How long will my money last? That is one of the most important questions in retirement planning because it turns a large account balance into a real-life timeline. A $700,000 portfolio may feel comfortable until you compare it with annual withdrawals, inflation, healthcare costs, taxes, and market downturns.

The answer depends on three core factors: your starting balance, your annual withdrawal rate, and your investment return. You need to compare your savings, spending, and expected income sources using a how long will my money last calculator. In retirement, your money doesn’t simply sit still. You withdraw from it, markets move, inflation raises prices, and taxes reduce what you keep. That is why a retirement withdrawal calculator is useful: it shows whether your plan is sustainable or whether you need to adjust before the numbers become stressful.

Interactive Tool: The Retirement Withdrawal Calculator

Retirement Withdrawal Calculator

Use this calculator to estimate how long retirement savings may last. Enter your beginning balance, annual withdrawal, expected return, inflation rate, tax rate, and optional annual income. The tool also shows projected balances at 20-year, 30-year, and 40-year horizons.

| Horizon | Projected Ending Balance | Status |

|---|---|---|

| 20 Years | $0.00 | Not calculated |

| 30 Years | $0.00 | Not calculated |

| 40 Years | $0.00 | Not calculated |

Starting Withdrawal Rate = Annual Withdrawal ÷ Beginning Balance × 100

Net Withdrawal Need = Annual Withdrawal − Annual Part-Time or Other Income

Gross Withdrawal Needed = Net Withdrawal Need ÷ (1 − Tax Rate)

Each Year: Balance grows by expected return, then inflation-adjusted gross withdrawal is subtracted

Note: This is a simplified planning calculator. It does not model market volatility, sequence-of-returns risk, required minimum distributions, Social Security timing, pension income, changing taxes, fees, or healthcare shocks. Use it as a starting estimate, not a retirement plan.

A retirement withdrawal calculator estimates how many years your savings may last based on inputs such as beginning balance, annual withdrawals, expected return, inflation, and tax assumptions. For example, if you have $1,000,000 saved and withdraw $50,000 per year, your starting withdrawal rate is 5%. If your portfolio earns enough to offset withdrawals and inflation, it may last for decades. But if returns are weak early in retirement, that same withdrawal plan may drain your balance faster than expected.

A how long will my money last calculator is especially helpful because it makes the tradeoffs visible. Lower spending, part-time income, delayed withdrawals, or a more balanced investment plan can extend your timeline dramatically. If you are wondering how long will my money last in retirement, don’t look only at the first year. Look at a 20-year, 30-year, and 40-year horizon. A retiree at 67 may need money for 25 years. Someone retiring at 55 may need it to last 40 years or more.

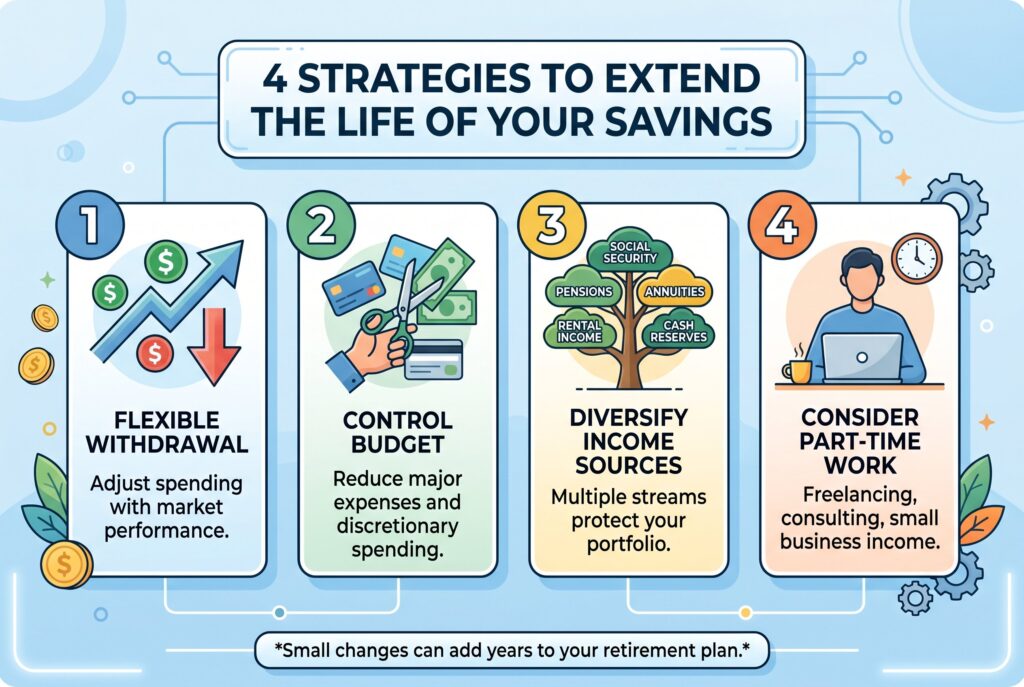

4 Strategies to Extend the Life of Your Savings

If your calculation shows your money may run out too soon, the solution isn’t always to panic or return to full-time work. Often, small changes can add years to your plan.

Adjust Your Withdrawal Strategy

A fixed withdrawal strategy can be risky, especially when the market is down. If you keep withdrawing the same amount during a downturn, you may be forced to sell investments at lower prices, which can damage your portfolio over time. A flexible withdrawal strategy gives you more control. In strong market years, you may allow yourself to spend a little more. In weaker years, you can reduce discretionary expenses such as travel, dining out, or large purchases. This helps protect your investments and gives your portfolio more time to recover.

Control Your Retirement Budget

Reducing expenses is one of the most powerful ways to make retirement savings last longer. Every dollar you don’t withdraw can remain invested and continue working for you. Review major spending categories such as housing, insurance, subscriptions, travel, dining, gifts, and vehicle costs. The goal isn’t to make retirement feel restrictive or unpleasant. Instead, it’s to protect your financial freedom and reduce unnecessary pressure on your portfolio.

Diversify Your Retirement Income Sources

Relying on only one source of retirement income can create unnecessary risk. A stronger retirement plan often includes multiple income streams, such as Social Security, pensions, annuities, rental income, dividends, interest, business income, or cash reserves. When income comes from different sources, you don’t have to depend entirely on selling investments. This can reduce stress during market downturns and help create a more stable retirement income plan.

Consider Part-Time Work in Retirement

Part-time work can make a meaningful difference in retirement, even if you only earn a modest amount. Freelancing, consulting, seasonal work, or running a small business can help reduce the amount you need to withdraw from your savings. Even an extra $15,000 or $25,000 per year can delay portfolio depletion and give your investments more time to recover after market declines. For some retirees, part-time work also provides structure, purpose, and social connection.

Tax-Smart Withdrawals: Which Accounts to Tap First?

Understand the Tax Impact of Your Withdrawals

The amount you withdraw in retirement is important, but the source of those withdrawals can be just as important. Different accounts are taxed in different ways, and a poor withdrawal strategy can increase your tax bill and shorten the life of your savings. A retirement distribution calculator can help compare different withdrawal sequences and estimate how taxes may affect your long-term retirement income.

Use Taxable Brokerage Accounts Strategically

Taxable brokerage accounts are often a useful source of income in the early years of retirement. Unlike traditional retirement accounts, taxes generally apply only to investment gains rather than the full amount withdrawn. This can help keep your taxable income lower and provide greater flexibility when managing cash flow. An investment withdrawal calculator can help estimate how selling investments may affect both taxes and portfolio longevity.

Plan Carefully for IRA and 401(k) Withdrawals

Withdrawals from traditional IRAs and 401(k) plans are generally taxed as ordinary income. As a result, taking large distributions in a single year can push you into a higher tax bracket and increase your overall tax liability. An IRA withdrawal calculator can help estimate taxes before you take money out, allowing you to make more informed decisions about when and how much to withdraw.

Maintain a Cash Reserve for Market Downturns

Cash reserves serve a different purpose than investment accounts. They provide a financial cushion that can cover expenses during periods of market volatility. A savings withdrawal calculator can help estimate how long your cash reserve may last based on your spending needs. Having cash available can reduce the need to sell stocks during market declines, helping protect your portfolio from losses that may be difficult to recover from later.

Create a Tax-Efficient Withdrawal Order

Many retirees follow a withdrawal strategy that starts with taxable accounts, then moves to tax-deferred accounts, and finally uses Roth accounts when needed. However, the optimal order depends on several factors, including your age, tax bracket, Social Security claiming strategy, required minimum distributions (RMDs), and estate planning goals. Building a tax-efficient withdrawal plan can help reduce lifetime taxes and improve the sustainability of your retirement income.

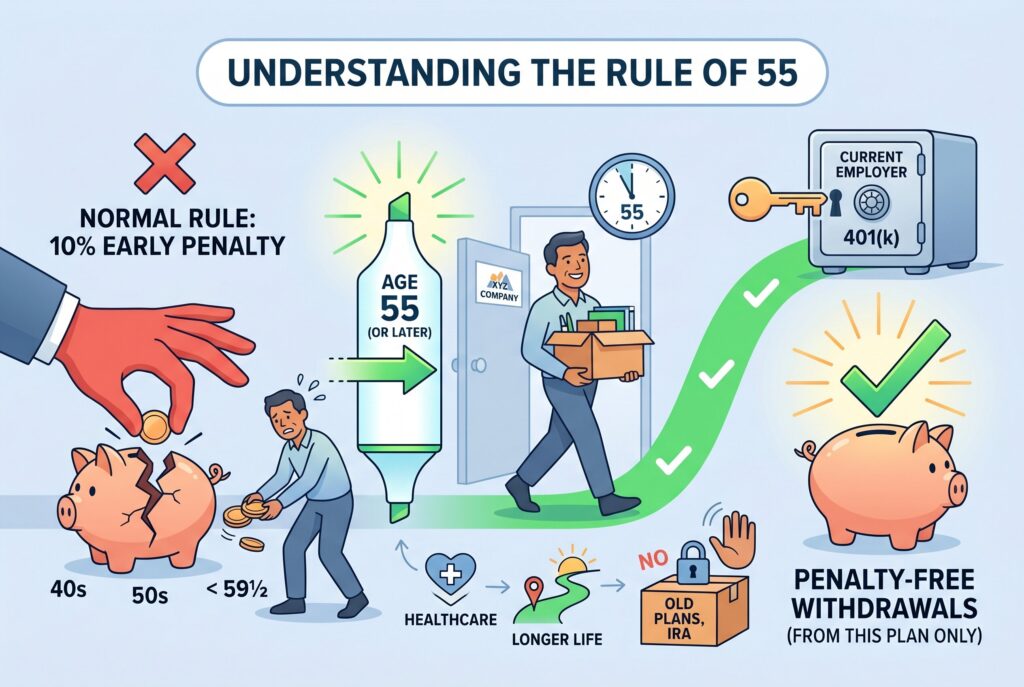

Retiring Early? Understanding the Rule of 55

In case you want to retire at 55, you need to understand early withdrawal rules. Normally, taking money from a 401(k) or IRA before age 59½ can trigger a 10% early withdrawal penalty, plus income taxes. The rule of 55 may offer an exception. Under the 401(k) rule of 55, if you leave your job during or after the year you turn 55, you may be able to withdraw from that employer’s 401(k) without the 10% early withdrawal penalty.

This rule generally applies only to the 401(k) connected to the employer you just left. It usually doesn’t apply to old 401(k)s from previous employers or traditional IRAs. That means rollovers should be handled carefully before early retirement. The rule of 55 can be useful, but it isn’t a reason to retire without a full plan. You still need healthcare coverage, a spending plan, tax projections, and enough assets to support a longer retirement.

Conclusion

Your retirement path isn’t a straight line. Markets change, inflation changes, health changes, and your spending habits may change. That is why investment plan review should happen at least once a year. Ask yourself: Is my withdrawal rate still reasonable? Are my expenses rising faster than expected? Do I have enough cash for weak markets? Are my retirement income sources diversified? Should I adjust my tax strategy?

Professional advice can be valuable if your situation includes multiple accounts, early retirement, Social Security decisions, Roth conversions, pensions, rental income, or large tax questions. The question of how long will my money last isn’t something you answer once and forget. It’s a question you revisit regularly. Use a retirement withdrawal calculator, update your assumptions, and adjust before small problems become permanent. Retirement confidence comes from knowing your plan can bend without breaking.

Related Articles

Can I Cancel My 401(k) and Cash Out While Still Employed? (2026 Hardship Rules)