")

The HSA vs FSA decision can feel confusing because both accounts help you pay for healthcare with tax-advantaged dollars. But the difference between HSA and FSA is much bigger than the names suggest. One is built for long-term growth and portability. The other is designed for short-term, predictable medical spending. In 2026, with healthcare costs still rising, choosing the right account can help you avoid wasted money, reduce taxes, and plan smarter during Open Enrollment.

What Is an HSA? The Long-Term Growth Engine

An HSA is a personal healthcare savings account available only if you’re enrolled in an HSA-qualified HDHP. Unlike an FSA, the account belongs to you. If you leave your job, retire, or change employers, the HSA stays with you.

The HSA’s biggest advantage is its triple tax benefit. Contributions can be tax-free or tax-deductible. Growth inside the account can be tax-free. Withdrawals are tax-free when used for qualified medical expenses.

That makes an HSA more than a spending account. It can become a long-term healthcare reserve. If you don’t need the money this year, you can let it roll over. If your provider allows investing, you may be able to invest HSA funds in mutual funds, ETFs, or other options.

For healthy workers, high earners, and people who want to build a future medical safety net, an HSA can quietly become one of the most powerful accounts in a financial plan.

What Is an FSA? The Short-Term Budgeting Tool

How does FSA work? An FSA lets you set aside pre-tax dollars from your paycheck to pay for eligible healthcare costs during the plan year. Common uses include copays, prescriptions, dental work, vision care, therapy, diagnostic imaging, and other qualified medical expenses.

The FSA’s strength is predictability. If you know you’ll spend money on monthly prescriptions, glasses, braces, physical therapy, or scheduled procedures, an FSA can reduce your taxable income while helping you budget for those costs.

But the tradeoff is flexibility. An FSA is owned by your employer, not by you. If you leave your job, you may lose access to unused funds unless continuation rules apply. Also, FSAs usually don’t roll over fully. Some employers allow a limited carryover or grace period, but the account is still mostly designed for annual spending, not long-term saving.

HSA vs. FSA: The 2026 Comparison Chart

This is the core FSA vs HSA distinction: HSA money can become a lifelong asset, while FSA money is usually a yearly spending tool.

Interactive Tool: 2026 HSA vs. FSA Savings Estimator

To estimate your tax savings, use this simple formula:

Estimated tax savings = Contribution × estimated tax rate

Example: If you contribute $3,300 to an FSA and your combined federal, state, and payroll tax rate is 30%, your estimated tax savings may be about $990.

$3,300 × 30% = $990

For an HSA, the same logic applies, but the account can also grow over time if you invest unused funds. That is where the long-term difference appears. An FSA saves tax on near-term spending. An HSA can save tax today and potentially build tax-free healthcare wealth for future years.

2026 HSA vs. FSA Savings Estimator

Use this estimator to compare HSA and FSA tax savings. Enter your contribution amounts, estimated combined tax rate, and optional HSA investment assumptions to see both near-term tax savings and long-term HSA growth potential.

Tax Savings Inputs

Optional HSA Growth Inputs

Estimated Tax Savings = Contribution × Estimated Tax Rate

Projected HSA Investment Value = Invested HSA Amount × (1 + Expected Annual Return)Years

Projected HSA Growth = Projected HSA Investment Value − Invested HSA Amount

Note: This calculator is for educational planning only. HSA and FSA eligibility, annual limits, payroll rules, investment availability, qualified medical expense rules, and use-it-or-lose-it provisions may vary. Confirm details with your employer, benefits provider, or tax professional.

2026 Contribution Limits: What You Need to Know

The 2026 FSA contribution limits are important because FSAs require planning before the year begins. The expected healthcare FSA limit for 2026 is up to $3,300. That makes the FSA 2026 limits useful for people with predictable medical costs, but risky for people who may not spend the full amount.

The HSA limits are higher and depend on whether you have self-only or family HDHP coverage. HSA limits also include catch-up contributions for eligible older savers.

The key planning point isn’t just the maximum. It’s the amount you can confidently use. With an FSA, overfunding can mean forfeiting money. With an HSA, unused money remains yours, so contributing more can make sense if you can afford it and qualify.

Eligibility Rules: Can You Have Both?

The HSA and FSA rules can be tricky. In general, you can’t contribute to an HSA while covered by a regular healthcare FSA because the FSA may pay for general medical expenses before you meet the HDHP deductible.

There is one important exception: a limited-purpose FSA. This type of FSA is usually restricted to dental and vision expenses. Because it doesn’t cover broad medical costs, it can often be paired with an HSA.

You may also see dependent care FSAs, but those are different. They’re used for childcare or dependent care expenses, not medical expenses, and they don’t usually interfere with HSA eligibility. Before electing both accounts, read your benefits guide carefully. One wrong election can make you ineligible for HSA contributions.

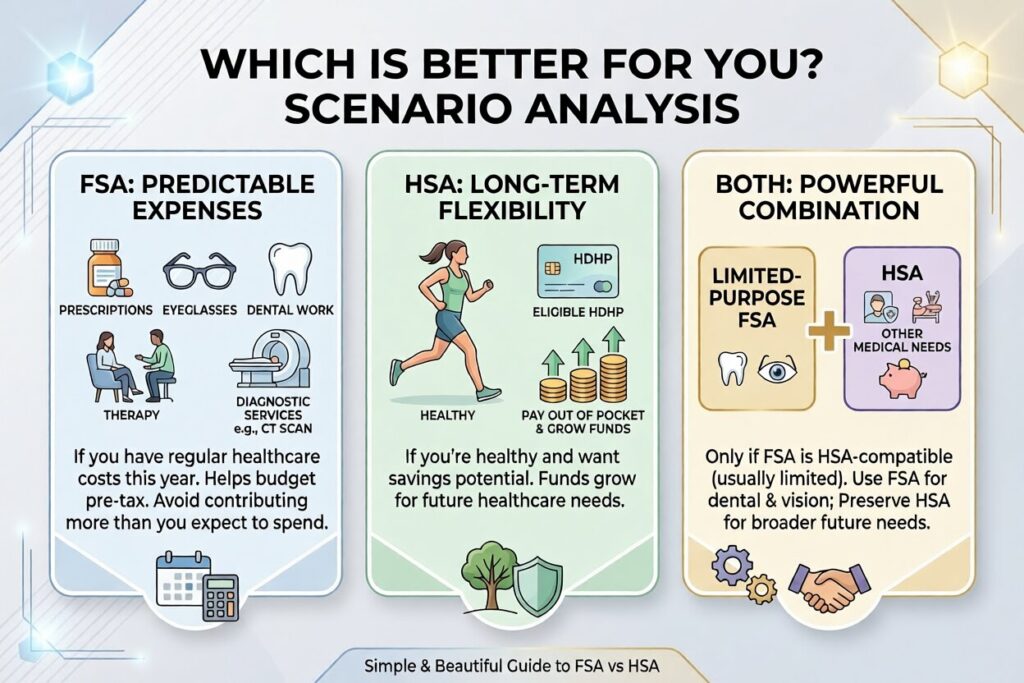

Which Is Better for You? Scenario Analysis

Choose an FSA if you have predictable healthcare expenses this year. For example, an FSA may work well if you know you’ll pay for regular prescriptions, eyeglasses, dental work, therapy, or diagnostic services like a CT scan. The FSA helps you budget with pre-tax dollars, but you should avoid contributing more than you expect to spend.

Choose an HSA if you’re healthy, enrolled in an eligible HDHP, and want long-term flexibility. It’s especially useful if you can pay some current medical costs out of pocket while allowing HSA funds to grow. Choose both only if your FSA is HSA-compatible, usually limited-purpose. That combination can be powerful: use the limited FSA for dental and vision, and preserve the HSA for broader future healthcare needs.

Conclusion

The HSA vs FSA choice isn’t about which account sounds better. It’s about timing, ownership, and risk. FSA money is excellent for expenses you can see coming. HSA money is better for costs you may face years from now.

Before Open Enrollment, review your insurance plan, expected medical bills, employer contributions, and investment options. The right decision can lower your taxes and make healthcare feel less unpredictable. The wrong one can leave money trapped, forfeited, or underused. Use the FSA for planned spending. Use the HSA for flexibility and future power. When you understand the difference, every healthcare dollar can work harder.

Related Articles

HRA vs. HSA: 2026 Key Differences & Comparison Guide (+ Chart)