different institutions may have very different 401(a) experiences.

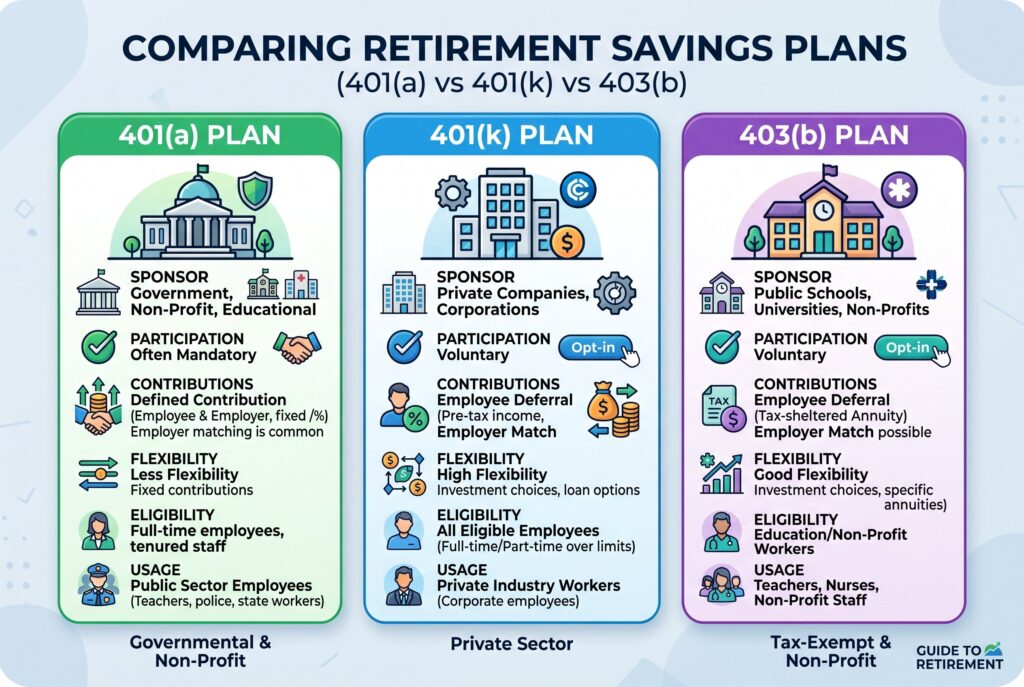

401(a) vs 401(k) vs 403(b): What Is the Difference?

A 401(a) is usually employer-controlled and often used by government, education, and nonprofit employers. Participation may be mandatory, and contribution rates may be set by the employer.

A 401(k) is more common in the private sector. Employees usually choose whether to participate and how much salary to defer, subject to annual limits.

A 403(b) is common for schools, universities, hospitals, religious organizations, and nonprofits. It’s often used as a voluntary supplemental retirement account. In some public-sector benefits packages, the 401(a) may hold employer contributions, while the employee can also save separately in a 403(b) or 457(b).

2026 401(a) Contribution Limits

For 2026, the total annual contribution limit for defined contribution plans, including many 401(a) plans, is $72,000 or 100% of compensation, whichever is lower. This total generally includes employer contributions, employee contributions, and forfeitures allocated to the account.

This isn’t the same as the 401(k) employee deferral limit. A 401(k) employee deferral limit controls how much an employee can elect to defer from salary into a 401(k), while the 401(a) limit is generally an overall annual additions limit. One important planning detail: 401(a) limits may operate separately from certain 457(b) plan limits. That is why some public employees can build retirement savings through a 401(a), a 403(b), and a 457(b), depending on what their employer offers.

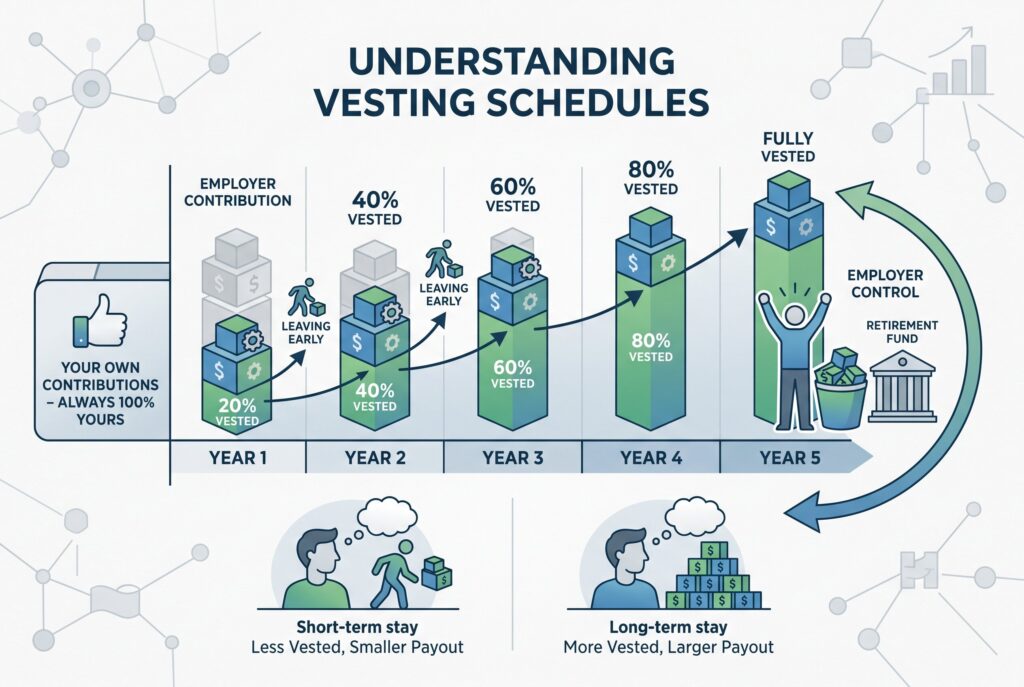

Vesting Schedules and Employer Control

Vesting determines how much of the employer-contributed money you truly own if you leave your job. Your own required employee contributions are usually yours, but employer contributions may vest over time. For example, a plan might vest 20% per year over five years. If you leave after two years, you may keep only 40% of the employer contribution balance. If you stay until fully vested, you keep 100%.

This matters when evaluating a job offer. A generous employer contribution is valuable, but only if you stay long enough to vest. Always read the vesting schedule, contribution formula, investment menu, and fees before assuming the plan is automatically better than another retirement benefit.

401(a) Withdrawal Rules, RMDs, and Rollovers

401(a) withdrawal rules are generally tied to retirement-plan tax rules and your employer’s plan document. If you withdraw money before age 59½, you may owe income tax and a 10% early withdrawal penalty unless an exception applies.

When you leave your job, you may be able to roll over your vested 401(a) balance into an IRA or another eligible employer plan. A direct rollover can help avoid current taxes and penalties while keeping the money invested for retirement. Required minimum distributions, or RMDs, may apply once you reach the IRS-required age. The exact timing can depend on current law, your employment status, and plan rules, so check the plan administrator before taking action.

Conclusion

If your 401(a) plan includes employer contributions or an employer match, it can be one of the most valuable parts of your benefits package. Turning down employer money is usually a mistake unless fees are unusually high or the plan has serious limitations.

The smartest approach is to understand how your 401(a) works with your other accounts. If your employer also offers a 403(b) or 457(b), those accounts may let you save more on top of the 401(a). Review contribution rules, vesting, investment choices, and rollover options before making decisions. A 401(a) isn’t as familiar as a 401(k), but for many public-sector and nonprofit employees, it can become the foundation of a strong retirement strategy.

Related Articles

- 401(a) vs. 403(b): 2026 Mandatory vs. Voluntary Rules

- 401(a) vs 401(k): 2026 Key Differences and Which Plan Is Better?

- Traditional IRA Rules and Tax Benefits Explained: A Simple Beginner’s Guide for Smart Saving

- Roth IRA Calculator: Estimate Your Tax-Free Savings and Future Growth with Simple Tips

- Social Security Retirement Age Explained: Early, Full, and Delayed Benefits for Smarter Planning