: Ranked by Age & Goal")

There isn’t one best investment accounts for kids that fits every family. The right choice depends on your child’s age, the purpose of the money, your need for tax benefits, and how much control you want over the account later.

If the goal is college, a 529 plan often gives the strongest tax advantages. If the goal is flexible wealth building, a custodial account may work better. If your teenager has earned income, a A Roth IRA for a child can be one of the most powerful tools for building long-term wealth, giving their money decades to grow tax-free. But choosing the right account starts with more than just picking an investment product. The real question is: What do you want this money to help your child achieve when they become an adult? Once that vision is clear, the right strategy becomes much easier to build around it.

The 18-Year Generational Compounding Calculator

A child’s biggest advantage isn’t income. It’s time. Imagine investing $100 per month from birth to age 18. At a 7% average annual return, that could grow into a meaningful five-figure account before adulthood. If the money stays invested longer, the compounding effect becomes far more powerful. That’s why parents and grandparents often regret waiting. A small monthly contribution made early can beat a larger contribution made late. A calculator helps you compare monthly deposits, expected return, time horizon, and final balance so the decision feels concrete instead of abstract.

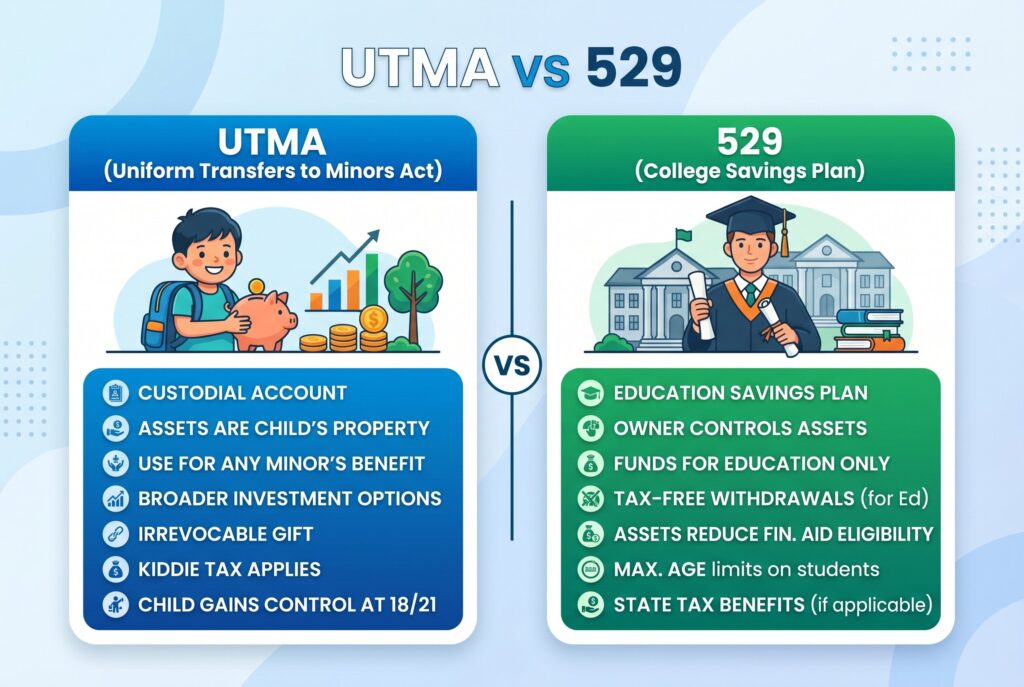

The Core Dilemma: UTMA vs 529

The most common debate is UTMA vs 529. Both can be useful, but they solve different problems. A 529 plan is built for education. Money can grow tax-deferred, and withdrawals may be tax-free when used for qualified education expenses. This can include college costs and certain other education-related expenses, depending on current rules.

A UTMA or UGMA is a custodial account for kids. It’s a brokerage account for kids managed by an adult custodian until the child reaches the age of majority under state law. Unlike a 529, the money doesn’t have to be used for school. Your child may eventually use it for a car, business, first apartment, travel, or general wealth building.

That flexibility is powerful, but it has a catch. Assets in a UTMA or UGMA legally belong to the child. Once control transfers, the parent can’t simply take the money back or redirect it. Custodial assets may also affect financial aid more heavily than parent-owned 529 assets. So the decision is simple: use a 529 when education is the main goal. Use a UTMA or UGMA when flexibility matters more than college-specific tax treatment.

Ranked by Age: The Right Account at the Right Time

1. Age 0 to 5: The Baby Phase

For a newborn or toddler, many parents first think about a savings account for baby. That can be useful for cash gifts, birthday money, or short-term needs, but it usually won’t build long-term wealth by itself. At this age, time is the biggest advantage, but the right account depends on what the money is meant to do. If the goal is education, a 529 plan is often the strongest fit because the tax benefits are built around qualified education expenses. If you want the child to have more flexibility as an adult, a UTMA or UGMA account may make sense, though the assets typically become theirs once they reach the age of majority.

For families who want more control, especially when larger sums are involved, a trust can serve a different purpose. It is less about maximizing tax benefits and more about setting rules: when the child can access the money, what it can be used for, and how much control they receive at different ages. That distinction matters. A 529 answers the question, “How do we fund education efficiently?” A custodial account answers, “How do we give the child flexible assets?” A trust answers, “How do we protect and guide the use of wealth over time?” The best choice starts with the purpose, not the product.

2. Age 6 to 12: The Scholar Phase

The elementary and middle school years are an ideal time to teach financial ownership. A custodial brokerage account can help children see how investing works, from owning fractional shares to understanding diversification and long-term growth. The goal isn’t to create young traders, it’s to show that money can become ownership in real businesses.

At this stage, many families benefit from using more than one account, with each serving a distinct purpose. A 529 plan can remain dedicated to education expenses, helping parents and grandparents contribute toward future college or vocational training costs in a tax-efficient way. A custodial brokerage account, on the other hand, can serve as a hands-on investing classroom. Children can follow their investments, learn how markets work, and see the impact of long-term compounding. The account can also provide flexibility for future goals that may have nothing to do with education, such as starting a business, making a down payment on a home, or pursuing other opportunities as a young adult.

Separating these goals often makes planning easier. The 529 is designed to answer the question, “How will we pay for education?” The custodial account addresses a different question: “How can we build financial skills and create flexible assets for the future?” When each account has a clear role, families can save and invest with greater purpose and fewer trade-offs.

3. Age 13 to 17: The Teen Phase

Teenagers may be ready for more responsibility. Some platforms now offer teen investing accounts with parental oversight, which can help a young person learn before managing money alone. This is also the age when an IRA for kids becomes relevant. A custodial Roth IRA requires earned income. Babysitting, lifeguarding, retail work, tutoring, or other legitimate paid work may qualify if properly documented.

For teenagers with earned income, a Roth IRA can be one of the most powerful long-term investing accounts available. Unlike accounts designed for education or general savings, a Roth IRA is built specifically for retirement, allowing investments to grow tax-free over time. The real advantage is the timeline. Contributions made at age 16 or 18 may remain invested for 40, 50, or even 60 years before retirement. Few other financial decisions offer that much time for compounding to work.

There are limits to keep in mind. Contributions cannot exceed the child’s earned income for the year, and annual IRA contribution limits still apply. Even so, early contributions can give a young investor a meaningful head start on retirement savings.

How to Open a Brokerage Account for a Child

Parents often ask how to open a brokerage account for a child. The process is usually straightforward, but the account type matters.

- First, choose the structure. For general investing, look at UTMA or UGMA custodial accounts. For education, consider a 529 plan. For a working teen, consider a custodial Roth IRA.

- Second, gather information. You’ll typically need the custodian’s name, address, Social Security number, date of birth, and employment information. You’ll also need the child’s legal name, date of birth, and Social Security number.

- Third, open the account through a brokerage, bank, or 529 provider. Link a funding account and set up automated contributions. Automation matters because it turns good intentions into a monthly habit.

- Fourth, choose investments carefully. For long timelines, many families use diversified index funds or target-date education portfolios. Avoid overly complex strategies. A child’s investment account should be built for patience, not speculation.

Common Mistakes Parents Should Avoid

Choosing an Account Before Defining a Goal

Many parents start by asking which account is best: a 529 plan, UTMA, Roth IRA, or trust. In reality, the better starting point is identifying the goal. Different accounts are designed for different outcomes. A 529 is built for education expenses, a Roth IRA supports long-term retirement savings, a custodial account provides flexibility, and a trust can offer greater control over how assets are managed and distributed. Choosing the wrong structure can lead to unnecessary restrictions, tax consequences, or planning challenges later. The account should support the objective, not determine it.

Misunderstanding Who Owns the Money

Ownership rules are often overlooked. In a custodial account such as a UTMA or UGMA, the assets belong to the child from the moment they are contributed. The parent acts as the custodian and manages the account, but the funds are not the parent’s property. This distinction becomes important when the child reaches the age of majority. At that point, control typically transfers to the child, who can use the money as they see fit. Families who want to retain greater control over future distributions may need to consider other structures, such as trusts.

Keeping Long-Term Money in Cash

Safety is important, but excessive caution can create its own risks. Many parents leave children’s savings entirely in cash or traditional savings accounts for years, even when the money is not expected to be used until adulthood. Over long periods, inflation can reduce purchasing power and limit growth. Investment accounts designed for children allow families to take advantage of time, which is often the most valuable asset a young investor has. A longer time horizon generally creates more opportunities for compounding to work.

Conclusion

The best investment accounts for kids depends on what you want the money to accomplish. Choose a 529 plan for education. Choose a UTMA or UGMA for flexible investing. Choose a custodial Roth IRA for a teen with earned income. Consider a trust fund for kids when control, protection, and long-term family planning matter.

There are many investment accounts for kids, but the best one is the account your family understands, funds consistently, and uses with purpose. Start early, keep the structure simple, automate contributions, and teach your child what the money means. The real gift isn’t only the account balance. It’s giving your child time, options, and a calmer financial start.