For high-income earners, the backdoor Roth and mega backdoor Roth both solve the same frustrating problem: you may want tax-free Roth growth, but IRS income limits can block you from making direct Roth IRA contributions. The difference is scale. A regular backdoor strategy helps you move IRA-sized dollars into a Roth account, while the mega version may let you move tens of thousands more through an employer retirement plan. In 2026, knowing the difference can turn unused savings capacity into a serious long-term tax advantage.

Side-by-Side: Backdoor vs. Mega Backdoor Roth in 2026

| Feature | Regular Backdoor Roth | Mega Backdoor Roth |

| Where it happens | Individual Retirement Accounts, or IRAs | Workplace plans, usually 401(k) or Solo 401(k) |

| 2026 contribution limit | $7,500, or $8,600 if age 50+ | Depends on plan limits and employer contributions |

| Employer permission needed? | No | Yes |

| Primary tax form | IRS Form 8606 | IRS Form 1099-R |

| Pro-rata rule risk | High if you have pre-tax IRAs | Lower because 401(k) plans use separate accounting |

| Best for | Smaller annual Roth funding | High earners with large cash flow |

For 2026, the 401(k) employee deferral limit is $24,500, the IRA limit is $7,500, and the IRA catch-up contribution for age 50+ is $1,100.

What Is a Backdoor Roth IRA?

What is a backdoor Roth IRA? It’s a legal Roth conversion strategy for people who earn too much to contribute directly to a Roth IRA. Here is how it works. First, you contribute post-tax dollars to a Traditional IRA. Since your income is high, you usually treat this as a nondeductible contribution. Then you convert that money into a Roth IRA.

The danger is the pro-rata trap. If you already have pre-tax money in a Traditional IRA, SEP IRA, or SIMPLE IRA, the IRS doesn’t let you isolate only the after-tax dollars. It treats your IRA money as one combined bucket. That means part of your conversion may become taxable. This is why a backdoor IRA can be simple for someone with no pre-tax IRA balance, but messy for someone with old rollover IRA assets.

What Is a Mega Backdoor Roth?

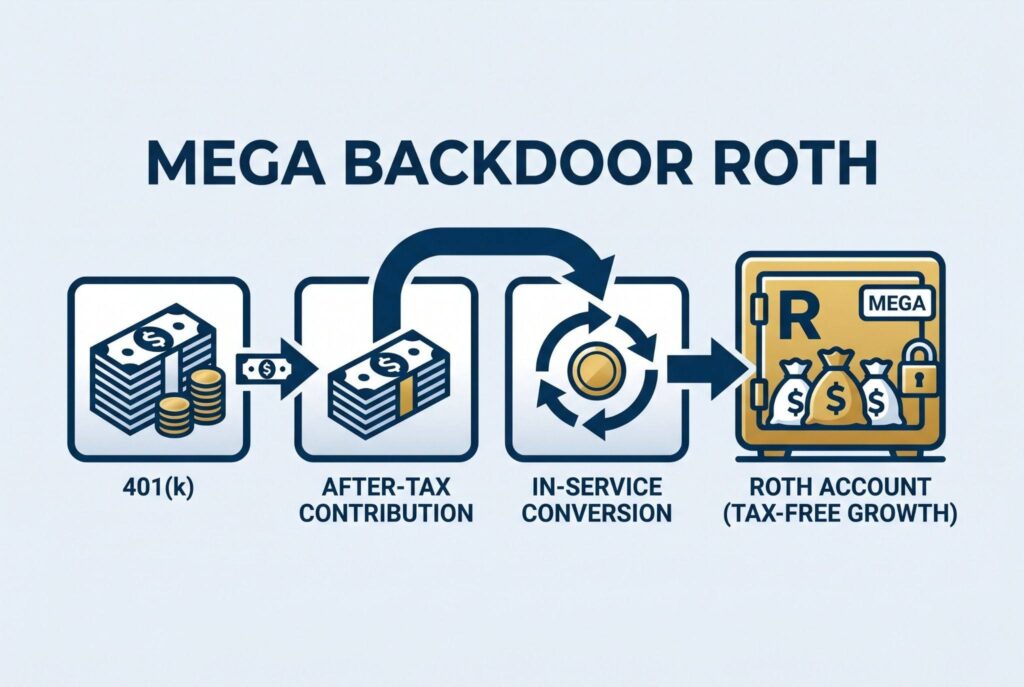

What is a mega backdoor Roth? It’s a bigger Roth strategy that operates through a workplace retirement plan. The process has three layers. First, you max out your regular 401(k) deferral. Second, you contribute additional after-tax non-Roth dollars to your 401(k), if the plan allows it. Third, you convert those after-tax dollars into a Roth 401(k) or roll them into a Roth IRA. The plan requirements are strict. Your employer’s 401(k) must allow after-tax non-Roth contributions. It must also allow either in-plan Roth conversions or in-service withdrawals. Without those features, the mega strategy usually isn’t available.

Interactive Tool: 2026 Mega Backdoor Space Calculator

To estimate your mega backdoor Roth limit 2026, use this formula:

Possible after-tax contribution space = Total plan limit − employee deferral − employer contribution

For example, assume you’re under 50:

- Total plan limit: $72,000

- Your 401(k) deferral: $24,500

- Employer match: $12,000

$72,000 − $24,500 − $12,000 = $35,500

That $35,500 may be your potential after-tax contribution room if your plan allows it. The official 2026 annual additions limit for defined contribution plans is $72,000 for those under age 50. This math is why the mega backdoor feels so powerful. It doesn’t replace normal retirement savings; it sits on top of it.

2026 Mega Backdoor Space Calculator

Use this calculator to estimate potential mega backdoor Roth after-tax contribution space for 2026. Enter the total defined contribution plan limit, your employee deferral, and employer contribution. The calculator shows the possible after-tax contribution room if your plan allows after-tax contributions and in-plan Roth conversion or rollover.

Potential After-Tax Contribution Space = Total Plan Limit − Employee Deferral − Employer Contribution − Other Plan Additions

Total Contributions Already Used = Employee Deferral + Employer Contribution + Other Plan Additions

Plan Limit Remaining = Potential After-Tax Contribution Space ÷ Total Plan Limit × 100

Note: This calculator is for planning only. The 2026 annual additions limit shown here is based on the example provided. Actual eligibility depends on your plan document, after-tax contribution rules, in-plan Roth conversion or rollover availability, employer contributions, nondiscrimination testing, compensation limits, and payroll timing.

The Solo 401(k) Advantage for the Self-Employed

Self-employed individuals may have a special opportunity. If you own a business with no eligible full-time employees other than yourself or possibly your spouse, you may be able to design a Solo 401(k) with after-tax contribution and Roth conversion features. That means you aren’t waiting for a corporate HR department to offer the right plan. You may be able to choose a provider and plan document that supports the strategy from the start. But the Solo 401(k) version isn’t automatic. Your income, business structure, plan document, contribution timing, and tax filing deadlines all matter. If you have employees, controlled group rules and plan testing can become more complex.

Which Strategy Should You Choose?

Choose the regular backdoor Roth if your employer plan doesn’t allow after-tax contributions, you don’t have large pre-tax IRA balances, or you simply want to fund the annual IRA limit.

Choose the mega backdoor Roth if your workplace plan allows it, you already max out your standard 401(k), and you still have significant cash flow available for retirement savings. Can you do both? Yes, in many cases. Contributing to a workplace 401(k) doesn’t automatically prevent you from using a backdoor Roth IRA in the same year. The real questions are whether you have enough cash flow, whether the pro-rata rule applies, and whether your employer plan supports the mega strategy.

Conclusion

Both strategies can be extremely effective, but neither should be treated casually. For a regular backdoor Roth contribution, IRS Form 8606 is critical because it tracks nondeductible IRA basis. If you skip it, you may create confusion or even double taxation later. For a mega backdoor Roth, Form 1099-R reporting and plan records matter. The IRS has guidance on rollovers of after-tax retirement plan contributions, including situations where accounts contain both pre-tax and after-tax amounts. IRS Notice 2014-54 also clarified important rollover treatment for after-tax amounts in retirement plans.

The main takeaway is simple: the backdoor Roth is smaller but more accessible; the mega backdoor Roth is larger but depends on plan design. Used carefully, both can help high earners build tax-free retirement wealth. Used carelessly, either one can create tax headaches. Before moving money, ask your CPA or financial advisor to review your IRA balances, 401(k) plan features, contribution limits, and reporting requirements.