Current assets play a crucial role in a company’s day-to-day operations and short-term financial stability. They represent the resources available to support routine business activities, meet upcoming obligations, and maintain operational flexibility. By examining current assets, investors, creditors, and managers can better assess a company’s liquidity, working capital position, and ability to sustain its short-term financial commitments.

What Are Current Assets?

What are current assets? Current assets are resources a business expects to convert into cash, sell, or use within one year or one normal operating cycle. They appear on the balance sheet and show how much short term financial fuel a company has available.

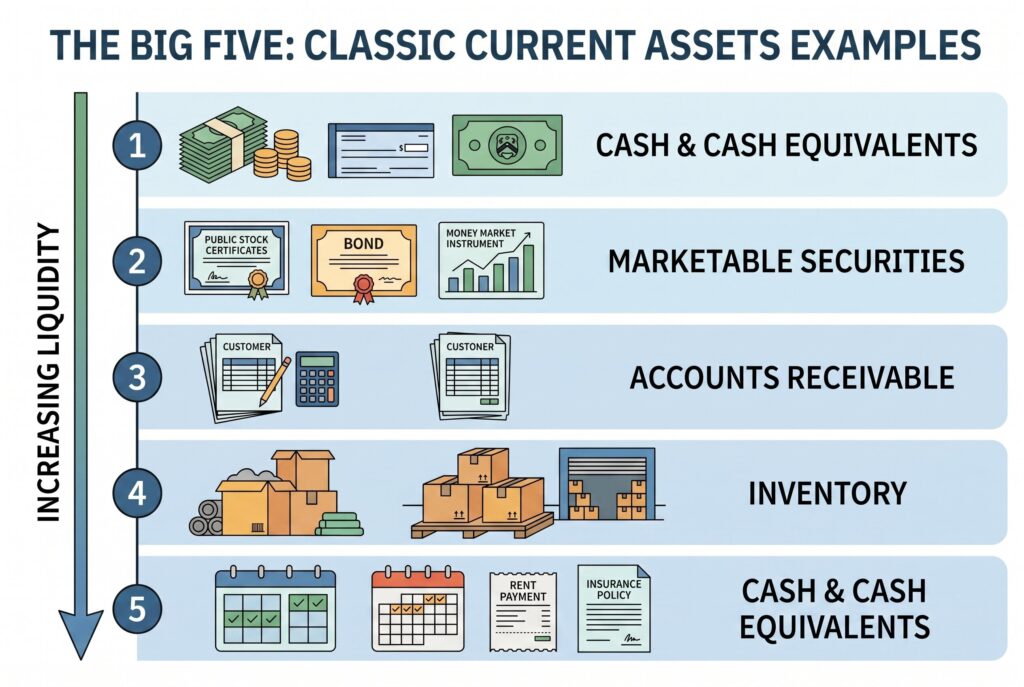

The Big Five: Classic Current Assets Examples

Current assets are usually listed on the balance sheet in order of liquidity, from easiest to hardest to convert into cash.

Cash and Cash Equivalents

Cash and cash equivalents are the most liquid current assets. This category includes cash on hand, checking accounts, savings accounts, and short-term instruments such as Treasury bills. Businesses can use these funds immediately to pay vendors, employees, taxes, or loan obligations.

Marketable Securities

Marketable securities are short-term investments that can typically be sold quickly in the financial markets. Examples include publicly traded stocks, bonds, and money market instruments. While not as liquid as cash, they can usually be converted into cash within a few days.

Accounts Receivable

Accounts receivable represents money owed to a business by its customers for goods or services that have already been delivered. When payment is expected within normal credit terms, such as Net 30 or Net 60, the receivable is classified as a current asset.

Inventory

Inventory consists of raw materials, work in progress, and finished goods that a company intends to sell. Although inventory has value, it is less liquid than cash or receivables because it must first be sold before it can generate cash.

Prepaid Expenses

Prepaid expenses are payments made in advance for benefits that will be received in the future. Common examples include prepaid rent, insurance premiums, software subscriptions, and service contracts. They qualify as current assets because the associated benefits are expected to be consumed within the next year.

The Classification Checklist: Answering Your Biggest Questions

Is inventory a current asset?

Yes, inventory is a current asset when the business expects to sell it within one year or one operating cycle. Retailers, manufacturers, farms, restaurants, and wholesalers often carry inventory as a major current asset. However, inventory can be risky. A warehouse full of slow moving products may look strong on the balance sheet, but it won’t help payroll tomorrow unless customers buy it. Obsolete inventory can trap cash and weaken liquidity.

Is accounts receivable a current asset?

Yes, accounts receivable is a current asset if customers are expected to pay within one year. It represents future cash that the business has already earned. Still, not all receivables are equal. A receivable from a reliable customer due in 30 days is much stronger than an overdue invoice from a struggling customer. Smart companies track receivables aging to avoid overstating liquidity.

Is equipment a current asset?

No, equipment isn’t a current asset. Machinery, vehicles, computers, factory tools, and office equipment usually serve the business for more than one year. These are classified as noncurrent assets or fixed assets. Equipment is also depreciated over time, while most current assets aren’t depreciated. This distinction matters because equipment supports long term operations, while current assets support short term liquidity.

Current Assets vs. Liquid Assets: The Dangerous Mix Up

Many business owners assume current assets and liquid assets mean the same thing. They don’t.

Liquid assets are assets that can be turned into cash almost immediately without losing much value. Cash, cash equivalents, and many marketable securities are liquid assets. Current assets are broader. They include liquid assets, but they also include inventory, receivables, and prepaid expenses. These may be useful, but they aren’t always instantly spendable. For example, $100,000 in cash can pay employees today. But $100,000 in inventory can’t pay employees unless the business sells it first. That is why analysts often use the quick ratio, which removes inventory from the calculation, to test stronger liquidity.

The rule is simple: every liquid asset is usually a current asset, but every current asset isn’t liquid.

Why Current Assets Matter for Working Capital

Current assets are the foundation of working capital.

The formula is:

Working Capital = Current Assets − Current Liabilities

If current assets exceed current liabilities, the business has more short term resources than short term obligations. That usually means stronger financial flexibility.

If current liabilities exceed current assets, the company may struggle to pay bills on time, even if it owns valuable long term assets. A business can own buildings, equipment, and land yet still face a cash crunch if it doesn’t have enough current assets.

This is why lenders, investors, and CFOs study current assets closely. They reveal whether a company can survive short term pressure without selling long term assets or raising emergency financing.

The CFO Playbook: Why Tracking This Matters

Tracking current assets isn’t only an accounting task. It’s a management discipline.

- First, current assets influence borrowing power. Lenders often review current ratio, quick ratio, cash reserves, receivables quality, and inventory levels before approving credit lines. A business with strong current assets usually looks safer to lenders.

- Second, current assets create strategic flexibility. Cash and marketable securities let a company buy discounted inventory, hire talent, invest during a downturn, or acquire a competitor when opportunities appear.

- Third, current assets protect against shocks. Slow sales, late customer payments, supplier delays, and recession pressure are easier to handle when the company has enough cash and collectible receivables.

- Fourth, current assets reveal operational weakness. Too much inventory may signal overbuying. Too many receivables may signal weak collections. Too much prepaid expense may reduce immediate liquidity. The balance matters.

Conclusion

Current assets show whether a business has enough short term resources to keep operating smoothly. The smartest approach is to review cash, receivables, inventory, prepaid expenses, current ratio, quick ratio, and working capital together. When current assets are managed well, a business doesn’t just survive short term pressure. It gains the flexibility to grow, borrow, invest, and act before competitors can.