Confusing APR vs APY can cost you real money. One number usually shows what you pay when borrowing. The other shows what you earn when saving. The difference between APR and APY comes down to fees and compounding. In 2026, when people compare credit cards, mortgages, personal loans, CDs, and high-yield savings accounts, knowing which number you’re looking at can protect your wallet.

APR vs. APY: The Core Differences

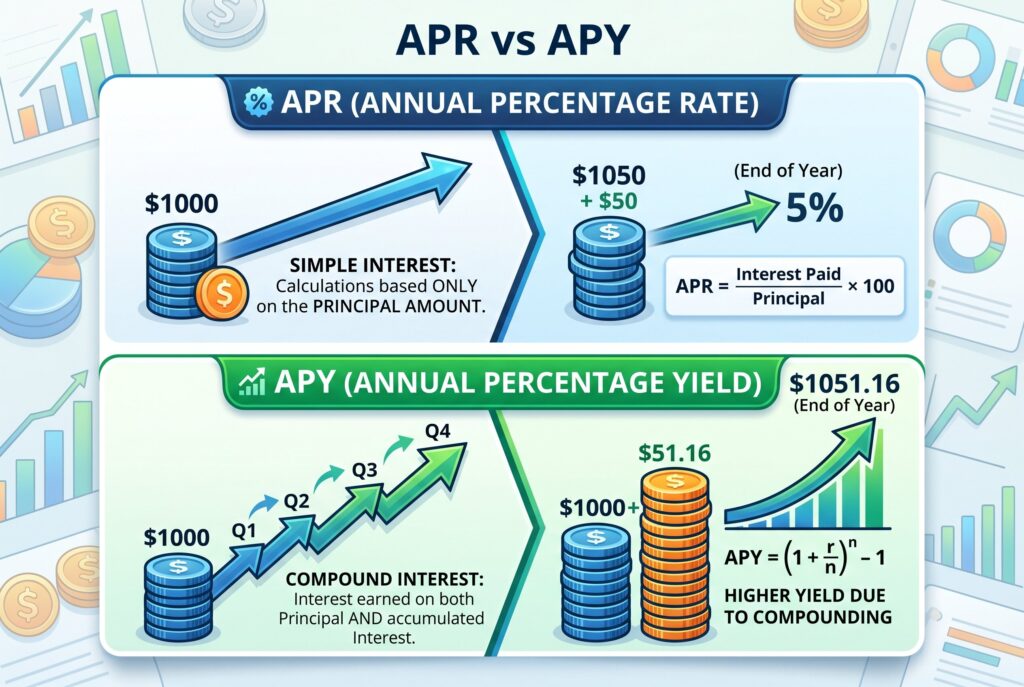

APR measures borrowing cost. APY measures earning power.

APR is used for credit cards, mortgages, auto loans, personal loans, and other debt products. APY is used for savings accounts, certificates of deposit, money market accounts, and other deposit products.

APR doesn’t show the full effect of compounding. APY does. That is why APY is usually higher than the stated interest rate when interest compounds monthly or daily.

The best case for APR is low. A lower APR means borrowing costs less. The best case for APY is high. A higher APY means your money grows faster.

What is APR? The True Cost of Borrowing

APR stands for Annual Percentage Rate. It tells you the annual cost of borrowing money, expressed as a percentage. APR is more useful than a simple interest rate because it may include additional borrowing costs, such as origination fees, certain closing costs, or lender charges. This is especially important for mortgages, auto loans, and personal loans.

For example, a loan may advertise a 7% interest rate, but once fees are included, the APR may be 7.6%. That APR gives a more realistic picture of the cost. The difference between APR and interest rate is that the interest rate usually shows only the cost of borrowing the principal. APR gives a broader annual cost, though it still doesn’t fully show compounding in the same way APY does. For credit cards, APR matters most if you carry a balance. If you pay your balance in full every month, purchasing APR may not affect you much. But if you carry debt, a high APR can make balances grow quickly.

What is APY? The Magic of Compounding

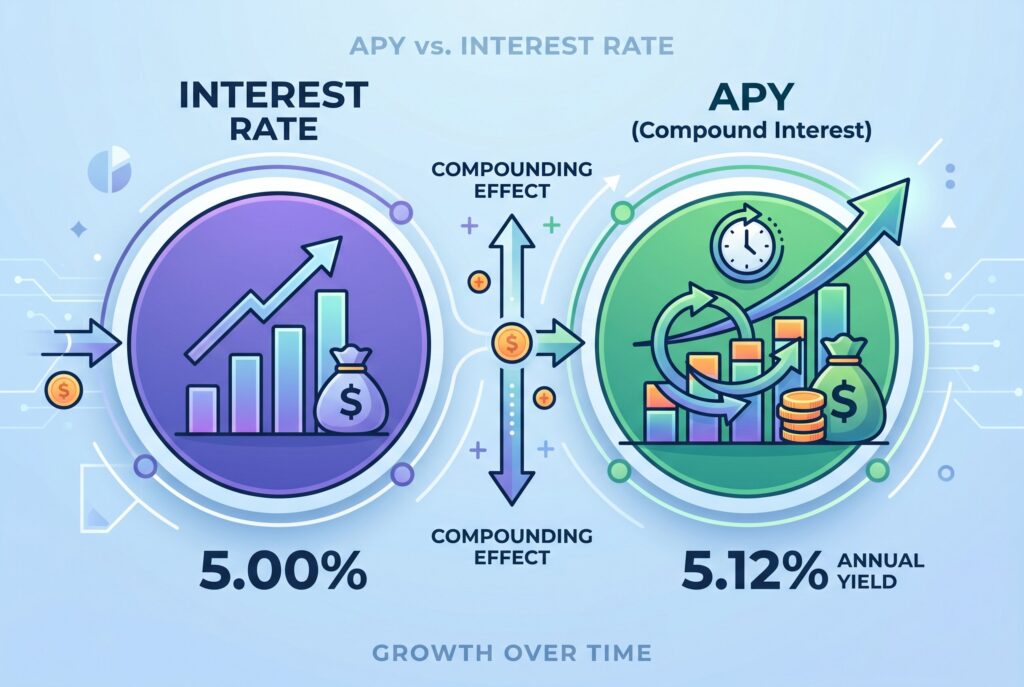

What does APY mean? APY stands for Annual Percentage Yield. It shows how much you can earn in one year after compounding is included. Compounding means you earn interest on your original deposit and then earn interest on the interest. The more often interest compounds, the more powerful APY becomes.

For example, daily compounding usually produces more earnings than annual compounding if the stated interest rate is the same. That is why APY vs interest rate matters. The interest rate tells you the base rate. APY tells you the real annual earning effect after compounding.

Interest rate vs APY is especially important when comparing high-yield savings accounts, CDs, and money market accounts. A higher APY generally means better earning potential, as long as fees, minimum balances, and withdrawal rules don’t cancel out the benefit.

Dividend rate vs APY works similarly for credit unions. A dividend rate may show the stated payout rate, while APY shows the annual return after compounding.

Interactive Simulator: APR vs. APY Compounding Impact

An APR vs APY simulator should let users enter a balance, rate, compounding frequency, and time period. For borrowing, it can show how much interest builds on a loan or credit card balance. For saving, it can show how much money grows with APY.

For example, $10,000 in a high-yield savings account with 4.5% APY could earn about $450 in one year before taxes. But $10,000 in credit card debt at 24% APR can become expensive fast if you only make minimum payments. A simulator makes the lesson clear: APY is your friend when you save, while APR can become a burden when you borrow.

The Bank Marketing Trick: Why Institutions Use Both

Banks and lenders use APR and APY because each number presents financial products differently. Savings accounts advertise APY because compounding makes the number look stronger. A 4.5% APY sounds more attractive than a lower simple interest rate.

Loans and credit cards advertise APR because APR is usually easier for borrowers to compare and may look less scary than a compounded borrowing cost. This doesn’t mean the terms are dishonest. It means you need to know what each one measures. Before opening an account or signing a loan, always ask: is this APR or APY?

Real-World 2026 Examples

The Credit Card Debt Trap APR

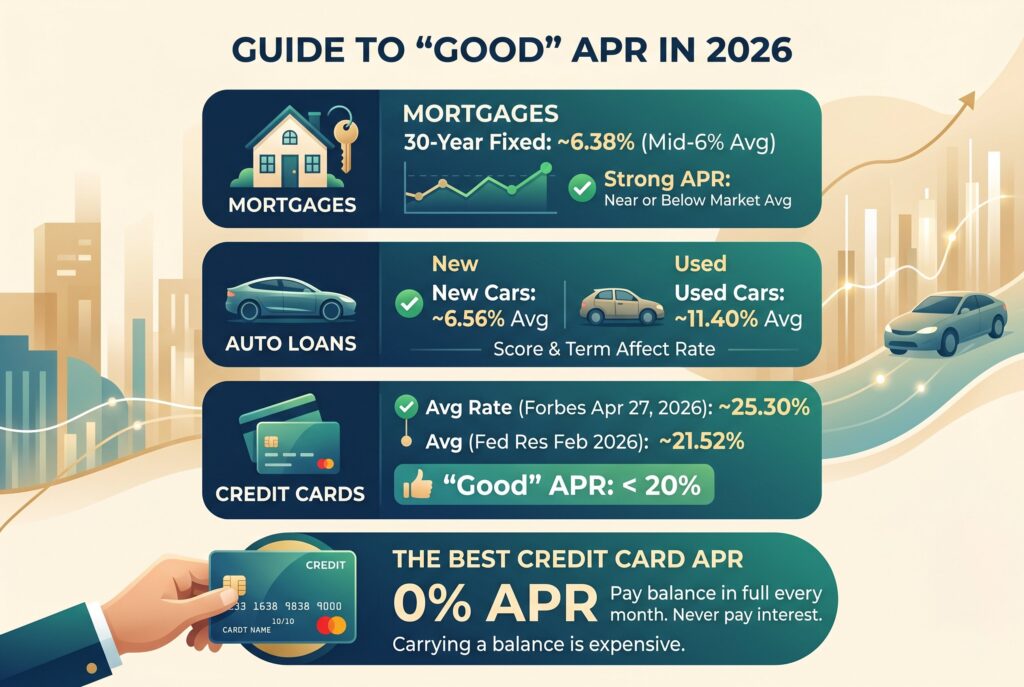

Imagine a credit card has a 24% APR. If you carry a $5,000 balance and only make small payments, interest can pile up quickly. Credit card interest is often calculated using an average daily balance, so the cost can feel invisible until the balance stops going down. This is why what is a good APR for a credit card depends on your credit profile and market conditions, but lower is always better. A good APR for credit card borrowing is one that keeps interest manageable, especially if you ever carry a balance.

High-Yield Savings Accounts APY

Now imagine you deposit $10,000 into a high-yield savings account with 4.5% APY. If the account has no monthly fee and the APY stays stable, your money earns interest while remaining accessible. That is the power of APY. It rewards patience and compounding.

Conclusion

APR vs APY isn’t just a finance vocabulary lesson. It affects how much you pay on debt and how much you earn on savings. Before choosing any financial product, ask whether the rate is APR or APY. For loans and credit cards, look for a low APR. For savings, CDs, and deposit accounts, look for a high APY. The number that looks best in an ad isn’t always the number that matters most. Know what you pay, know what you earn, and let the math work for you instead of against you.