")

When people search for how to set up a trust, the biggest mistake is thinking the job ends once the documents are signed. In reality, setting up a living trust in 2026 has two equally important phases: creation and funding. Creation is the legal blueprint. Funding is the process of moving assets into the trust so the document actually controls them. If you create the trust but forget to retitle your house, update bank accounts, or assign business interests, your family may still face probate. A living trust only works when the paperwork and the asset transfers are completed together.

Phase 1: Creation

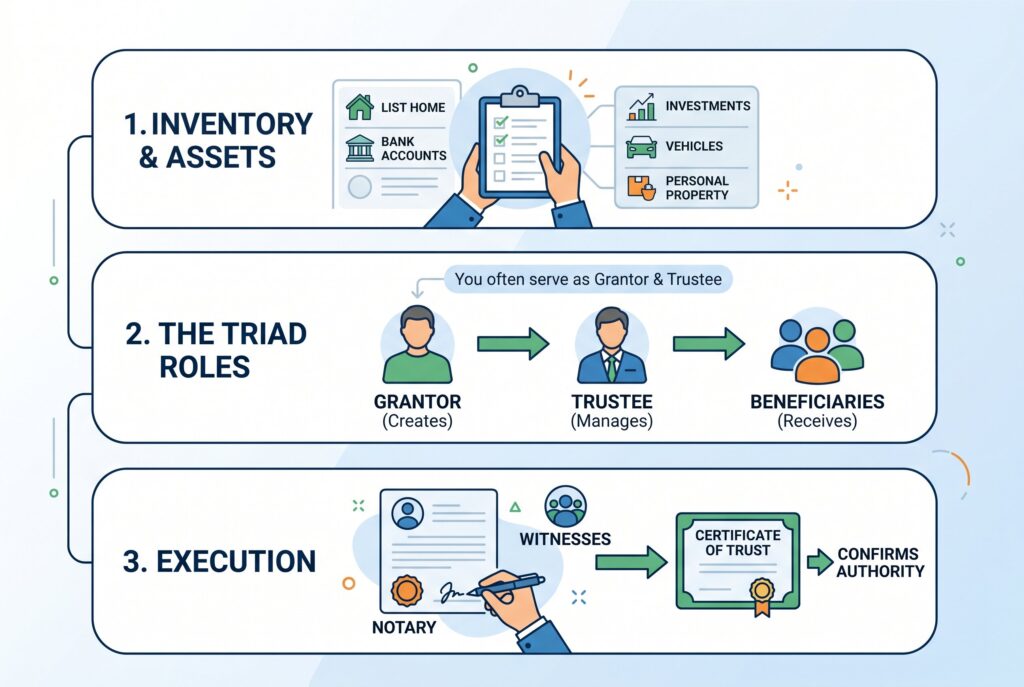

Step 1: Inventory & the Revocable Advantage

Before learning how to create a trust, begin with a full inventory. List your home, bank accounts, taxable investment accounts, business interests, vehicles, valuable personal property, and life insurance policies. This gives you a clear picture of what the trust must eventually control.

For most families, a revocable living trust is the most practical structure. You can change it, cancel it, update beneficiaries, sell assets, refinance property, and remain in control while you are alive. Among the biggest benefits of a trust is that it can help your family avoid probate after death while allowing a successor trustee to manage assets if you become incapacitated.

Step 2: Assigning the Core Triad

To understand how a trust works, think of three key roles: the grantor creates the trust, the trustee manages it, and the beneficiaries receive the assets or benefits. Each person has a specific role in making sure the trust operates as intended.

In a revocable living trust, you can usually serve as both grantor and trustee during your lifetime, allowing you to maintain full control of your assets. When learning how to set up a living trust, one of the most important decisions is choosing a successor trustee. This person or institution takes over if you pass away or become unable to manage your affairs due to illness, injury, or incapacity. A good successor trustee should be trustworthy, organized, financially responsible, and capable of communicating effectively with beneficiaries during potentially stressful situations.

Step 3: Execution and the Certificate of Trust

Once the document is drafted, it must be signed correctly under your state’s rules. That may involve notarization, witnesses, or both. Don’t rush this step, because improper execution can create disputes later.

After signing, ask for a Certificate of Trust. This shorter document proves the trust exists and confirms trustee authority without revealing private details about who inherits what. It’s especially useful when dealing with banks, brokerages, title companies, and financial institutions.

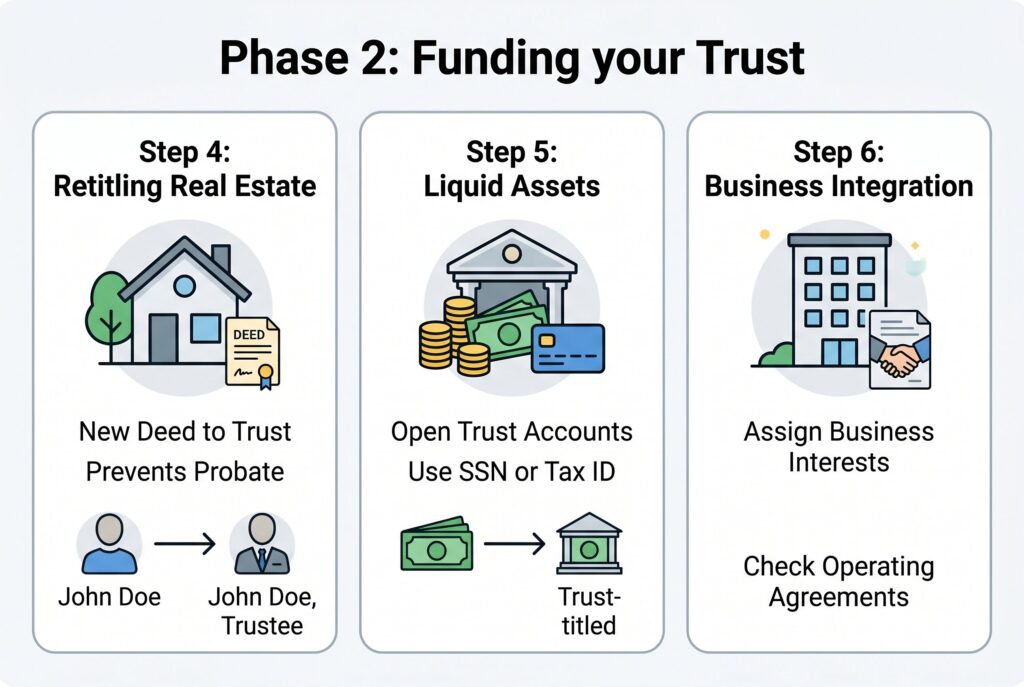

Phase 2: Funding

The answer to how to start a trust isn’t complete until funding is done. Funding means transferring ownership of assets from your personal name into the name of the trust.

Step 4: Retitling Real Estate

Your home is often the most important asset to fund. You can’t simply list the property in a schedule and assume it’s protected. In most cases, you must prepare and record a new deed, such as a warranty deed or quitclaim deed, transferring ownership from your individual name to the trust.

For example, the owner may change from John Doe to John Doe, Trustee of the John Doe Living Trust. The exact wording depends on your trust and state law. This deed must be recorded with the local land records office. If it isn’t recorded properly, the home may still require probate.

Step 5: Liquid Assets & How to Open a Trust Account

For cash and taxable investments, you may need to open trust account arrangements at your bank or brokerage. Bring your Certificate of Trust, government issued ID, and any required tax information.

A revocable living trust often uses your Social Security number while you are alive because you and the trust are usually treated as the same taxpayer. The bank may ask you to complete a change of ownership form or open a new trust titled checking, savings, or brokerage account.

This step matters because money left in a personal account may not be controlled by the trust unless beneficiary designations or transfer rules apply.

Step 6: Business Integration

If you own an LLC, partnership interest, or closely held business, you may need to assign that ownership interest to the trust. This often requires an Assignment of LLC Interest or similar transfer document.

Check your operating agreement first. Some businesses restrict transfers or require member consent. Skipping this step can create major problems because the business interest may become frozen or disputed after death. Business owners should treat trust funding as part of succession planning, not just estate paperwork.

The SECURE Act Warning

Retirement accounts require special caution. Don’t retitle an active IRA or 401(k) into the name of your living trust while you are alive. Doing so may trigger tax consequences, penalties, or a deemed distribution.

Instead, retirement accounts are usually handled through beneficiary designations. In some cases, you may name the trust as a beneficiary, but this must be drafted carefully. A poorly written trust beneficiary designation can create tax acceleration problems and force heirs to withdraw funds faster than expected. This is one area where professional advice is strongly recommended.

What Not to Put Directly Into a Living Trust

Not every asset belongs inside the trust during your lifetime. Retirement accounts usually stay outside. Health savings accounts often need individual ownership. Vehicles may or may not be worth retitling depending on state rules, insurance, and local transfer procedures.

Life insurance is commonly handled by beneficiary designation, though some families may use more advanced trust planning for tax or control reasons. Personal property can often be transferred through a general assignment document, but valuable collections should be listed clearly.

The goal isn’t to put everything blindly into the trust. The goal is to coordinate ownership, beneficiaries, and legal control.

Maintenance: Keep the Trust Alive

A living trust should be reviewed every three to five years and after major life events. Update it after marriage, divorce, birth, death, adoption, major asset purchases, business changes, or relocation to another state. Also review funding after each major purchase. If you buy a new house, open a new brokerage account, or create a new LLC, the trust may need updates.

Conclusion

A living trust is most effective when it is properly funded and kept up to date. Simply creating the document isn’t enough. Assets such as real estate, financial accounts, and business interests must be transferred into the trust for it to work as intended. When maintained correctly, a living trust can help avoid probate, protect privacy, provide continuity during incapacity, and make the transfer of assets easier for your loved ones. As your family and finances change over time, the trust should be reviewed and updated to reflect your current wishes and circumstances.

Related Articles

Types of Trusts Explained: How to Match the Right Trust to Your Wealth