")

The cost to set up a trust in 2026 depends on how complex your estate is and who prepares the documents. If you use DIY software, the price may be as low as $150 to $400. If you hire an estate planning attorney, the average attorney fee for living trust preparation usually falls between $1,500 and $4,000. Advanced trusts for high net worth families, asset protection, tax planning, or business succession can cost $5,000 to $15,000 or more. The real question isn’t only how much does it cost to set up a trust, but what is included in that price.

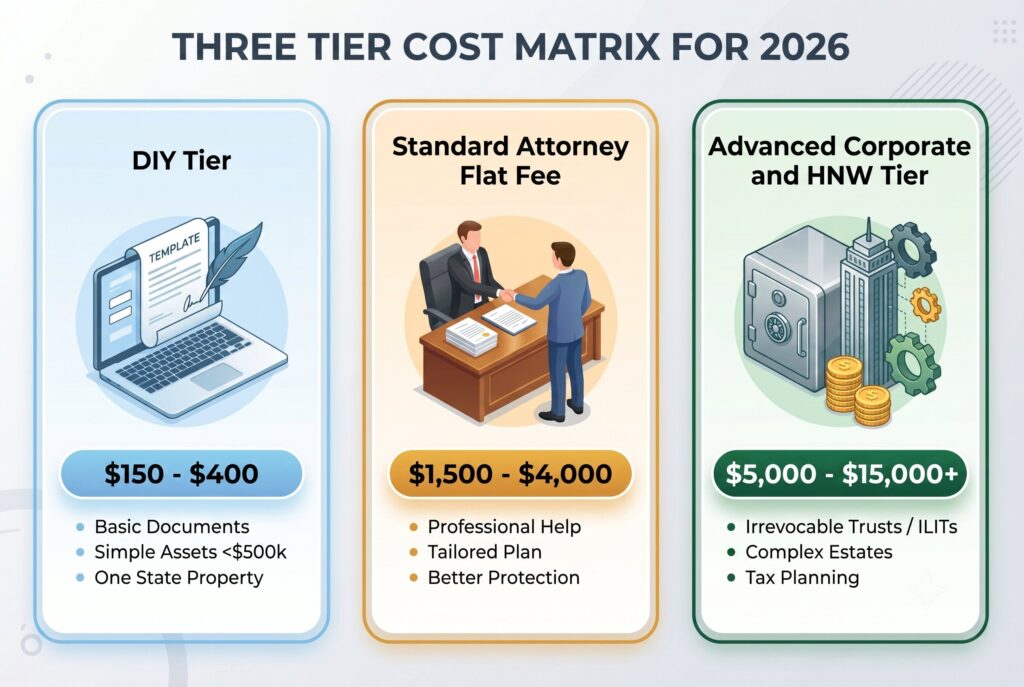

The Three Tier Cost Matrix for 2026

1. The DIY Tier ($150 to $400)

The lowest DIY trust cost comes from online platforms that generate basic documents from templates. This may work if your estate is simple, your assets are under about $500,000, your family structure is straightforward, and you own property in only one state. The risk is that software usually creates documents, not a complete estate plan. You may still need to fund the trust, retitle accounts, prepare deeds, and coordinate beneficiaries. If you make a mistake, your family may still face probate.

2. The Standard Attorney Flat Fee ($1,500 to $4,000)

This is the most common range for families who want to set up a trust with professional help. A standard attorney package may include a revocable living trust, pour over will, power of attorney, healthcare directive, trustee instructions, and notarized execution. This option costs more upfront, but it usually gives better protection because the attorney can tailor the trust to your state, assets, family structure, and future goals.

3. The Advanced Corporate and HNW Tier ($5,000 to $15,000+)

Advanced planning costs more because it may involve irrevocable trusts, ILITs, GRATs, asset protection trusts, business succession documents, or multiple real estate transfers. These structures require more tax analysis, drafting time, and coordination with financial advisors. For high value estates, this fee can still be reasonable if the planning protects millions of dollars from probate, litigation, or unnecessary tax exposure.

The Scope Trap: Flat Fee vs Hourly Scope Creep

A flat fee sounds simple, but you need to know exactly what it includes. Some attorneys draft the trust only. Others include funding assistance, deed preparation, bank instructions, and follow up support. The biggest hidden issue is funding. If the attorney hands you a binder but doesn’t help transfer your house, bank accounts, or brokerage assets into the trust, the plan may remain unfinished. Ask whether deed recording is included. If not, you may pay an extra $300 to $500 per property. Also ask whether the fee includes phone calls, revisions, trustee instructions, and document storage.

Hidden Maintenance Costs After Opening

A family trust cost doesn’t always end when the documents are signed. Some trusts require ongoing expenses. If you name a corporate trustee, expect annual management fees. Many banks and trust companies charge around 1% to 1.5% of trust assets each year. That can be expensive on large estates. If the trust is irrevocable, it may need its own EIN and annual tax filing. A CPA may charge around $500 to $1,200 per year to prepare Form 1041. Even revocable trusts can create future costs. If you divorce, remarry, have a child, buy property, or change beneficiaries, amendments or restatements may cost $300 to $800 or more.

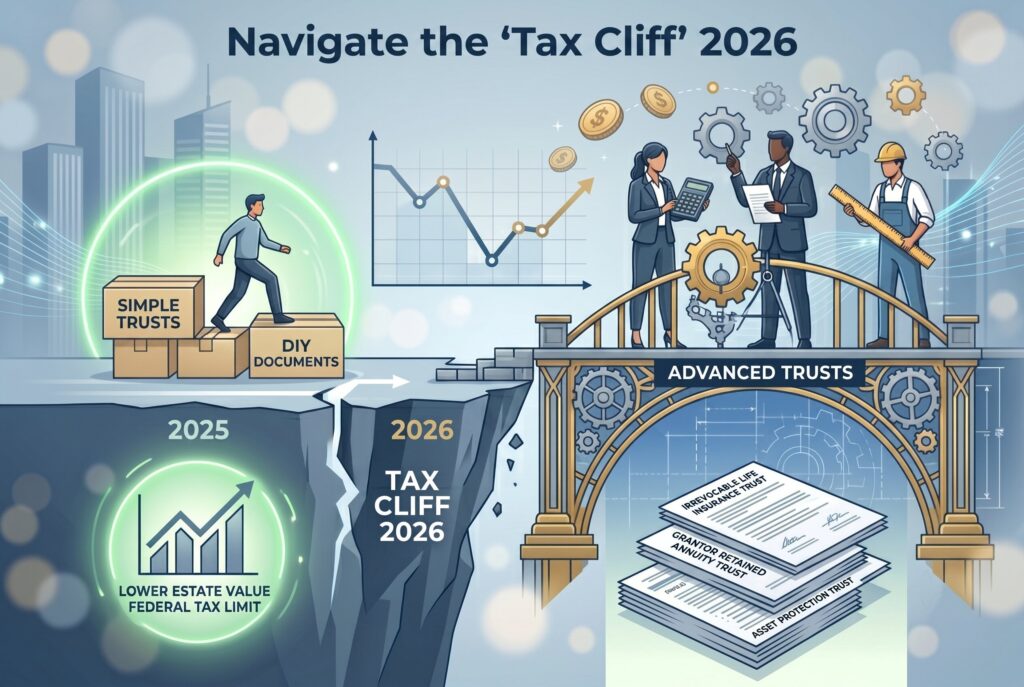

The 2026 Tax Cliff Premium

In 2026, advanced estate planning may become more expensive because many families are preparing for lower estate tax exemptions. If your estate is near the federal exemption range, simple DIY documents may not be enough. Lawyers charge more for advanced trust structures because they require strategy, not just paperwork. An irrevocable life insurance trust, grantor retained annuity trust, or asset protection trust must be drafted carefully to avoid tax problems and preserve legal benefits. This is why how to create a trust isn’t always a document question. For larger estates, it’s a financial engineering question.

Trust Account Basics: What Happens After Signing?

After the trust is created, you may need to open bank or brokerage accounts in the trust’s name. Trust account basics include account titling, trustee authority, tax identification, and funding. For a revocable trust, banks often allow the grantor’s Social Security number while the grantor is alive. For an irrevocable trust, the trust usually needs its own EIN. Opening the account is only the start. You still need to move assets into it. Cash, taxable investment accounts, and some business interests may be transferred. Retirement accounts usually require special caution and shouldn’t be retitled casually.

The Retainer Checklist: 5 Questions to Ask Before You Pay

Before paying a lawyer, ask whether the quoted price is a true flat fee or hourly estimate. Confirm whether the package includes a pour over will, healthcare directive, and power of attorney. Ask whether deed recording and trust funding are included. Find out what future amendments cost. Finally, ask whether your trust needs its own EIN or tax return. These questions protect you from paying for a trust that looks complete but still leaves important work unfinished.

Conclusion

The cost to set up a trust shouldn’t be judged only by the cheapest upfront price. A $300 template may look attractive, but it can become expensive if your assets aren’t funded correctly or your family ends up in probate. A $2,500 attorney drafted trust may feel costly today, but it can save heirs months of delay, court fees, and confusion later.

The right budget depends on your estate size, family complexity, property ownership, tax exposure, and how much guidance you need. If your life is simple, DIY may be enough. If your assets, family, or tax situation is complex, professional planning is usually worth the investment.