In corporate finance and valuation, understanding the full value of a business requires looking beyond its stock price alone. Companies are financed through a combination of equity, debt, and cash holdings, all of which affect the economic value available to investors and potential acquirers. For this reason, analysts often focus on measures that capture the value of the entire operating business rather than just the value of shareholders’ equity. This approach is particularly important in mergers and acquisitions, comparable company analysis, and valuation modeling, where assessing the total economic value of a company provides a more complete basis for comparison and decision-making.

What Is Enterprise Value?

It’s the total value of a company’s operating business to all capital providers. The enterprise value formula helps analysts look beyond market capitalization and understand what it would truly cost to acquire the entire company.

Deconstructing the Enterprise Value Formula

The basic enterprise value formula is:

Enterprise Value = Market Capitalization + Total Debt − Cash and Cash Equivalents.

For larger companies with more complex capital structures, analysts often use the expanded version:

Enterprise Value = Market Capitalization + Total Debt + Minority Interest + Preferred Equity − Cash.

Each component has a specific purpose.

- Market capitalization is the equity value of the company in the public market. It equals share price multiplied by shares outstanding.

- Total debt is added because an acquirer effectively takes responsibility for the target’s borrowings. If the company owes banks or bondholders money, that obligation still exists after the acquisition.

- Cash and cash equivalents are subtracted because the buyer gains access to that cash after taking control. In theory, cash can help repay debt or reduce the net purchase cost.

- Minority interest is added when the company consolidates subsidiaries it doesn’t fully own. Preferred equity is added because preferred shareholders have a claim that sits between debt and common equity.

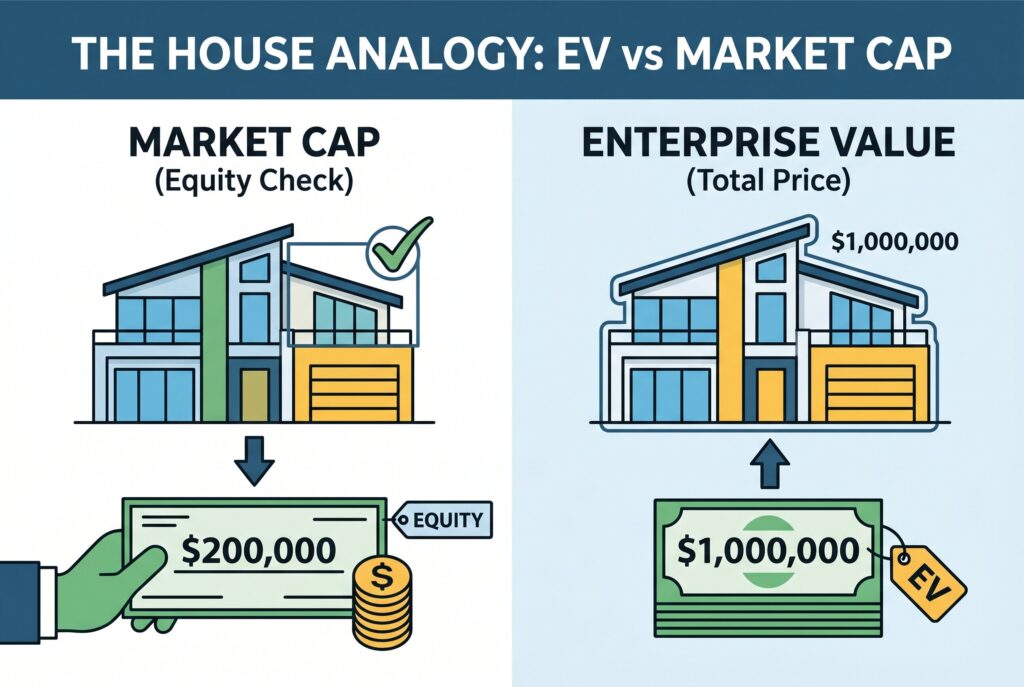

EV vs Market Cap: The Real Estate Analogy

The easiest way to understand EV vs market cap is to think about buying a house. Market cap is like the cash you pay to the seller for their ownership. Enterprise value is the full economic cost of owning the house, including the mortgage you must take over, minus cash or financial assets that come with it.

Imagine a house is worth $1,000,000. The owner has $800,000 of mortgage debt and $200,000 of equity. If you only look at the equity check, the price looks like $200,000. But the true value of the house is still $1,000,000.

Companies work the same way. A business can look cheap based on market capitalization, but if it carries heavy debt and little cash, enterprise value may tell a very different story.

Step by Step Enterprise Value Calculation

Assume a public company has the following profile:

Share price is $40.

Shares outstanding are 50 million.

Total debt is $700 million.

Cash and cash equivalents are $250 million.

Preferred equity is $100 million.

Minority interest is $50 million.

First, calculate market capitalization:

$40 × 50 million shares = $2 billion.

Then apply the expanded formula:

Enterprise Value = $2 billion + $700 million + $100 million + $50 million − $250 million.

Enterprise Value = $2.6 billion.

This means the company’s public equity is worth $2 billion, but the full operating business is valued at $2.6 billion after considering debt, preferred equity, minority interest, and cash.

Step by Step M&A Example

In M&A work, enterprise value calculation can include items that don’t look like traditional debt.

Consider a SaaS company with:

Market cap of $800 million.

Bank debt of $50 million.

Deferred revenue of $30 million.

Cash of $40 million.

At first glance, the simple EV formula gives:

$800 million + $50 million − $40 million = $810 million.

But in a SaaS acquisition, deferred revenue may be treated as a debt-like item. Why? Because customers already paid for services the company still needs to deliver. The buyer inherits that obligation.

Adjusted EV = $800 million + $50 million + $30 million − $40 million.

Adjusted EV = $840 million.

This is why M&A analysts don’t blindly copy balance sheet numbers. They investigate obligations, contract liabilities, working capital targets, leases, pensions, tax liabilities, and other debt like items.

Now consider a manufacturing company with:

Market cap of $500 million.

Bank debt of $120 million.

Equipment lease liabilities of $40 million.

Cash of $60 million.

The simple EV formula gives:

$500 million + $120 million − $60 million = $560 million.

However, in a manufacturing acquisition, lease liabilities may be treated as debt-like items because the buyer inherits the obligation to continue making lease payments for factories, warehouses, or production equipment.

Adjusted EV = $500 million + $120 million + $40 million − $60 million.

Adjusted EV = $600 million.

This shows that enterprise value adjustments aren’t limited to technology or SaaS companies. In manufacturing, analysts often review leases, environmental liabilities, pension obligations, maintenance capex needs, and supplier commitments to understand the true acquisition cost.

The Private Company Gap: Normalizing Financials

Private company valuation is harder because there isn’t a public share price. You can’t simply multiply share price by shares outstanding to calculate market capitalization. Instead, buyers often estimate enterprise value using valuation multiples. They look at comparable public companies or recent transactions, then apply a multiple to the private company’s normalized EBITDA, revenue, or free cash flow.

For example, if similar companies trade at 8 times EBITDA and a private company has $10 million of normalized EBITDA, estimated enterprise value may be:

8 × $10 million = $80 million.

Then the buyer moves from enterprise value to equity value by subtracting debt and adding cash.

If the company has $15 million of debt and $5 million of cash:

Equity Value = $80 million − $15 million + $5 million.

Equity Value = $70 million.

That $70 million is closer to what founders or shareholders may receive before deal costs, taxes, escrows, and working capital adjustments.

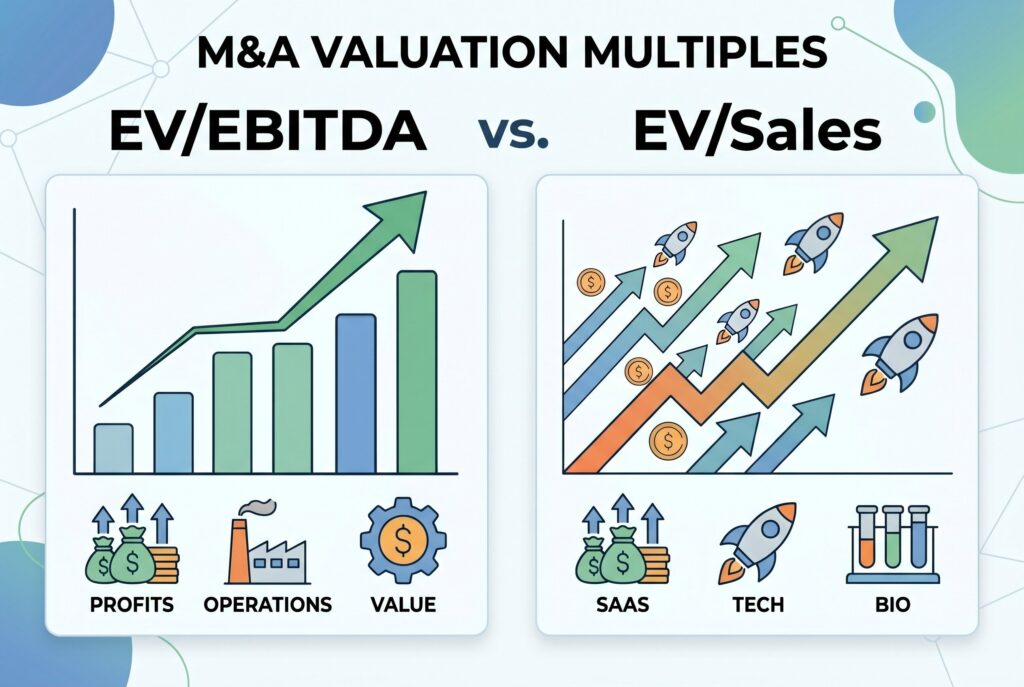

Core M&A Valuation Multiples: EV/EBITDA vs EV/Sales

Enterprise value is most useful when paired with operating metrics. EV/EBITDA is one of the most common M&A valuation multiples. It compares total business value with earnings before interest, taxes, depreciation, and amortization. It’s popular because it reduces the distortion created by different capital structures, tax rates, and depreciation policies.

EV/Sales is often used for companies that don’t yet have positive EBITDA. This is common in high growth technology, SaaS, biotech, and early stage companies. It can be useful, but it’s riskier because revenue doesn’t guarantee profitability.

EV/EBIT may be better for mature businesses where depreciation reflects real asset replacement needs. EV/FCF can be useful when cash conversion matters more than accounting earnings.

Common Mistakes in Enterprise Value Analysis

- The first mistake is using book value of equity instead of market capitalization for public companies. EV is based on market values where possible.

- The second mistake is subtracting all cash without thinking. Some cash may be required for daily operations and shouldn’t be treated as excess.

- The third mistake is ignoring lease liabilities, pensions, deferred revenue, tax exposures, or other debt like items.

- The fourth mistake is confusing enterprise value with purchase price. A final deal price may include control premiums, synergies, escrow holdbacks, working capital adjustments, and negotiation dynamics.

Conclusion

Enterprise value isn’t just a formula. It’s a way to see the full economic cost of owning a business. Market cap shows what common shareholders own. Enterprise value shows what the entire operating company is worth after considering debt, cash, preferred equity, and minority interest.

For investors, EV helps compare companies with different capital structures. For founders, it explains how buyers may value the business. For M&A analysts, it’s the starting point for EV/EBITDA, EV/Sales, comparable company analysis, and acquisition modeling.

A company can look cheap on market cap but expensive on EV if it’s loaded with debt. It can also look expensive on market cap but more attractive if it holds a large cash balance. The best analysts follow the cash, adjust for hidden obligations, and use enterprise value as the bridge between headline price and real takeover economics.