: Pre Tax vs. After Tax Calculation")

Cost of debt is the real price a company pays to borrow money from lenders, banks, bondholders, or other creditors. In simple terms, it’s the return lenders require for taking the risk of giving capital to the business. But the cost of debt formula isn’t just the interest rate written on a loan agreement. For valuation, analysts must separate pre tax cost of debt from after tax cost of debt. Because interest expense is usually tax deductible, debt creates a tax shield that makes its real cost lower than the stated borrowing rate.

The Fundamental Concept: Pre Tax Cost of Debt

Pre tax cost of debt measures the company’s borrowing cost before considering tax savings. There are two main ways to estimate it.

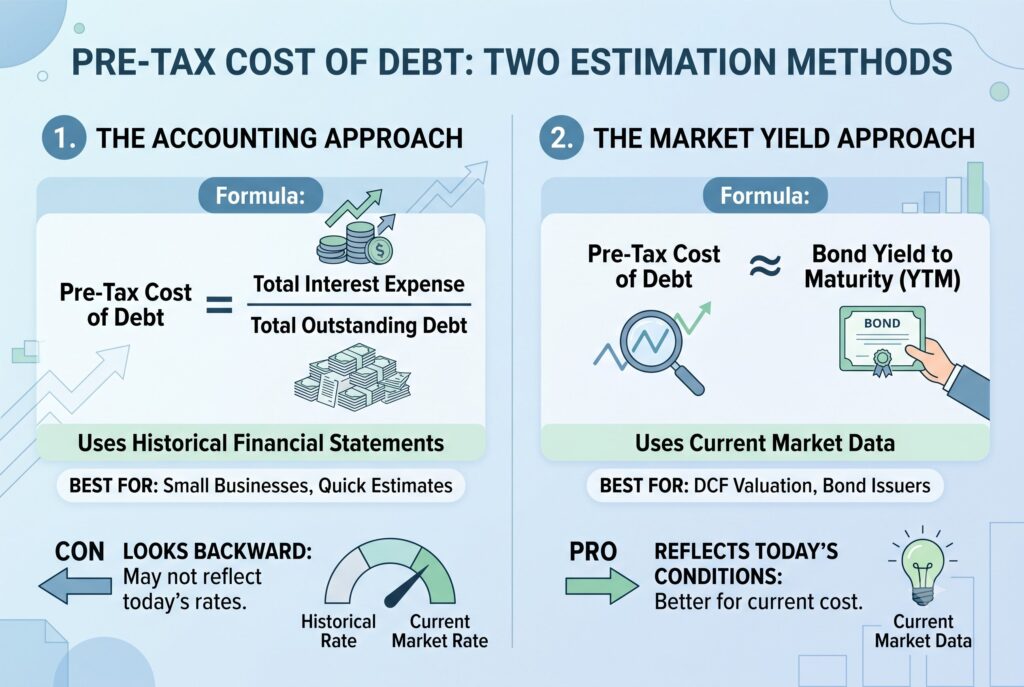

1. The Accounting Approach

The easiest method uses the company’s financial statements.

For example, if a company paid $600,000 in annual interest expense and has $10 million of total debt, its pre tax cost of debt is:

$600,000 / $10,000,000 = 6%

This method is simple and useful for small businesses, private companies, or quick estimates. However, it has one major weakness. It looks backward. It tells you what the company has been paying historically, not what lenders would charge if the company borrowed money today. That difference matters. If interest rates have risen sharply, the historical effective interest rate may understate the company’s current borrowing cost.

2. The Market Yield Approach

For professional valuation, the market yield approach is stronger. Instead of using old accounting data, analysts look at the current yield to maturity on the company’s publicly traded bonds.

If a company’s bonds are trading at a 7% market yield, then 7% is usually a better estimate of current pre tax cost of debt than last year’s average interest rate. This approach reflects today’s credit risk, market conditions, investor expectations, and refinancing environment. It’s especially useful when building WACC for DCF valuation.

The Power of the Tax Shield: After Tax Cost of Debt

Debt is often cheaper than equity because interest expense can reduce taxable income. This tax benefit is called the tax shield.

The after tax cost of debt formula is:

After Tax Cost of Debt = Pre Tax Cost of Debt × (1 − Tax Rate)

Suppose a company borrows $10 million at a 6% pre tax cost of debt and pays a 21% corporate tax rate.

Annual interest expense equals:

$10 million × 6 % = $600,000

Because that interest is deductible, the company saves:

$600,000 × 21% = $126,000 in taxes

So the true after tax cost is:

$600,000 − $126,000 = $474,000

As a % of debt:

$474,000 ÷ $10 million = 4.74%

Or directly:

6% × (1 − 21%) = 4.74%

That 4.74% is the number analysts normally use in WACC.

Why WACC Uses After Tax Cost of Debt

Weighted average cost of capital combines the cost of equity and cost of debt based on how a company funds itself. Since WACC measures the after tax cost of capital to the business, it uses after tax cost of debt, not pre tax cost of debt.

Using pre-tax cost of debt in WACC is a common beginner mistake. Because using the pre-tax rate ignores the value of the tax shield, overstates the company’s discount rate, and can lead to an artificially low DCF valuation. Even a small increase in WACC can reduce a company’s estimated value by millions of dollars.

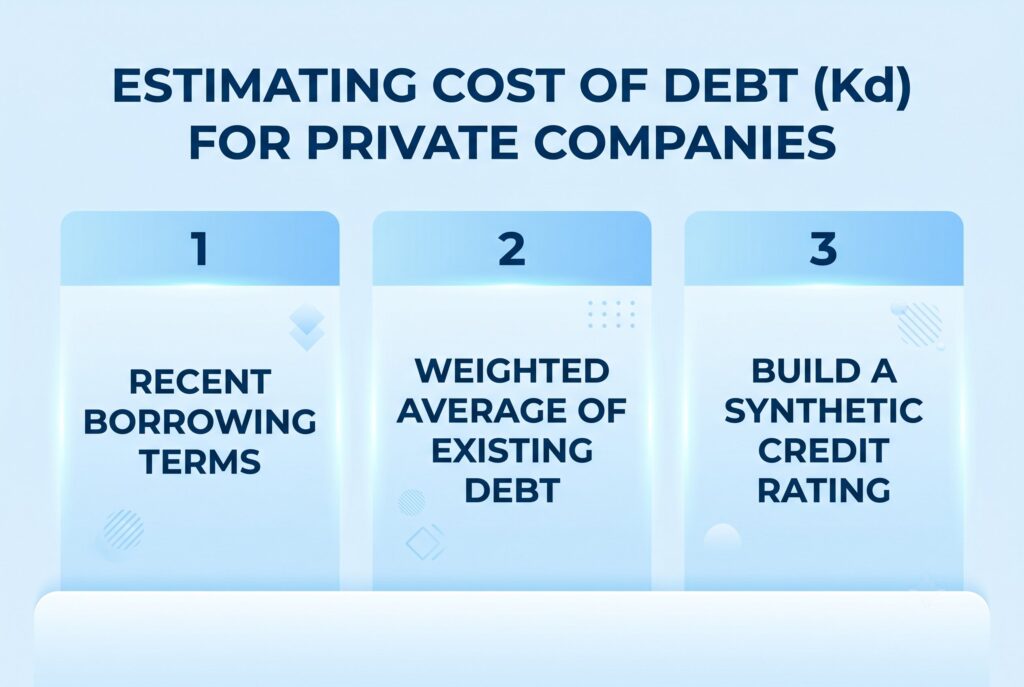

Advanced Execution: Estimating Kd for Private Companies

Private companies usually don’t have publicly traded bonds. That means analysts can’t simply pull a market yield from bond data.

In that case, there are three practical methods.

1. Use Recent Borrowing Terms

If the business recently received a bank loan, equipment loan, or credit facility, the interest rate can provide a useful market based estimate. But check whether the rate is fixed or floating, whether it includes fees, and whether it reflects today’s credit conditions.

2. Use the Weighted Average of Existing Debt

If the company has several loans, don’t simply average the interest rates. Weight each loan by its outstanding balance.

A $5 million loan at 7% matters more than a $200,000 equipment loan at 10%.

A better shortcut is:

This gives a balance weighted effective interest rate.

3. Build a Synthetic Credit Rating

For valuation work, a synthetic rating can estimate what the company would pay if it borrowed today.

Start with the interest coverage ratio:

A higher ratio means the company can cover interest payments more easily, so lenders view it as safer.

Next, map that ratio to an estimated credit rating. A strong coverage ratio may imply an A or BBB profile. A weak ratio may imply a lower rating.

Then add a credit spread to the risk free rate.

Pre Tax Cost of Debt = Risk Free Rate + Credit Spread

This method is especially useful for private company valuation, M&A models, and leveraged buyout analysis.

What to Do With Fees, Floating Rates, and Leases

Real borrowing cost isn’t always clean. Loan origination fees, commitment fees, closing costs, and refinancing costs can increase the effective interest rate. Floating rate debt can also change quickly when benchmark rates move.

If a company has floating rate debt, use the current forward looking rate, not last year’s average rate. If loan fees are material, amortize them into the effective borrowing cost.

Lease liabilities may also matter. In valuation, analysts often treat lease obligations as debt like items because they represent fixed future payment commitments.

Conclusion

Cost of debt isn’t just a formula from a finance textbook. It’s a live measurement of lender confidence, default risk, tax savings, and capital market conditions. The accounting approach is useful for quick estimates. The market yield approach is better for public company valuation. Synthetic credit ratings help when modeling private companies.

For WACC, always use after tax cost of debt because the tax shield reduces the real burden of borrowing. A careful analyst doesn’t stop at the interest rate. They check market yields, tax rates, fees, floating rate exposure, credit spreads, and the company’s current ability to service debt. That precision can make the difference between a clean valuation and a misleading model.