A free BPS calculator is the fastest way to turn confusing financial language into clear numbers. If you’re reading about mortgage rates, Federal Reserve moves, ETF fees, bond yields, or business loan pricing, you’ll often see rates described in basis points instead of plain percentages. That sounds technical, but the math is simple. One basis point equals 0.01%, and 100 basis points equals 1%. A basis point calculator helps you convert those small rate changes instantly so you can understand what they actually mean for your money.

These days, basis points matter because small rate changes can still create large financial consequences. A 25 BPS move may seem tiny, but on a mortgage, a business loan, or a retirement portfolio, that difference can add up quickly. That’s why understanding basis points isn’t just useful for bankers or traders. It’s useful for anyone comparing loans, savings rates, investment fees, or financial headlines.

What Is a Basis Point? BPS Meaning Explained

What is a basis point? A basis point is one one-hundredth of one percentage point. In other words, 1 BPS equals 0.01%. The term BPS meaning is simply “basis points,” and traders sometimes pronounce it as “bips.”

The reason basis points exist is precision. Percentages can create confusion when people talk about rate changes. For example, if a loan rate is 5% and someone says it increased by 1%, that sentence isn’t perfectly clear. It could mean the rate rose from 5% to 6%, or it could mean the rate increased by 1% of 5%, which would only move it to 5.05%.

Basis points remove that confusion. If the rate rises by 100 basis points, it means the rate moved from 5% to 6%. If it rises by 5 basis points, it means the rate moved from 5% to 5.05%. That’s why banks, lenders, investors, and central banks use basis points when they discuss interest rates, yields, spreads, and fees.

BPS Calculator and 2026 Financial Impact

BPS Calculator and 2026 Financial Impact

Convert basis points into a percentage and estimate the dollar impact on a balance, loan, investment, or other principal amount. This calculator helps show why even a small BPS change can matter in 2026 financial planning.

A basic BPS calculator converts basis points into percentages. A stronger basis point calculator also helps you understand the dollar impact. For example, 50 BPS equals 0.50%. On a $10,000 balance, that equals $50 per year. On a $500,000 loan, that same 50 BPS difference becomes much more serious. This is why basis points calculators are so helpful. They don’t just answer “what is 50 BPS?” They help you see why that number matters.

The most useful formula for dollar impact is:

So if you want to calculate 25 BPS on $200,000:

That means 25 basis points equals $500 on a $200,000 amount before considering compounding, loan amortization, or time.

BPS to Percentage Conversion Table

Here is a quick conversion table for common values:

1 BPS = 0.01%

5 BPS = 0.05%

10 BPS = 0.10%

25 BPS = 0.25%

50 BPS = 0.50%

75 BPS = 0.75%

100 BPS = 1.00%

150 BPS = 1.50%

200 BPS = 2.00%

500 BPS = 5.00%

This is the easiest way to remember basis points meaning: divide the number of basis points by 100 to get the percentage. If you want to go the other direction, multiply the percentage by 100 to get basis points.

How to Calculate Basis Points Manually

You don’t always need a basis points calculator. The manual math is simple once you know the conversion.

To convert basis points to a percentage:

To convert a percentage change to basis points:

For example, if an interest rate rises from 4.75% to 5.25%, the change is 0.50 percentage points. Multiply 0.50 by 100, and the answer is 50 basis points. If an ETF fee falls from 0.60% to 0.10%, the difference is 0.50 percentage points, or 50 BPS. This is what basis points really mean in practical finance: they’re a clean way to describe changes in rates, fees, yields, and spreads without using vague percentage language.

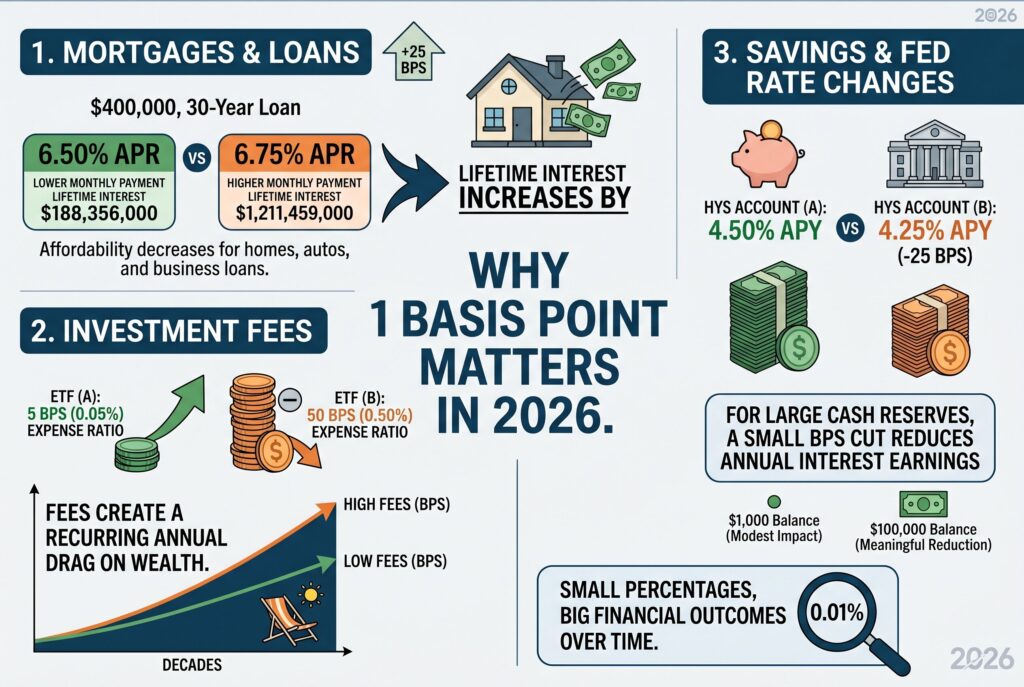

Why 1 Basis Point Matters in 2026

Mortgages and Loans

In mortgages, even a small basis point change can affect affordability. A 25 BPS increase from 6.50% to 6.75% may not look dramatic, but over a 30 year mortgage, it can raise monthly payments and increase lifetime interest by thousands of dollars. The same logic applies to business loans, auto loans, student loans, and credit lines. If the loan balance is large, even a 10 BPS or 25 BPS change can matter.

Investment Fees and Expense Ratios

Basis points are also important when comparing investment fees. An ETF with a 5 BPS expense ratio costs 0.05% per year. An ETF with a 50 BPS expense ratio costs 0.50% per year. That difference may look small, but over decades, higher fees can quietly reduce retirement wealth. A 45 BPS gap isn’t just a tiny decimal. It’s a recurring annual drag on your invested assets.

Savings Accounts and Fed Rate Changes

When the Federal Reserve raises or cuts rates, banks often adjust savings account APYs, CD yields, and lending rates. If a high yield savings account drops from 4.50% to 4.25%, that is a 25 BPS cut. For a small balance, the impact may be modest. For a large cash reserve, that change can reduce annual interest by a meaningful amount.

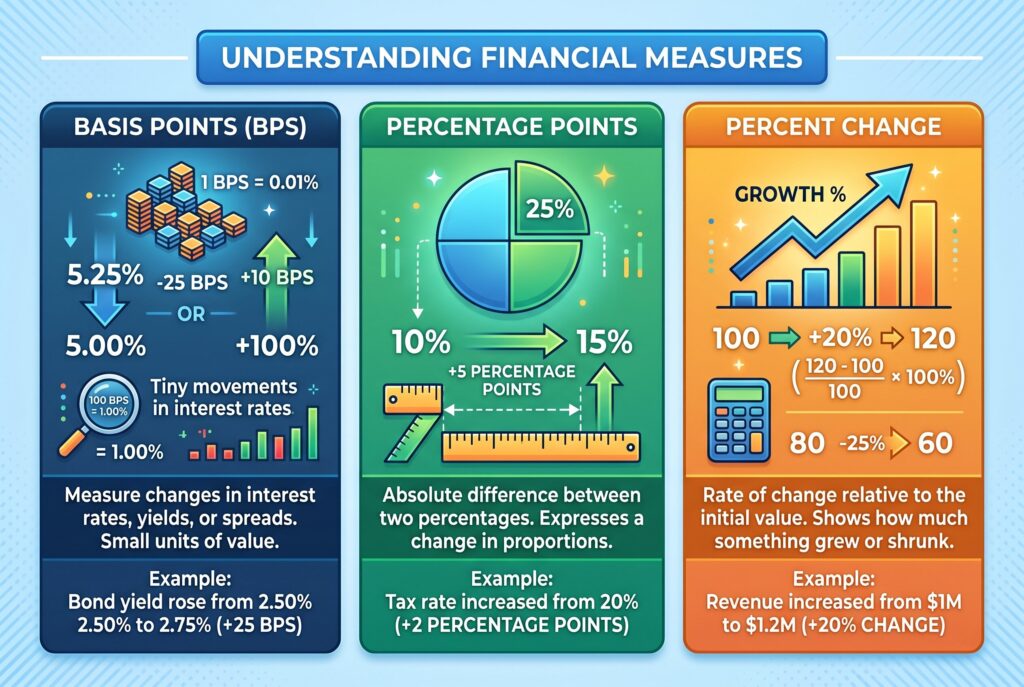

Basis Points vs Percentage Points vs Percent Change

This is one of the most important distinctions. Basis points measure absolute changes in percentage rates. Percentage points do the same thing, but basis points are more precise for small movements. Percent change measures relative movement.

For example, if a rate moves from 4% to 5%, that is a 1 percentage point increase. It’s also a 100 basis point increase. But relative to the original 4%, it’s a 25% increase. All three statements can be true, but they don’t mean the same thing. This is why financial professionals use basis points. They reduce ambiguity and make rate changes easier to compare.

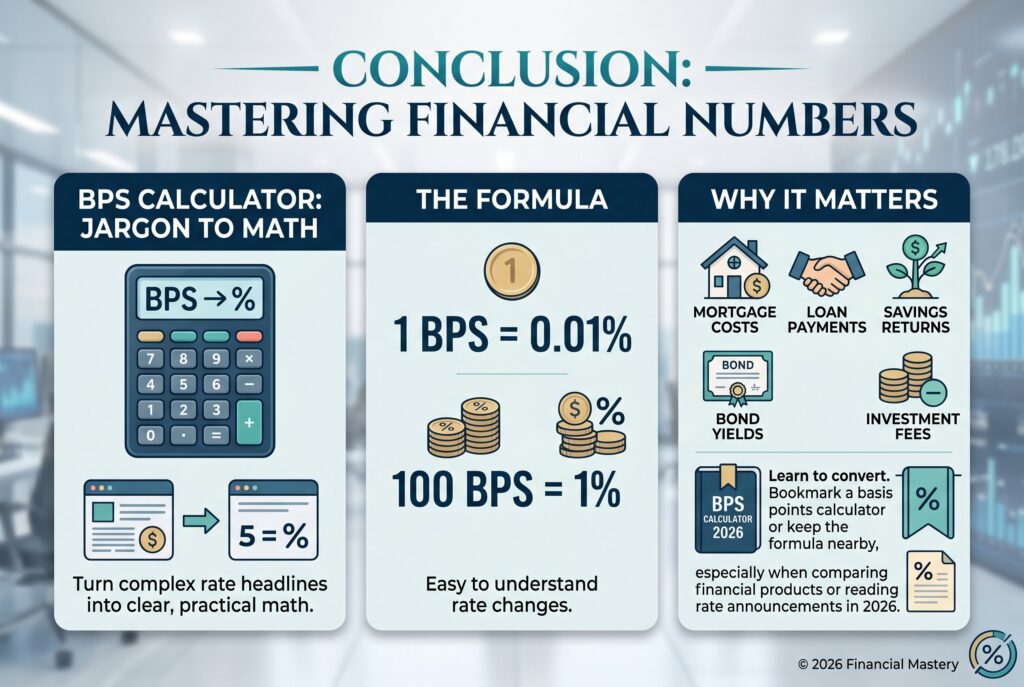

Conclusion

A BPS calculator is useful because it turns financial jargon into clear, practical math. Once you know that 1 BPS equals 0.01% and 100 BPS equals 1%, rate headlines become much easier to understand. Basis points may look tiny, but they can change mortgage costs, loan payments, savings returns, bond yields, and investment fees. That’s why learning how to convert them is worth it. Bookmark a basis points calculator or keep the formula nearby, especially when comparing financial products or reading rate announcements.