and Cash Out While Still Employed? (2026 Hardship Rules)")

Can I cancel my 401(k) and cash out while still employed? In most cases, not exactly. If you are still working for the company that sponsors your 401(k), your plan usually won’t let you close the account and withdraw the entire balance just because you want the money. However, that doesn’t mean you have no options. You can usually stop 401(k) contributions by contacting HR or changing your payroll election. And if you are facing a serious financial emergency, your plan may allow limited access through a hardship withdrawal from 401(k), a 401(k) loan, or an in-service withdrawal.

The key is understanding the difference between “canceling” your 401(k) and legally accessing part of it. A 401(k) is designed for retirement savings, not short-term cash flow. Taking money out early can trigger taxes, penalties, and lost investment growth that may hurt your future more than you expect.

Why You Can’t Just Cancel and Cash Out

A 401(k) isn’t like a checking account. It’s a tax-advantaged retirement account governed by IRS rules and your employer’s plan document. Because you received tax benefits for contributing, there are restrictions on when and how you can withdraw 401(k) funds.

When you are still employed, your money is often “locked in” to protect retirement assets from impulsive withdrawals. Most plans don’t allow a full cash out 401(k) while employed. Your employer may allow you to stop new contributions, but the existing balance usually stays in the plan until you leave the job, retire, reach a qualifying age, or meet a special withdrawal condition. This is why the phrase cancel 401(k) can be misleading. You may be able to pause or stop payroll contributions, but that is different from closing the account and taking the money.

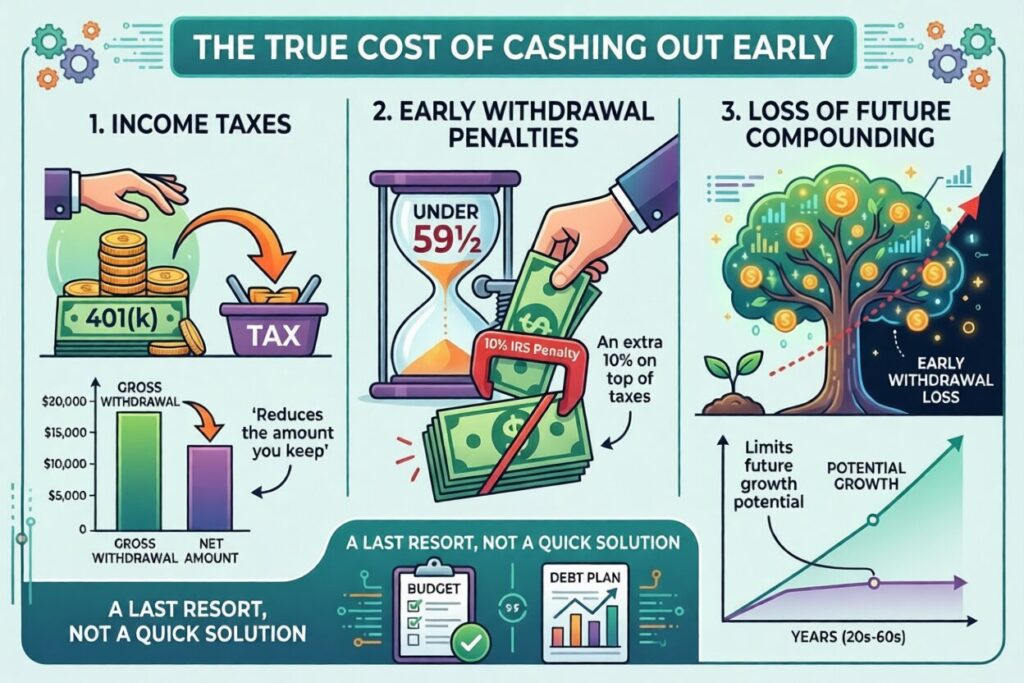

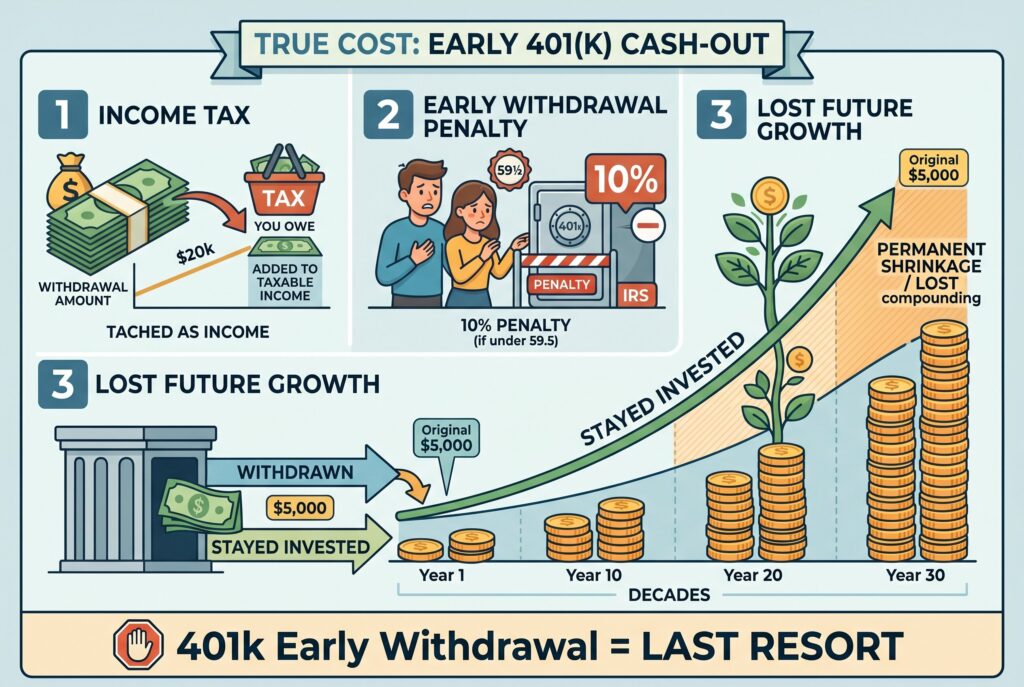

The True Cost of Cashing Out Early

Even when early access is allowed, the cost can be painful.

Income Taxes Can Reduce the Amount You Keep

One of the first costs of cashing out retirement savings early is income tax. Withdrawals from a traditional 401(k) are generally treated as ordinary income, meaning the money is added to your taxable income for the year. For example, withdrawing $20,000 could increase your tax bill and potentially push you into a higher tax bracket. Before taking money out, it’s important to understand how the withdrawal may affect your overall tax situation.

Early Withdrawal Penalties Can Add Extra Costs

If you withdraw money from a retirement account before age 59½, you may also face an early withdrawal penalty. In many cases, the IRS imposes an additional 10% penalty on top of any income taxes owed, unless you qualify for a specific exception. This means a substantial portion of your withdrawal could be lost to taxes and penalties before you ever use the money.

The Loss of Future Compounding Is the Biggest Risk

The most significant cost of an early withdrawal is often the growth you give up in the future. Money invested in a retirement account has years or even decades to benefit from compound returns. A $5,000 withdrawal today may seem manageable, but that same amount could have grown substantially over time if left invested. By removing funds early, you reduce the size of your portfolio and limit its ability to generate future growth. For this reason, an early 401(k) withdrawal is generally best viewed as a last resort rather than a quick solution to debt or short-term financial challenges.

Interactive Tool: Early Withdrawal Penalty Calculator

Early Withdrawal Penalty Calculator

Use this calculator to estimate the real cost of an early 401(k) withdrawal. Enter the withdrawal amount, tax rates, penalty rate, plan withholding, years until retirement, and expected investment return to estimate cash received and lost future growth.

Federal Tax = Withdrawal Amount × Federal Tax Rate

State Tax = Withdrawal Amount × State Tax Rate

Early Withdrawal Penalty = Withdrawal Amount × Penalty Rate

Estimated Cash Received = Withdrawal Amount − Federal Tax − State Tax − Penalty

Lost Future Value = Withdrawal Amount × (1 + Expected Return)Years Until Retirement

Total Estimated Cost = Taxes + Penalty + Lost Future Growth

Note: This calculator is for planning only. Actual 401(k) withdrawals may involve exceptions, mandatory withholding, state rules, local tax, plan rules, income phaseouts, and tax filing adjustments. This is not tax or financial advice.

Before you withdraw 401(k) funds, estimate the real cost. A basic early withdrawal penalty calculator should include:

- Withdrawal amount

- Federal tax bracket

- State tax rate

- 10% early withdrawal penalty

- Plan withholding

- Years until retirement

- Estimated investment return

For example, a $20,000 early withdrawal may lose $2,000 immediately to the 10% penalty. If you are in a 22% federal tax bracket, another $4,400 may go to federal income tax before state tax is even considered. Your actual cash received could be far lower than the amount you withdrew. The calculator should also show lost growth. If $20,000 could have grown at 7% annually for 25 years, the future value could be dramatically higher than today’s emergency cash.

3 Legal Ways to Access Your 401(k) While Still Employed

There are legal ways to access money while still employed, but each has strict rules.

1. Hardship Withdrawal from 401(k)

A hardship withdrawal from 401(k) may be allowed if you have an immediate and heavy financial need. Common qualifying reasons may include certain medical expenses, costs to buy a primary residence, tuition, funeral expenses, repairs after casualty losses, or payments needed to prevent eviction or foreclosure. The benefit is that you don’t have to repay the money. The downside is serious: the withdrawal may be taxable, may face the 10% penalty if no exception applies, and permanently removes money from your retirement account.

2. 401(k) Loan

A 401(k) loan lets you borrow from your own vested balance. Many plans cap loans at 50% of your vested balance or $50,000, whichever is less. The advantage is that a 401(k) loan usually doesn’t create taxes or penalties if you repay it on schedule. The interest goes back into your account. The risk is that if you leave your job, the unpaid balance may become due quickly. If you can’t repay it, the loan may be treated as a taxable distribution.

3. In-Service Withdrawal

An in-service withdrawal allows certain employees to withdraw money while still working. Not all plans allow this. Some plans permit it only after age 59½. Others may allow limited withdrawals from after-tax contributions or rollover money. Ask HR or your plan administrator for the summary plan description. That document tells you what your specific plan allows.

Thinking About Quitting to Cash Out?

Some people consider quitting just to cash out 401(k) money. Be careful. Once you leave a job, you may have more access to the account, but taxes and penalties may still apply. After leaving a job, you usually have several options. You may leave the money in the old plan, roll it into a new employer plan, roll it into an IRA, or cash out. Cashing out is often the most expensive option because it can create taxes, penalties, and lost retirement growth.

If you are in your 50s, learn about the rule of 55 before making a decision. The 401(k) rule of 55 may allow penalty-free withdrawals from your current employer’s 401(k) if you leave that job in or after the year you turn 55. This can be useful for early retirement planning, especially if you are asking can I retire at 55. But the rule of 55 is narrow. It usually applies only to the plan connected to the employer you just left, not old 401(k)s or IRAs.

Better Alternatives Before You Cash Out

Before you raid your 401(k), look for less damaging options. You may be able to pause contributions temporarily to increase take-home pay. You may negotiate payment plans with creditors, explore debt relief, reduce expenses, sell unused assets, use a lower-cost personal loan, or build a hardship budget. If the issue is high-interest debt, compare the interest cost with the tax and penalty cost of a withdrawal. Sometimes a 401(k) loan is less damaging than a full withdrawal. Sometimes neither is wise.

Conclusion

Usually, you can’t fully cancel and cash out while still working for the plan sponsor. You can often stop contributions, and you may qualify for a hardship withdrawal from 401(k), 401(k) loan, or in-service withdrawal. Still, early access should be a last resort. Your 401(k) isn’t just money for today. It’s future rent, future healthcare, future freedom, and future stability. Before you cash out, understand the taxes, penalties, and lost growth. Then choose the option that solves today’s problem without creating a larger retirement crisis later.

Related Articles

Can I Withdraw From a 403(b) While Still Employed? 2026 Rules