Every business needs capital to operate, expand, and compete. Whether funding comes from loans, investors, or a combination of both, that capital is never free. Companies must generate enough returns to meet the expectations of those who provide financing. Understanding the true cost of raising and using capital is therefore essential for evaluating investments, measuring performance, and making strategic financial decisions. This is where the concept of Weighted Average Cost of Capital (WACC) becomes especially important. Understanding the WACC meaning helps investors, managers, and analysts determine the minimum return a company must earn on its investments to create value rather than erode it.

What Is the Weighted Average Cost of Capital?

Weighted average cost of capital, often shortened to WACC, is the average return a company must earn to satisfy both its lenders and shareholders. In plain English, WACC is the company’s blended cost of funding. Debt holders expect interest payments.

Deconstructing the WACC Formula

The standard WACC formula looks complicated at first, but it is simply a weighted mix of debt cost and equity cost.

Here is what each variable means.

E is the market value of equity. This means the value investors currently place on the company’s stock, not just the accounting value shown on the balance sheet.

D is the market value of debt. This includes bonds, loans, and other interest bearing obligations.

V is the total value of capital, calculated as E + D.

E / V is the percentage of the company funded by equity.

D / V is the percentage funded by debt.

Re is the cost of equity.

Rd is the cost of debt.

T is the corporate tax rate.

The formula matters because companies rarely use only one source of money. A business may fund itself with shareholder equity, bank loans, bonds, retained earnings, or all of them together. WACC turns that capital mix into one usable hurdle rate.

The Mechanics: Cost of Equity vs. Cost of Debt

1. Finding the Cost of Equity CAPM

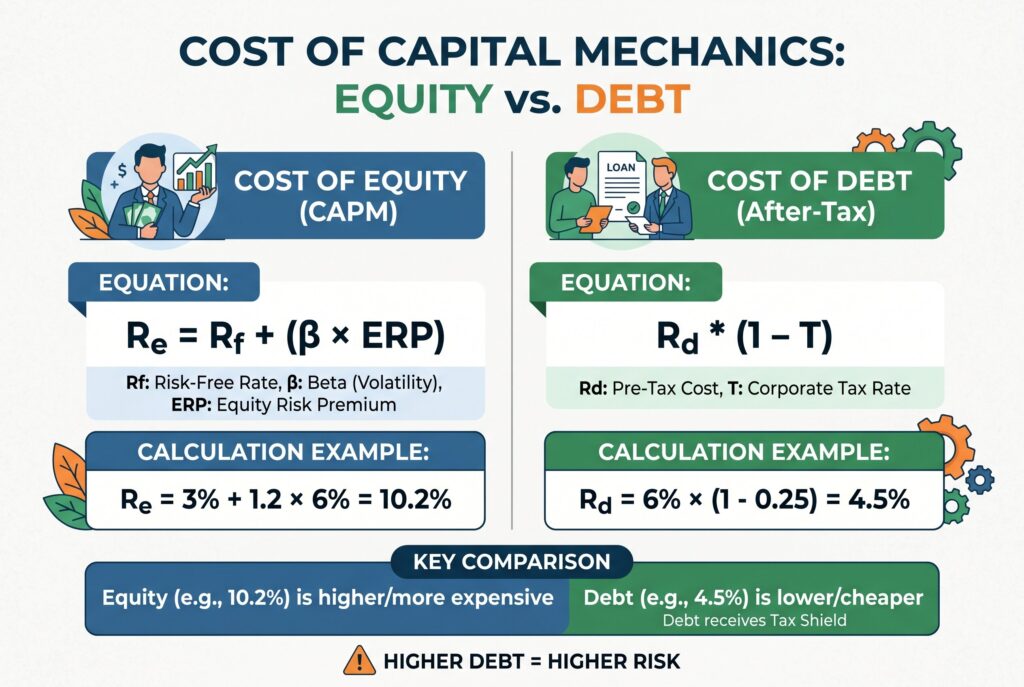

Debt usually has a visible price because loans and bonds have stated interest rates. Equity is harder. Shareholders don’t receive a fixed coupon, so analysts often estimate the cost of equity CAPM.

The CAPM formula is:

Re = Risk Free Rate + Beta × Equity Risk Premium

The risk free rate is often based on long term government bonds. Beta measures how volatile the stock is compared with the market. The equity risk premium reflects the extra return investors demand for owning stocks instead of safer assets. For example, if the risk free rate is 3%, beta is 1.2, and the equity risk premium is 6%, then:

Re = 3% + 1.2 × 6% = 10.2%

That means equity investors would expect roughly 10.2% to compensate them for the risk.

2. Understanding the Cost of Debt

The cost of debt is the interest rate a company pays to borrow money. For a public company, analysts often estimate it by looking at bond yields or current borrowing rates. For a private company, they may use bank loan rates or comparable company credit spreads.

However, debt receives special treatment because interest expense is usually tax deductible. That is why the formula multiplies Rd by (1 − T). This adjustment creates the tax shield WACC benefit.

If a company borrows at 6 percent and its tax rate is 25%, the after tax cost of debt is:

6% × (1 − 0.25) = 4.5%

This is why debt is often cheaper than equity. But too much debt increases bankruptcy risk, refinancing risk, and investor concern. At some point, adding debt can increase WACC rather than lower it.

WACC Calculation Example: A Simple Company

Imagine a company has $60 million in market value of equity and $40 million in debt. Total capital is $100 million. Its cost of equity is 10%. Its pre tax cost of debt is 5%. Its tax rate is 25%.

Equity weight = 60%

Debt weight = 40%

After tax cost of debt = 5% × (1 − 0.25) = 3.75%

WACC = (60%× 10%) + (40% × 3.75%)

WACC = 6% + 1.5%

WACC = 7.5%

This company should only accept projects expected to earn more than 7.5%. A project with a 9% return may create value. A project with a 5% return may destroy value.

Mercedes Benz WACC Case Study

To understand how to calculate WACC in the real world, consider a simplified Mercedes Benz WACC example. The numbers below are illustrative, not official valuation inputs.

Assume Mercedes-Benz Group had a market capitalization of approximately $67.2 billion at the end of 2025 and total debt of approximately $106 billion based on its 2025 annual reporting and market data.

Total capital = $67.2 billion + $106.0 billion = $173.2 billion

E/V = $67.2 billion / $173.2 billion = 38.8%

D/V = $106.0 billion / $173.2 billion = 61.2%

Next, estimate the cost of equity using CAPM. Assume a U.S. risk-free rate of 4.5%, a beta of 1.15, and an equity risk premium of 5.5%.

Re = 4.5% + (1.15 × 5.5%)

Re = 10.83%

Now assume Mercedes-Benz has a pre-tax cost of debt of 5.0% and an effective corporate tax rate of 29%.

After-tax cost of debt = 5.0% × (1 − 0.29)

After-tax cost of debt = 3.55%

Apply the WACC formula:

WACC = (38.8% × 10.83%) + (61.2% × 3.55%)

WACC = 4.20% + 2.17%

WACC = 6.37%

This means a new electric vehicle platform, battery plant, software initiative, or manufacturing expansion would need to earn more than approximately 6.37% to create value under these assumptions.

Disclaimer: This example uses Mercedes-Benz Group financial and market data from 2025. The company’s market capitalization was approximately $67.2 billion at year-end 2025, while debt figures were derived from its 2025 annual reporting. The risk-free rate, beta, equity risk premium, cost of debt, and tax rate are reasonable market assumptions used for illustration. Actual WACC will vary depending on market conditions and the valuation date.

Why WACC Changes Over Time

WACC isn’t fixed. It moves when interest rates, credit spreads, stock volatility, tax rates, and capital structure change. If long term government bond yields rise, the risk free rate rises. That usually pushes the cost of equity higher. If lenders demand higher rates, the cost of debt increases. If the company takes on too much debt, equity investors may demand a higher return because the business becomes riskier. This is why analysts should stress test WACC. A DCF model that uses only one discount rate can create a false sense of precision.

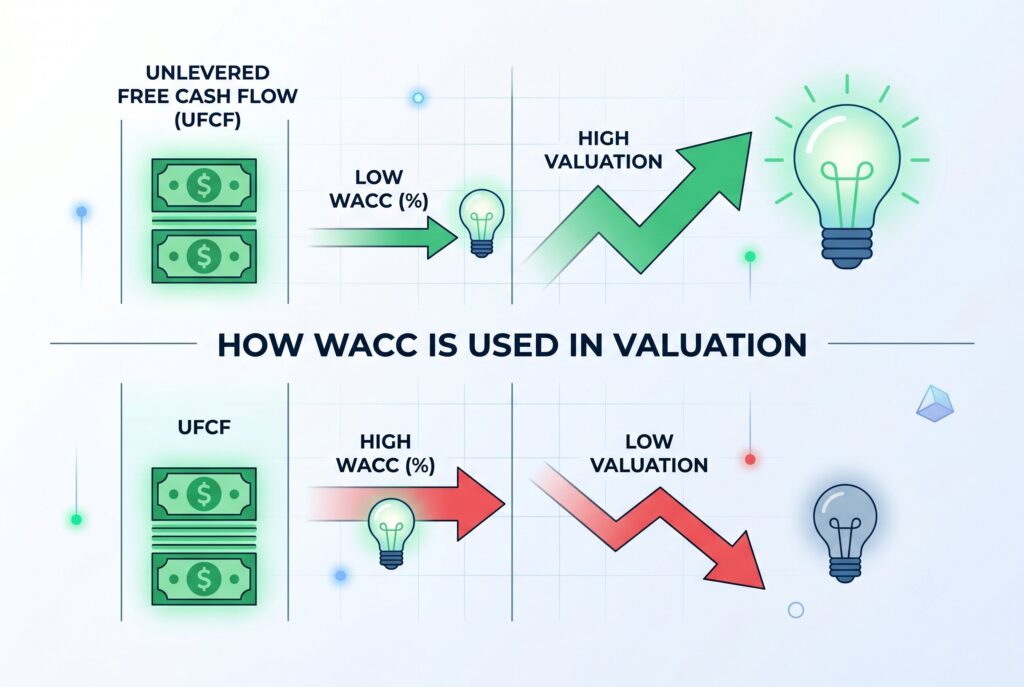

How WACC Is Used in Valuation

In a discounted cash flow model, WACC is used as the discount rate for unlevered free cash flow. It helps convert future cash flows into present value. A lower WACC usually increases valuation because future cash flows are discounted less aggressively. A higher WACC reduces valuation because future cash flows become less valuable today. That makes WACC one of the most important assumptions in corporate finance.

Conclusion

WACC is essential because it tells a company the minimum return required to justify investment. It connects capital structure, investor expectations, tax policy, borrowing costs, and valuation into one number. Still, WACC is only as good as its assumptions. Beta can change. Market risk premiums are estimated. Debt costs shift with interest rates. Tax rules can evolve. For that reason, strong analysts don’t memorize WACC. They understand the moving parts and test how sensitive valuation is to each one.

Related Articles

Free WACC Calculator: Fast & Accurate Corporate Valuation Tool