")

What is probate? Probate is the legal process used to settle a person’s estate after death. A probate court reviews the will, confirms who has authority to act, makes sure debts and taxes are paid, and oversees the transfer of remaining assets to heirs or beneficiaries. It can happen whether the person died with a will or without one. When there is a valid will, the estate is testate. When there isn’t a will, the estate is intestate, and state law decides who inherits. A probate estate can be simple or stressful depending on the assets, debts, family dynamics, and state rules. Understanding “how does probate work” can help families avoid confusion during an already emotional time.

The Fiduciary Vocabulary Guide

Testate vs. Intestate

Testate means the person died with a valid will. The will usually names beneficiaries and appoints an executor. Intestate means the person died without a valid will. In that case, state law decides who receives property. Intestacy can create delays because the court must identify legal heirs instead of simply following written instructions.

Executor vs. Administrator

An executor is the person named in the will to manage the estate. An administrator is appointed by the probate court when there isn’t a will or when the named executor can’t serve. Both roles carry fiduciary responsibility, which means they must act in the best interests of the estate and beneficiaries, not themselves.

Letters Testamentary

Letters Testamentary are court documents that prove the executor has legal authority to act for the estate. Banks, brokerages, insurance companies, and title offices often won’t release information or transfer assets without them. This document is what turns a grieving family member into the official estate representative.

When Is Probate Required? The Asset Rule

Probate Assets

When is probate required? Usually, probate is required when assets are owned only in the deceased person’s name and don’t have a beneficiary designation. Common probate assets include a house titled solely to the person who died, a personal bank account with no payable-on-death beneficiary, vehicles, personal property, and investment accounts without transfer instructions.

Non-Probate Assets

Non-probate assets can transfer outside probate. These may include life insurance with a named beneficiary, retirement accounts with beneficiaries, jointly owned property with rights of survivorship, and accounts with payable-on-death or transfer-on-death designations. These assets usually pass directly to the named person, which can save time and provide faster access to cash.

How Does Probate Work? The 5-Step Process

Step 1: Filing the Petition and Authenticating the Will

The process usually begins when someone files a petition with the probate court. If there is a will, the court reviews it to confirm it appears valid. This step officially opens the estate case and notifies interested parties. If the will is missing, unclear, or challenged, the process can become slower and more expensive.

Step 2: Appointing the Fiduciary

Next, the court appoints the executor or administrator. Once approved, that person receives authority to manage the estate. This role includes communicating with heirs, protecting assets, dealing with creditors, keeping records, and following court deadlines. It isn’t just an honorary title; it’s a serious legal job.

Step 3: Inventorying the Estate’s Assets

The fiduciary must identify, list, and value the estate’s assets. This may include real estate, bank accounts, brokerage accounts, vehicles, business interests, jewelry, furniture, and digital assets. Accurate inventory matters because heirs, creditors, tax agencies, and the court all rely on the numbers.

Step 4: Paying Outstanding Debts and Taxes

Before heirs receive property, the estate must pay valid debts and taxes. This may include credit card balances, medical bills, funeral costs, final income taxes, property taxes, and estate administration expenses. The executor shouldn’t distribute assets too early, because unpaid claims can create personal liability problems.

Step 5: Distributing the Remaining Assets

After debts, taxes, and court requirements are handled, the remaining assets can be distributed. If there is a will, distributions follow the will. If there isn’t a will, distributions follow state intestacy law. Once transfers are complete and records are filed, the probate estate can usually be closed.

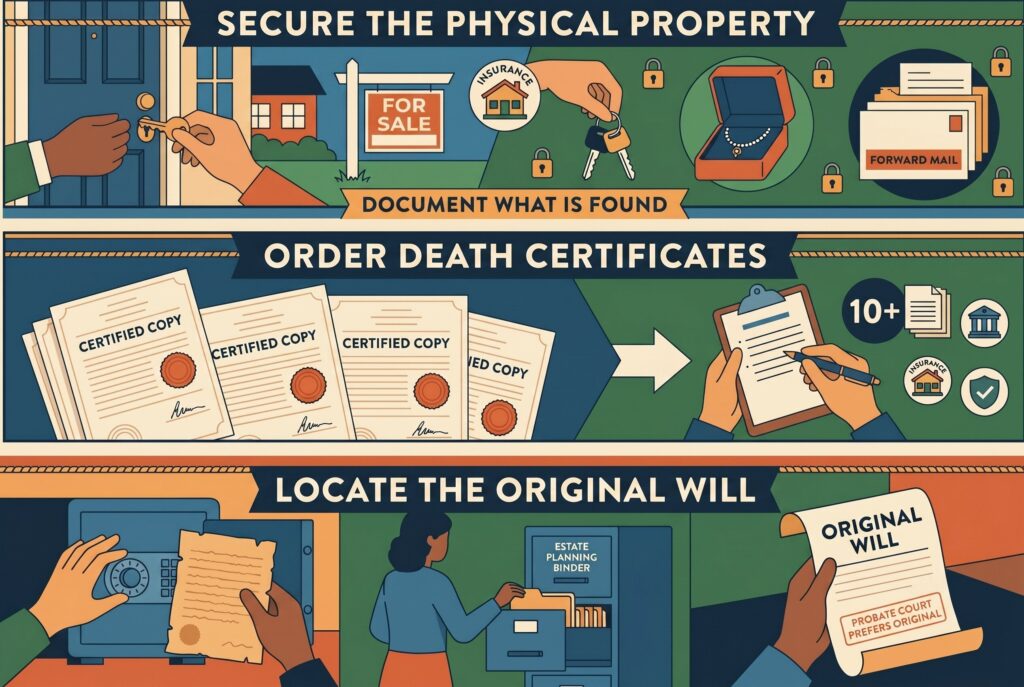

The Executor’s Action Plan: The First 30 Days

Secure the Physical Property

The first job is protection. Lock the home, secure vehicles, collect valuables, forward mail, and keep insurance active. Empty houses can attract theft, damage, or family disputes. The executor should document what is found and avoid giving away items casually before the estate inventory is complete.

Order Death Certificates

Families often need more death certificates than expected. Banks, insurers, retirement plans, government agencies, and title companies may each require certified copies. Ordering 10 or more copies early can prevent delays. It’s a small administrative step that can save weeks later.

Locate the Original Will

The original will matters. Look in safes, filing cabinets, safe deposit boxes, attorney offices, and estate planning binders. A copy may help, but courts often prefer the original document. If the original can’t be found, the court may require extra proof before accepting a copy.

How to Avoid Probate: The Wealth Preservation Strategy

Set Up a Revocable Living Trust

A revocable living trust is one of the most effective answers to how to avoid probate. Assets placed properly inside the trust can pass to beneficiaries without going through probate court. A trust can also preserve privacy, reduce delays, and help manage assets if the owner becomes incapacitated.

Use POD and TOD Designations

Payable-on-death and transfer-on-death designations let certain accounts pass directly to named beneficiaries. This can work for bank accounts, brokerage accounts, and sometimes vehicles or real estate, depending on state law. These designations are simple, but they must be updated after marriages, divorces, births, deaths, or major life changes.

Leverage Life Insurance Policies

Life insurance can provide fast liquidity because proceeds usually go directly to the named beneficiary. That money can help pay funeral costs, household bills, mortgage payments, or legal expenses while the estate is still being processed. The key is keeping beneficiary names current and avoiding naming the estate unless there is a specific reason.

The State-by-State Small Estate Affidavit

Many states offer a simplified process for smaller estates. A small estate affidavit may allow heirs to collect assets without full probate if the estate falls below a legal threshold. The limit varies by state, so families should check local rules. This option can save time, but it still requires accuracy and proper documentation.

Conclusion

Probate isn’t always bad, but it can be slow, public, and expensive. The more planning you do while alive, the easier things are for the people you love. If you want to reduce stress for your family, learn “when is probate required”, understand “how does probate work,” and use tools such as beneficiary designations, joint ownership where appropriate, life insurance, and revocable living trusts. A strong estate plan doesn’t only transfer money. It protects privacy, preserves family peace, and gives your heirs a clear path when they need it most.