vs 403(b): Which Government Retirement Plan Is Better?")

If you’re comparing 414(h) vs 403(b), you’re probably a teacher, firefighter, state employee, or another public worker trying to make sense of a benefits package that feels more confusing than helpful. That’s normal. Government retirement plans often use unfamiliar labels, and it can sound like you’re supposed to pick one winning option. In reality, that usually isn’t the right way to think about it. For many public employees, these two plans serve different jobs inside the same retirement strategy.

That’s the key shift. A 414(h) retirement plan is often tied to your pension system and handled through mandatory payroll deductions, while a 403(b) is usually a voluntary savings account you can use to build extra retirement assets. Once you understand that difference, the question becomes less about either or and more about how both plans can work together.

The Short Answer: It Isn’t Either Or, It’s Both

For most public employees, the best answer isn’t choosing between a 414(h) plan and a 403(b). It’s understanding that they usually do different things. A 414(h) retirement plan is commonly part of a government pension arrangement. In many cases, contributions are mandatory, and the plan helps fund a defined benefit pension that may pay you monthly income for life in retirement. A 403(b), on the other hand, is usually a voluntary account that works more like a personal investment bucket. You choose whether to contribute, how much to save, and how to invest the money.

That means one plan is often building your pension foundation, while the other gives you flexibility and extra growth potential. So when people ask which government retirement plans are better, the honest answer is that they’re usually strongest together, not in competition.

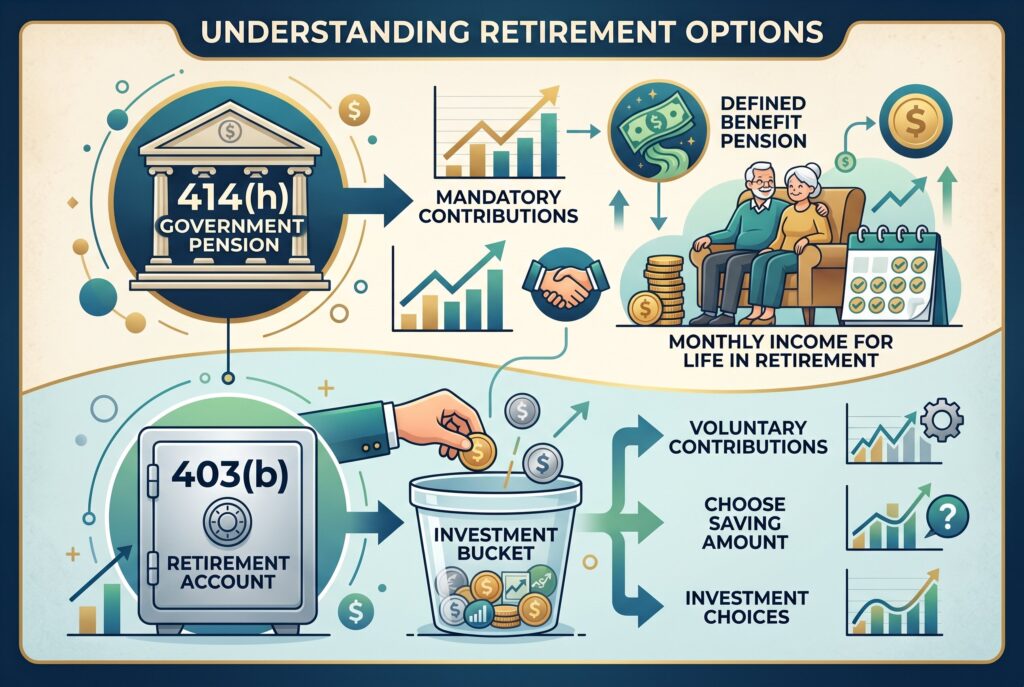

What Is a 414(h) Retirement Plan? The Mandatory Pension

A 414(h) retirement plan is a public-sector retirement arrangement tied to government employment. It’s most closely associated with mandatory employee contributions that are treated under special tax rules.

The phrase 414(h) employer pick up is the part that confuses people most. Here’s the simple version. Even though the money comes out of your paycheck, the employer “picks up” the contribution for tax purposes. That’s why so many public employees ask, is 414(h) pre tax? At the federal level, the answer is usually yes. The contribution is generally treated as pre-tax for federal income tax purposes, which lowers current taxable wages.

But the bigger story is what the money is funding. In many public systems, these mandatory contributions support a defined benefit pension. That means your eventual retirement income may be based on a formula, often involving years of service and salary, rather than just the performance of an investment account. In other words, the payout is usually designed to provide guaranteed monthly income instead of a single account balance you manage on your own. That’s what makes the 414(h) plan feel different from private-sector retirement accounts. It’s usually not about optional savings behavior. It’s about participating in the pension structure required by your government employer.

What Is a 403(b) Plan? The Voluntary Supplement

What is a 403b? A 403(b) is a tax-advantaged retirement account designed mainly for employees of public schools, certain nonprofits, and some ministers. Functionally, it’s very similar to a 401(k), but it serves a different slice of the workforce. If you work in a school district, university, hospital nonprofit, or other eligible public-service environment, this is often the main voluntary retirement savings account offered alongside your pension or other employer plan.

Unlike a 414(h) setup, the 403(b) is usually optional. You decide whether to contribute, and in many cases you choose the investment options inside the account. That means your eventual retirement value depends on how much you save, how consistently you contribute, and how the investments perform over time. This is why the 403(b) is often best understood as a supplement, not a replacement, for pension-style benefits. It gives you personal control and asset growth potential that a formula-driven pension may not provide on its own.

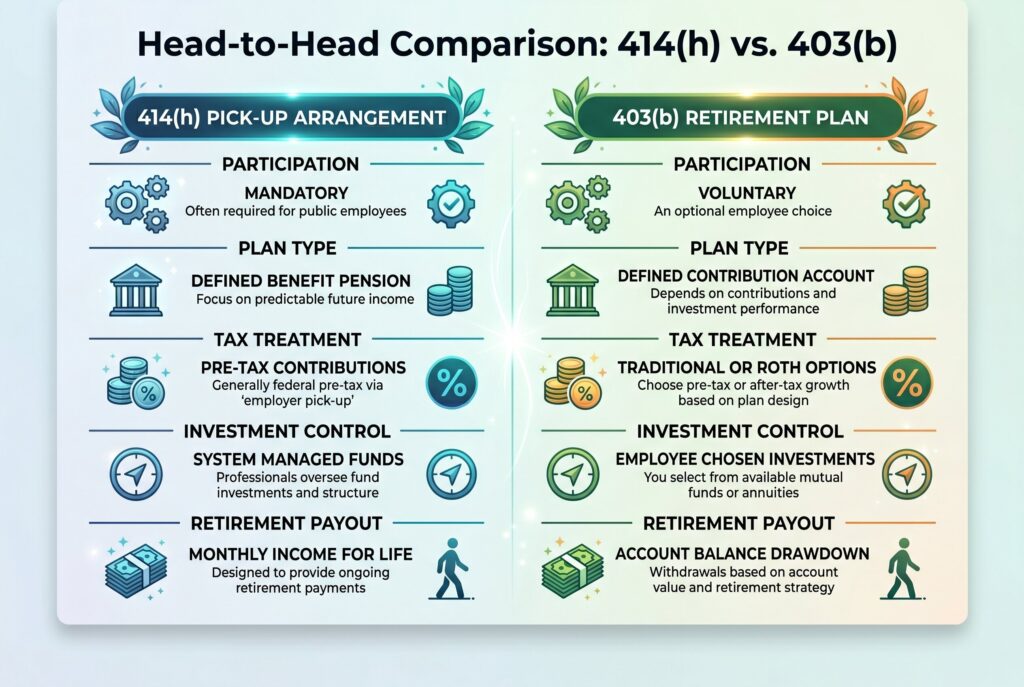

Head to Head Comparison: 414(h) vs. 403(b)

| Category | 414(h) | 403(b) |

|---|---|---|

| Participation | Usually mandatory (public retirement system) |

Usually voluntary |

| Plan Type | Often supports defined benefit pension |

Defined contribution account |

| Tax Treatment | Generally pre-tax via employer pick-up |

Pre-tax or Roth (after-tax) options |

| Investment Control | Managed by retirement system |

Employee chooses investments |

| Retirement Payout | Typically monthly pension income |

Account balance withdrawn per strategy |

Should You Invest in a 403(b) if You Already Have a 414(h)?

In many cases, yes. A pension can provide valuable stability, but it rarely replaces your entire working income. That’s where a 403(b) becomes important. It helps bridge the gap between pension income and the lifestyle you may actually want in retirement. It also gives you a pool of assets that is more flexible than a strict pension formula.

This matters for teacher retirement options and other public-sector careers because a pension alone may not cover travel goals, healthcare uncertainty, inflation pressure, or the desire to retire earlier than the full pension formula rewards. A 403(b) helps build the liquid side of your retirement picture.

Contribution limits matter here too. The 403(b) contribution limits 2026 are part of the practical planning question because the account can become a major wealth-building tool over time. If you already have the mandatory pension side covered through a 414(h) structure, the 403(b) is often where you gain flexibility, growth, and more personal control over how much extra you’re setting aside.

Visualize Your Retirement Strategy

The smartest way to think about these plans is to picture them as two different income engines. Your 414(h) plan helps create a pension foundation. That’s the predictable income layer. Your 403(b) builds an investment layer on top of that foundation. That’s the flexible wealth layer. One helps protect you from outliving income. The other helps you manage opportunity, inflation, and choice. When both are used well, they create a more complete retirement strategy than either one could provide alone. That’s especially true in government retirement plans, where pension benefits are valuable but often not enough to cover every future need by themselves.

Conclusion

The best answer to 414(h) vs 403(b) is usually not choosing one and ignoring the other. It’s understanding how each plan solves a different retirement problem.

The 414(h) retirement plan gives many public employees a pre-tax, pension-focused foundation. The 403(b) gives them the chance to build additional savings, personal flexibility, and investment growth. That’s why asking for 414(h) pre tax is important, but it’s only one piece of the bigger strategy. The tax advantage helps today, while the 403(b) helps expand what retirement can look like tomorrow.

If you’re eligible for both, the strongest move is usually to learn your pension formula first, then decide how much additional security and flexibility you want to build through your 403(b). That’s how public employees turn confusing paperwork into a real long-term retirement plan.