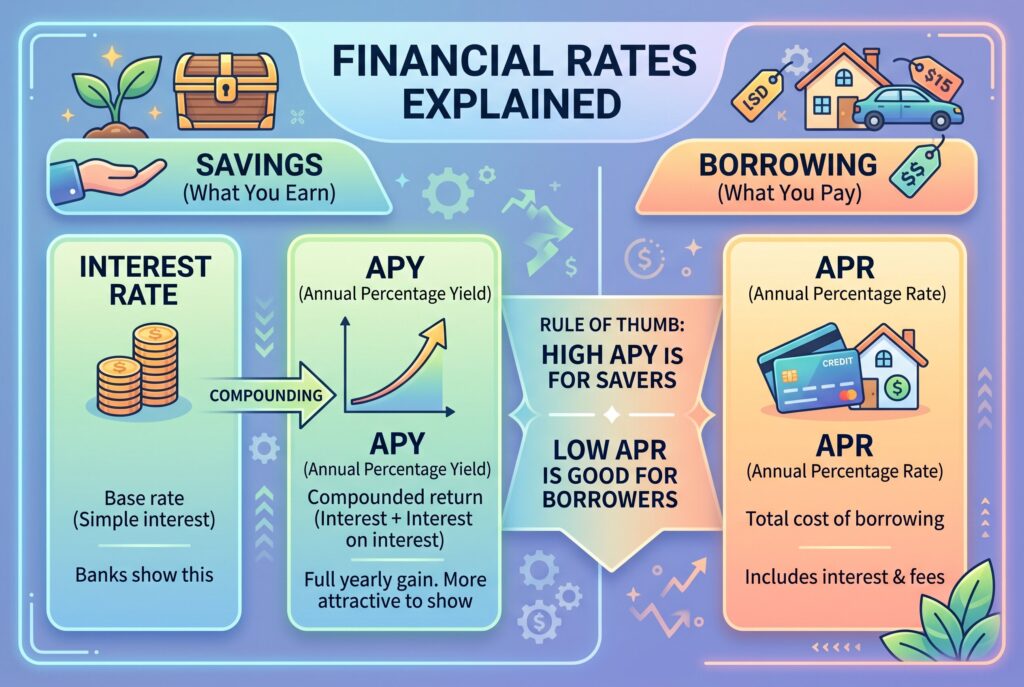

Dividend rate vs APY is a common source of confusion, especially for credit union members. Traditional banks usually talk about an interest rate, while credit unions often use the term dividend rate. In practice, both describe the base rate your money earns before compounding. APY is the number that shows your real annual earning power, which is why it matters most when comparing savings accounts, money market accounts, CDs, or share certificates.

What Is A Dividend Rate? The Credit Union Difference

A dividend rate is the base rate a credit union pays on a deposit account. It works much like an interest rate at a traditional bank. The language is different because credit unions are member owned, so they distribute earnings to members as dividends.

This doesn’t mean the dividend rate is the same as stock market dividends. Stock dividends are paid by companies to shareholders. A credit union dividend rate is simply the return paid on accounts such as savings, money market accounts, and share certificates. When comparing offers, the dividend rate tells you the starting point. It doesn’t show the full effect of compounding, so it isn’t always the best number to use alone.

What Does APY Mean? The Power Of Compounding

What does APY mean? APY stands for Annual Percentage Yield. It shows how much you can earn over one year when compounding is included. Compounding means your earned dividends or interest can begin earning more money too.

For example, if your account compounds monthly, your first month’s earnings are added to the balance. The next month, you earn on the original balance plus the previous earnings. Daily compounding can increase the final APY slightly more than monthly or quarterly compounding. That’s why APY is more useful than the base rate. It gives you a clearer view of your total annual return.

Interactive Tool: Dividend Rate To APY Converter

A dividend rate to APY converter helps you see why the APY is usually higher. You enter the dividend rate, choose the compounding frequency, and compare the final annual yield.

For example, a 4.50% dividend rate compounded monthly won’t produce exactly 4.50% APY. The APY will be slightly higher because the account earns on previously earned dividends. The more often compounding happens, the more noticeable the difference becomes. This is why savers shouldn’t rely only on the advertised dividend rate. If two accounts show similar base rates, the one with the stronger APY may produce better real earnings.

Dividend Rate to APY Converter

Use this calculator to convert a dividend rate into annual percentage yield, or APY. Enter the dividend rate, choose the compounding frequency, and optionally add a balance to estimate annual dividend earnings.

Note: This calculator estimates APY based on compounding frequency. Actual APY may vary depending on account rules, dividend posting schedule, minimum balance requirements, and financial institution policies.

APY vs. Interest Rate And Where APR Fits In

APY vs interest rate is similar to dividend rate vs APY. The interest rate is the base number. APY is the compounded result. Banks usually say interest rate, while credit unions may say dividend rate, but both are starting points. Interest rate vs APY matters because financial institutions may advertise different numbers depending on what looks more attractive. A savings account may highlight APY because it gives the full yearly return. A simple interest rate may look lower because it doesn’t show compounding.

APR vs APY is different. APR is usually what you pay on borrowed money, such as loans or credit cards. APY is what you earn on deposit accounts. A simple rule helps: low APR is good when borrowing, high APY is good when saving.

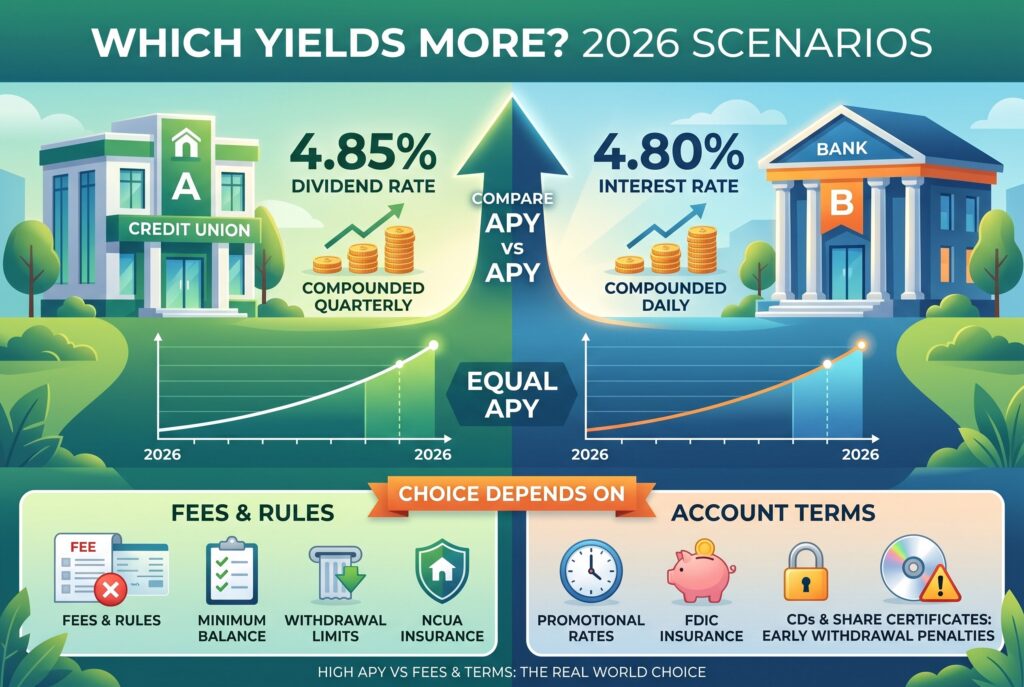

Which Yields More? Real World Scenarios

Imagine Credit Union A offers a 4.85% dividend rate compounded quarterly. Bank B offers a 4.80% interest rate compounded daily. At first, Credit Union A looks better because the base rate is higher.

But the right comparison isn’t dividend rate vs interest rate. It’s APY vs APY. Daily compounding at Bank B may narrow the gap or even beat the credit union offer depending on the exact formula and account terms.

Now imagine both accounts have the same APY. In that case, the better choice may depend on fees, minimum balance rules, withdrawal limits, insurance coverage, and whether the rate is promotional. A high APY isn’t useful if you can’t meet the balance requirement or if monthly fees reduce your earnings. For CDs and share certificates, also check early withdrawal penalties. A slightly higher APY may not be worth it if you might need the money before maturity.

Conclusion

The key takeaway is simple: stop judging savings products by the base dividend rate alone. Dividend rate tells you what the account starts with, but APY tells you what you can actually earn after compounding. When comparing credit union accounts, bank savings accounts, CDs, money market accounts, or share certificates, always look for the APY in the fine print. If two products seem close, compare APY, fees, compounding frequency, minimum balances, and withdrawal rules. That’s how you find the account that truly helps your money grow in 2026.