The most common mistake when opening a trust account is confusing two separate steps. Creating the trust is a legal step, usually handled with an attorney or estate planning platform. Opening the bank account is the execution step, where the trust receives a checking, savings, or brokerage account in its own legal name. If you arrive with incomplete documents, the wrong tax ID, or incorrect account titling, the bank may delay or reject the request. A trust account works best when the paperwork, trustee authority, and funding plan are prepared before you walk into the branch.

What Is a Trust Account?

A trust account is a financial account managed by a trustee on behalf of a trust and its beneficiaries. The trustee is responsible for handling the account according to the terms of the trust agreement, while the assets in the account are held for the benefit of the individuals or organizations named in the trust. Trust accounts are commonly used for estate planning, asset management, and wealth transfer.

How to Open a Trust Account

Step 1: The Legal Prerequisites

Before asking a bank how to set up a trust, make sure the trust already exists. A bank doesn’t create your estate plan. It opens an account for a trust that has already been legally drafted and signed. At minimum, you usually need a signed trust agreement or a shorter Certificate of Trust. The Certificate of Trust is often preferred at the bank because it confirms the trust name, date, trustee powers, and trustee identity without exposing private inheritance details. Also confirm that the trust document allows the trustee to open bank accounts, deposit funds, write checks, transfer money, and manage financial assets. If those powers are unclear, the bank may ask for legal review before opening the account.

Step 2: SSN vs. EIN

The tax ID question is one of the biggest causes of delay. A revocable trust often uses the grantor’s Social Security number while the grantor is alive because the trust is usually treated as the same taxpayer. That means the income is generally reported under the grantor’s personal tax return.

An irrevocable trust usually needs its own Employer Identification Number, also called an EIN. The same may apply after a grantor dies and a revocable trust becomes irrevocable. If you are unsure which tax ID applies, ask your attorney or tax professional before going to the bank. Using the wrong number can create reporting problems, rejected applications, or later account corrections. This is why the tax ID should be confirmed before you open trust account paperwork.

Step 3: The Ultimate Bank Document Checklist

To make the process smoother, prepare a clean folder before your appointment. Bring the Certificate of Trust or trust agreement, government issued photo ID for every trustee who will sign, the trust’s EIN letter if required, and any amendments to the trust. You should also bring the opening deposit. Some basic trust checking accounts may require around $100 to $500, while trust brokerage accounts or managed trust accounts may require higher minimums. Ask the bank in advance whether all trustees must appear in person. Some institutions require every acting trustee to sign signature cards, while others allow one trustee to act alone if the trust document clearly grants that authority.

Step 4: Account Titling

Account titling is where small mistakes can become serious. A personal account in your name isn’t the same as a trust account. The account must be titled in the legal name of the trust. A clear format might look like this: John Doe and Jane Doe, Trustees of the Doe Family Trust, dated January 1, 2026. If the bank shortens or changes the title incorrectly, ask for clarification before funding the account. The title should match the trust documents closely enough to show that the account belongs to the trust, not to the trustees personally.

Step 5: Funding the Account

Opening the account isn’t the finish line. Funding is what gives the account value and purpose. You may transfer cash from personal accounts, deposit checks payable to the trust, or move taxable investment assets into a trust brokerage account. Be careful with retirement accounts. Many retirement accounts shouldn’t simply be retitled into a trust because tax consequences can be serious. In many cases, beneficiary designations are handled separately. Only assets that are properly transferred into the trust structure can help support probate avoidance. An empty trust account doesn’t protect money that remains outside the trust.

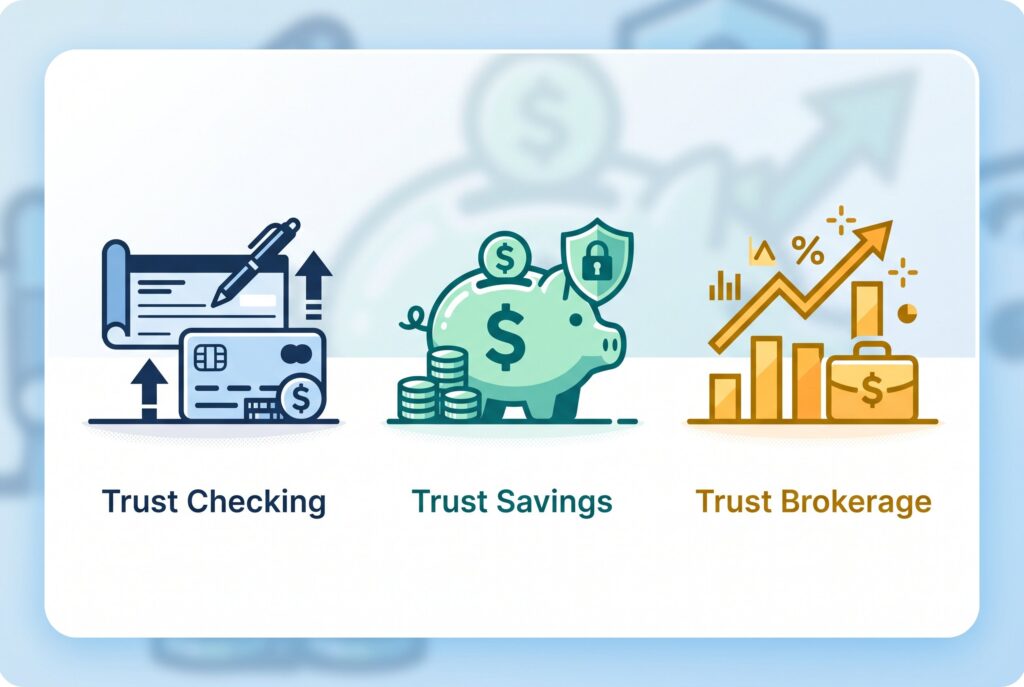

Trust Checking vs. Trust Savings vs. Trust Brokerage

A trust checking account is useful for paying bills, property expenses, taxes, insurance, and distributions. A trust savings account is better for holding cash reserves. A trust brokerage account is used for stocks, bonds, ETFs, mutual funds, and other investments. The right choice depends on the trust’s purpose. A family trust holding a house may need checking for maintenance costs. A long term inheritance trust may need brokerage access. A trust designed for short term estate administration may need both checking and savings.

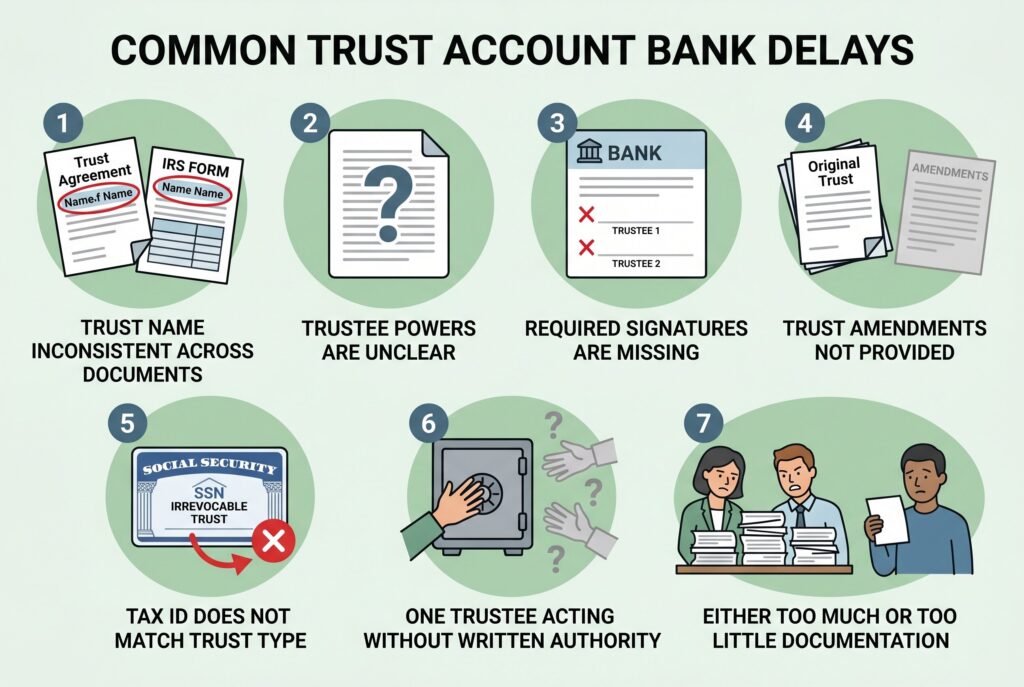

Common Reasons Banks Delay Trust Accounts

Trust Name Is Inconsistent Across Documents

One of the most common reasons a bank pauses the review process is that the trust name isn’t identical on every document. Even small discrepancies, such as abbreviations, punctuation differences, missing words, or an outdated trust name after an amendment, can raise compliance concerns. Banks must verify that the trust opening the account is the same legal entity referenced throughout the documentation. To avoid delays, review all trust-related documents before the appointment and ensure the trust name matches exactly across the trust agreement, certification of trust, tax records, and any amendments. If the trust name has changed, bring the amendment that documents the change.

Trustee Powers Are Unclear

Banks are required to confirm that trustees have the authority to open, manage, and transact on financial accounts. If the trust documents don’t clearly define those powers or contain ambiguous language, the bank may request additional documentation before proceeding. To prevent this issue, review the trust agreement or certification of trust in advance and confirm that trustee banking powers are clearly stated. If the language could be interpreted in different ways, consider obtaining a clarification letter from the attorney who prepared the trust.

Required Signatures Are Missing

Many trusts require signatures from all acting trustees or co-trustees before financial accounts can be opened or modified. Missing signatures can stop the process because the bank can’t verify that all required parties have approved the transaction. Before meeting with the bank, confirm whether all trustees must sign in person or whether notarized or remote signatures are acceptable. Carefully review all paperwork beforehand to ensure every required signature has been completed.

Trust Amendments Aren’t Provided

A bank may receive the original trust agreement without the amendments that modified trustee authority, beneficiary designations, or other key provisions. Without a complete record, the institution can’t determine the trust’s current terms and may suspend the review until additional documents are provided. To avoid this problem, bring every executed amendment along with the original trust agreement and organize the documents in chronological order so the bank can easily verify the most current version of the trust.

The Tax ID Doesn’t Match the Trust Type

Banks routinely verify taxpayer identification information as part of their compliance process. Issues can arise when the tax identification number provided doesn’t align with the trust’s legal structure. For example, a revocable trust may use the grantor’s Social Security Number, while an irrevocable trust often requires its own Employer Identification Number (EIN). Before the appointment, confirm the correct tax ID with your attorney, CPA, or tax advisor and bring supporting documentation that explains the trust’s tax status if necessary.

One Trustee Is Acting Without Written Authority

When a trust has multiple trustees, the bank must determine whether one trustee can act independently or whether all trustees must act together. If a single trustee attempts to complete the process without documentation showing individual authority, the bank may refuse to proceed. Reviewing the trust agreement beforehand can help clarify these requirements. If one trustee is authorized to act on behalf of the others, bring written authorization, trustee resolutions, powers of attorney, or any other documents the bank may require to verify that authority.

The Bank Receives Either Too Much or Too Little Documentation

Privacy concerns can create unexpected delays during the review process. Some families provide only the complete trust agreement, which may contain sensitive personal information the bank doesn’t need. Others provide only a brief summary that lacks the details required for verification. Both situations can slow the process because the bank either has excessive information to review or insufficient information to approve the account. The best approach is to contact the bank before the appointment and ask exactly which trust documents it accepts. Many institutions prefer a Certification of Trust because it provides the necessary legal information while protecting the family’s privacy.

Conclusion

Knowing how to open a trust account isn’t only about filling out a bank form. It’s about making sure the legal trust, tax ID, trustee authority, account title, and funding steps all work together. Before visiting the bank, confirm the trust is signed, gather the Certificate of Trust, verify whether you need an SSN or EIN, prepare trustee IDs, ask about minimum deposits, and review the exact account title. Once the account is open, fund it properly and keep records of every transfer. A trust account can help organize assets, support estate planning, and reduce probate problems, but only when it’s opened and funded correctly.

Related Articles

How Much Does It Cost to Set Up a Trust in 2026? (Full Fee Breakdown)