vs 401(k): 2026 Key Differences and Which Plan Is Better?")

Retirement plan names can feel like alphabet soup. You see 401(a), 401(k), 403(b), and 457(b), and they all sound similar enough to blur together. But if you work for a government agency, public school, university, nonprofit, or private company, the difference between a 401(a) vs 401(k) can affect how much control you have, how much you can save, and what happens when you leave your job.

A 401(a) plan is usually offered by government, education, and nonprofit employers, and the employer controls the plan design. A 401(k) is more common in the private sector and usually lets employees choose how much to contribute. For 2026, the overall defined contribution limit is $72,000, while the 401(k) employee deferral limit is $24,500.

401(a) vs 401(k): The Simple Difference

The biggest difference is control. A 401(a) plan is employer-directed. Your employer may decide whether participation is mandatory, how much you must contribute, and how employer contributions vest. A 401(k) is usually employee-directed. You choose whether to participate, how much salary to defer, and whether to use traditional pre-tax or Roth contributions if available. So the real question isn’t only “which plan is better?” It is “which plan does your employer offer, and how much control do you have?”

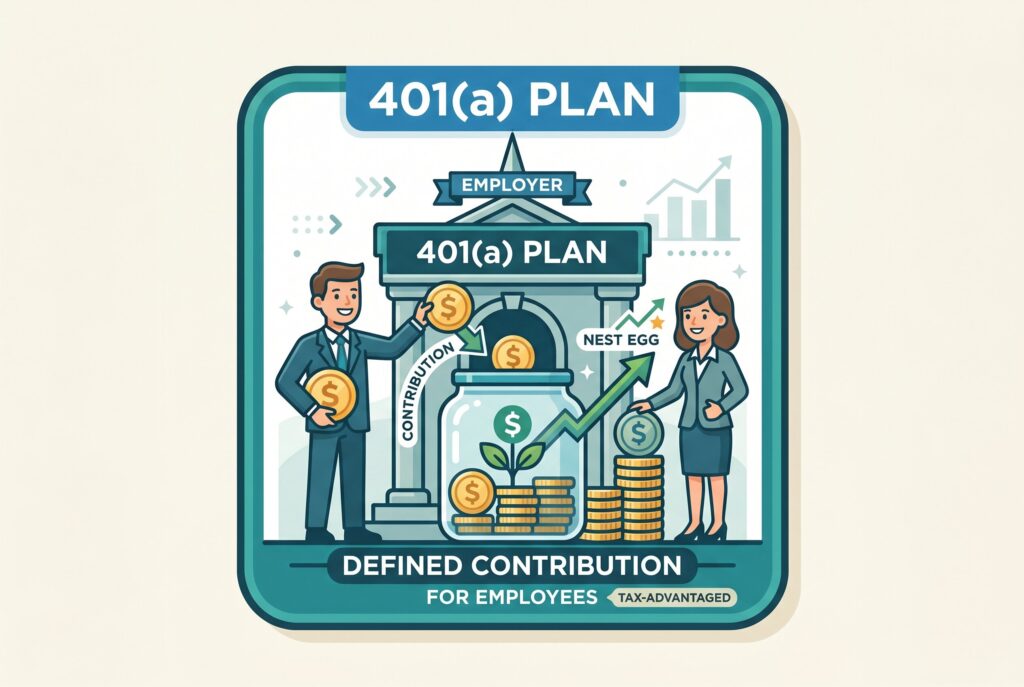

Who Usually Gets a 401(a) Plan?

A 401(a) plan is most common in the public sector. You may see one if you work for a city, county, state agency, public university, school district, hospital system, or nonprofit. These plans often hold employer contributions. In some benefits packages, the 401(a) is paired with a 403(b) or 457(b), giving employees multiple retirement savings layers. That is why a teacher, university employee, or government worker may have a 401(a) plus another voluntary plan.

Who Usually Gets a 401(k)?

A 401(k) is the standard workplace retirement plan for private-sector companies. You are more likely to see one if you work for a corporation, startup, small business, or large private employer. Most 401(k) plans are voluntary. You decide whether to contribute from your paycheck, and many employers encourage participation by offering a match. If your employer offers a match, contributing enough to receive the full match is usually one of the smartest first steps.

Mandatory Contributions vs Voluntary Contributions

A major difference between 401(a) vs 401(k) plans is whether you get a choice. Some 401(a) plans require mandatory employee contributions. For example, your employer might require you to contribute 6% or 8% of pay. You may not be able to lower that percentage. With a 401(k), contributions are usually voluntary. You can often start, stop, increase, or reduce contributions within plan rules. That flexibility makes 401(k)s easier to adjust when your budget changes.

2026 Contribution Limits

For 2026, the IRS increased the 401(k), 403(b), governmental 457, and Thrift Savings Plan employee deferral limit to $24,500. The broader defined contribution annual additions limit is $72,000 for 2026. This matters for 401(a) plans because the plan may include employer contributions, employee contributions, or both. The key distinction is that a 401(k) has a specific employee deferral limit, while a 401(a) is often governed by the overall annual additions limit and the employer’s plan design.

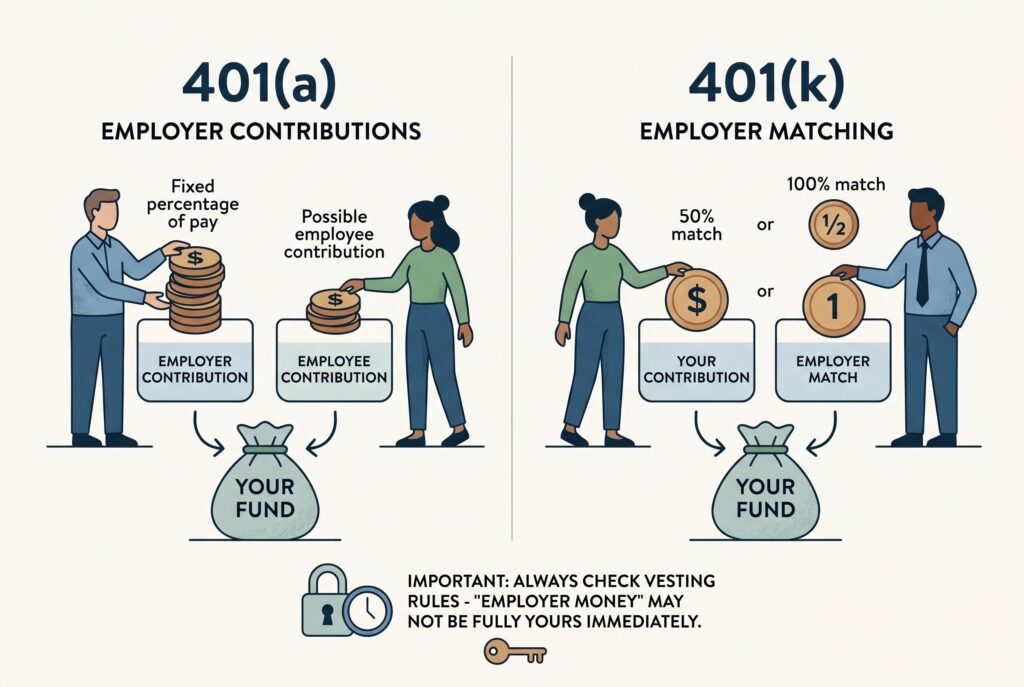

Employer Contributions and Matching

401(a) plans often emphasize employer contributions. Some employers contribute a fixed percentage of pay, while others require an employee contribution to receive employer money. 401(k) plans often use matching contributions. For example, an employer may match 50% or 100% of what you contribute up to a certain percentage of pay. In both cases, employer contributions are valuable. But always check vesting rules because “employer money” may not become fully yours immediately.

Vesting Rules: What You Actually Keep

Vesting determines how much of your employer’s contribution you keep if you leave your job. Your own contributions are generally yours, but employer contributions may vest over several years. For example, if your plan vests 20% per year over five years and you leave after two years, you may keep only 40% of employer contributions. This matters in both 401(a) and 401(k) plans, especially when comparing job offers.

Investment Options and Control

401(k) plans often provide a menu of mutual funds, target-date funds, index funds, and sometimes brokerage windows. Employees usually choose how to invest. 401(a) plans may offer less flexibility because the employer has more control. Some plans have limited menus or default investment structures. That doesn’t make them bad, but it does mean you should review fees, fund choices, and risk level carefully.

Withdrawal Rules and Early Penalties

401(a) withdrawal rules and 401(k) withdrawal rules are similar in many ways. Withdrawals before age 59½ may be subject to income tax and a 10% early withdrawal penalty unless an exception applies. Your plan document controls when withdrawals are allowed. Some plans limit in-service withdrawals, loans, or hardship access. Never assume you can access the money whenever you want simply because it is in your name.

Rollover Rules When You Leave a Job

When you leave an employer, you may be able to roll a vested 401(a) or 401(k) balance into an IRA or another eligible employer plan. A direct rollover usually helps avoid current taxes and penalties. A rollover to IRA can give you more investment control, but it may also change creditor protections, loan availability, and future backdoor Roth planning. Compare options before moving the money.

| Feature | 401(a) | 401(k) |

| Who Typically Offers It | Government agencies, schools, universities, nonprofits | Private-sector employers |

| Who Controls the Plan | Employer controls most plan rules | Employee controls participation and contribution amount |

| Employee Contributions | May be mandatory | Usually voluntary |

| Employer Contributions | Common and often fixed | Usually matching contributions |

| Contribution Flexibility | Limited employee flexibility | High employee flexibility |

| Investment Choices | May have fewer options | Usually broader investment menu |

| Best For | Public-sector and education workers | Private-sector employees |

| 2026 Employee Deferral Limit | Depends on plan design and annual additions limit | $24,500 |

| Overall Annual Additions Limit (2026) | $72,000 | $72,000 |

| Vesting Rules | Employer decides vesting schedule | Employer decides vesting schedule |

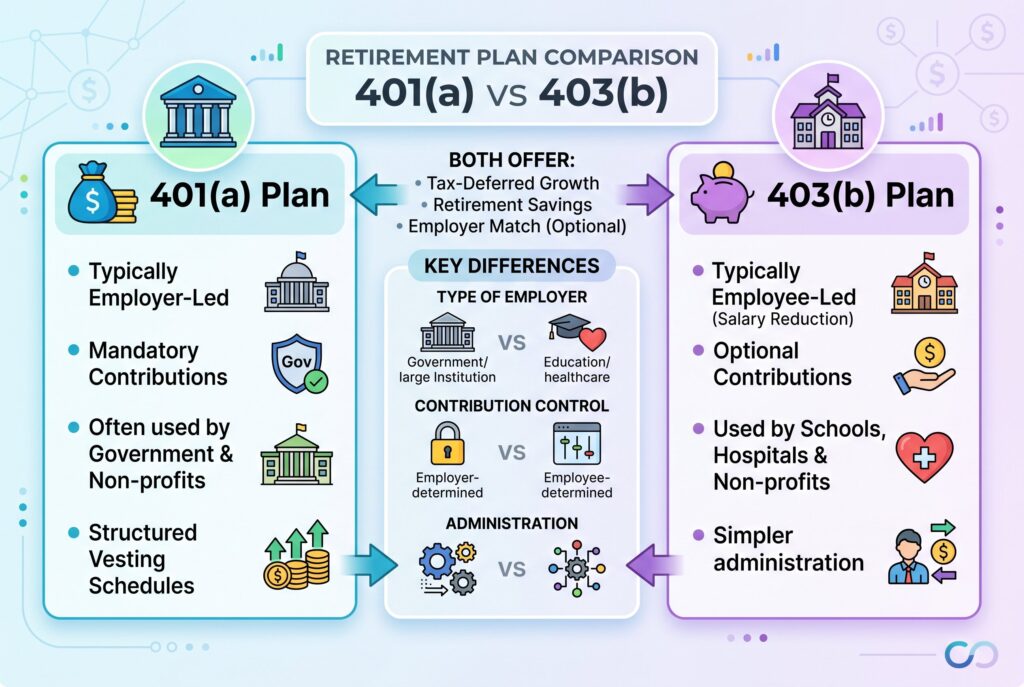

401(a) vs 403(b): Where It Fits

For public schools, universities, hospitals, and nonprofits, the comparison is often not just 401(a) vs 401(k). It may be 401(a) vs 403(b). A 403(b) is commonly used as a voluntary supplemental retirement plan for education and nonprofit workers. A 401(a) may hold employer contributions, while the 403(b) lets employees save extra from their paycheck. Together, they can create a stronger retirement strategy.

Which Plan Is Better?

A 401(k) may be better if you want flexibility, control over your contribution rate, and access to Roth or traditional salary deferrals. A 401(a) may be better if your employer contributes generously or requires participation that builds savings automatically. For public-sector workers, a 401(a) can be a powerful foundation, especially when paired with a 403(b) or 457(b). The best plan is the one that gives you the most employer money, reasonable fees, good investment options, and a contribution structure you can sustain.

Conclusion

Most workers don’t choose freely between a 401(a) and 401(k). Your employer decides what is available. Your job is to understand the rules and use the plan wisely. If your 401(a) includes employer contributions, don’t ignore it. If your 401(k) includes a match, try to capture the full match. If you have access to a 403(b) or 457(b) on top of a 401(a), consider whether you can save more after covering your essential budget. A retirement plan isn’t just a benefit line on a job offer. Used well, it becomes one of the strongest tools for building long-term financial security.