A backdoor Roth is a legal retirement planning strategy for high earners whose income blocks them from making a direct Roth IRA contribution. A backdoor Roth IRA isn’t a special account type. It’s a two-step process: contribute nondeductible money to a Traditional IRA, then convert that money to a Roth IRA. For 2026, this strategy matters because Roth IRA income limits still prevent many high-income investors from contributing directly.

2026 Income Limits & Why You Need a Backdoor

For 2026, direct Roth IRA contributions phase out between $153,000 and $168,000 for single filers and heads of household. For married couples filing jointly, the phase-out range is $242,000 to $252,000. Married filing separately remains $0 to $10,000. That means if your MAGI is above the upper limit, you can’t make a normal direct Roth IRA contribution. But there are no income limits on Roth conversions. That gap is what makes the backdoor Roth contribution strategy possible. For 2026, the IRA contribution limit is $7,500, plus a $1,100 catch-up contribution if you’re age 50 or older.

Step-by-Step: How to Set Up a Backdoor Roth in 2026

Step 1: Open and fund a Traditional IRA.

Start by opening a Traditional IRA if you do not already have one. Then contribute after-tax, nondeductible money to the account. This means you are not claiming a tax deduction for the contribution on your tax return. The goal is to create after-tax basis in the Traditional IRA, which can later be converted to a Roth IRA.

Step 2: Consider the timing.

Before converting, think carefully about when to move the money into the Roth IRA. Some advisors suggest waiting for a short period because of possible step transaction concerns, while others prefer converting quickly so the account has less time to generate taxable earnings. If the Traditional IRA earns interest, dividends, or investment gains before the conversion, that growth may be taxable. The right timing depends on your tax advisor’s view, your risk tolerance, and whether there is any account activity between the contribution and conversion.

Step 3: Convert to a Roth IRA.

After funding the Traditional IRA, request a Roth conversion through your IRA provider. This moves the Traditional IRA balance into a Roth IRA. If the account only contains nondeductible contributions and has no earnings, the conversion may create little or no taxable income. However, if the account earned money before the conversion, that growth is generally taxable. You should also consider the pro-rata rule if you have other pre-tax IRA balances, because that can make part of the conversion taxable.

Step 4: File IRS Form 8606.

When you file your tax return, complete IRS Form 8606 to report the nondeductible IRA contribution and track your after-tax basis. This step is important because it tells the IRS that part of your IRA money has already been taxed. Skipping Form 8606 can create confusion later and may cause double-taxation when you convert or withdraw funds. Keep a copy of the form with your tax records each year you make nondeductible IRA contributions.

Interactive Tool: The Backdoor Roth Pro-Rata Calculator

The most important calculator asks:

- Total pre-tax IRA money

- Total after-tax IRA basis

- Amount converted

- Expected taxable percentage

Example:

- Pre-tax IRA assets: $93,000

- After-tax contribution: $7,000

- Total IRA balance: $100,000

- After-tax percentage: 7%

If you convert $7,000, only 7% may be tax-free. The rest may be taxable because of the pro-rata rule.

Backdoor Roth Pro-Rata Calculator

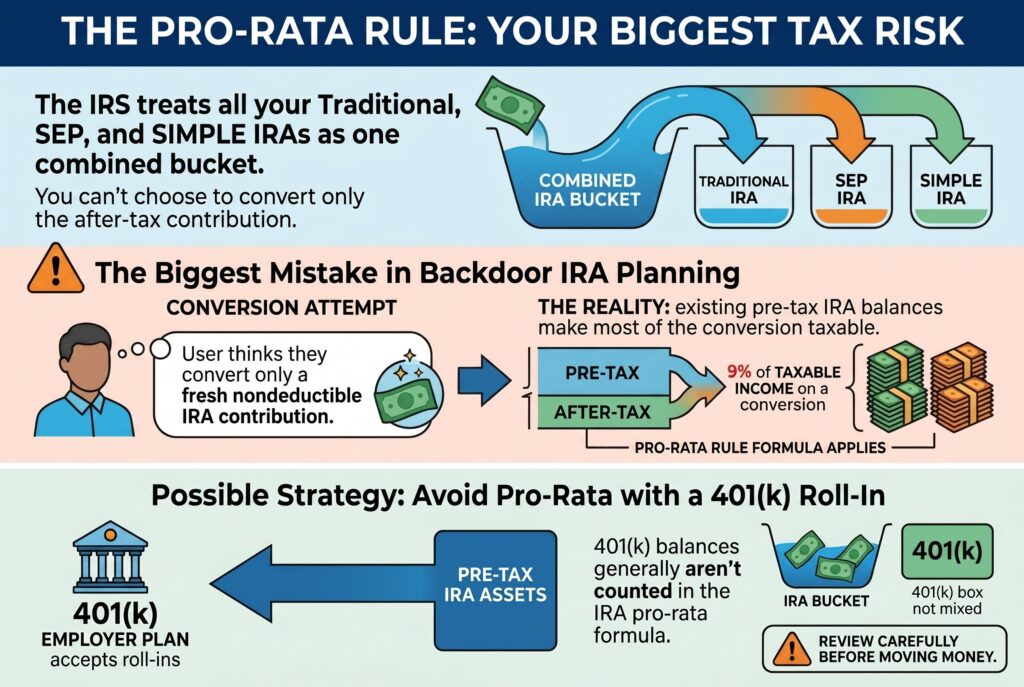

The Pro-Rata Rule: Your Biggest Tax Risk

The pro-rata rule says the IRS treats all your Traditional, SEP, and SIMPLE IRAs as one combined bucket. You can’t choose to convert only the after-tax contribution. This is the biggest mistake in backdoor IRA planning. Someone may think they’re converting only a fresh nondeductible IRA contribution, but existing pre-tax IRA balances can make most of the conversion taxable. One possible strategy is rolling pre-tax IRA assets into an employer 401(k), if the plan accepts roll-ins. 401(k) balances generally aren’t counted in the IRA pro-rata formula. This should be reviewed carefully before moving money.

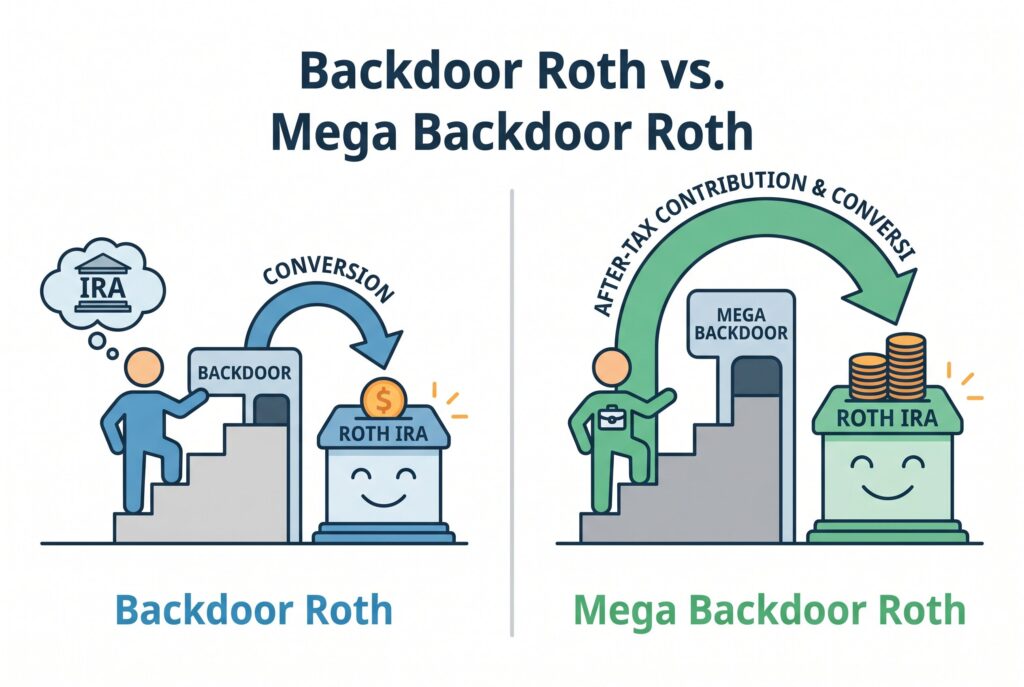

Backdoor Roth vs. Mega Backdoor Roth

What is a mega backdoor Roth? It’s a separate strategy that uses an employer-sponsored retirement plan, usually a 401(k), to move after-tax contributions into a Roth account. Backdoor Roth: Uses IRAs. The annual IRA limit is $7,500, or $8,600 if age 50 or older in 2026.

Mega backdoor Roth: Uses a 401(k) plan that allows after-tax contributions and in-plan Roth conversions or in-service withdrawals. The total defined contribution plan limit for 2026 is $72,000, before applicable catch-up rules. The mega backdoor Roth limit 2026 depends on your plan design, employer contributions, employee deferrals, age, and whether after-tax contributions are allowed.

Checklist: Before You Start Your 2026 Conversion

- Do you have other Traditional, SEP, or SIMPLE IRA assets?

- Have you checked whether your 401(k) accepts IRA roll-ins?

- Have you maxed out your 401(k) or HSA first?

- Do you have cash available to pay tax on any earnings or pre-tax conversion amount?

- Will you file Form 8606 correctly?

- Do you understand that Roth conversions generally can’t be undone?

- If the answer to any of these is unclear, get tax guidance before converting.

Conclusion

A backdoor Roth can be powerful for high earners who want tax-free Roth growth but can’t contribute directly. Still, it isn’t a casual click-and-done move. The pro-rata rule, Form 8606, taxable earnings, and conversion timing all matter. Used correctly, the backdoor Roth IRA can help you keep building tax-diversified retirement savings in 2026. Used carelessly, it can create surprise taxes. Precision is the difference.

Related Articles

Backdoor vs. Mega Backdoor Roth: 2026 Key Differences Explained