Welcoming a baby changes the way parents think about money. Suddenly, every cash gift, birthday check, and small transfer from grandparents feels like the beginning of something bigger. That is why many families start by opening a savings account for baby funds. It feels safe, simple, and responsible.

But in 2026, saving alone may not be enough. If your child has an eighteen year runway before adulthood, the biggest question isn’t only where to store the money. It’s how to protect its value from inflation and help it grow with purpose. A traditional savings account may keep the money separate, but a low interest rate can quietly weaken its future buying power.

The smartest plan usually combines safety, growth, and education. Parents may use a high yield savings account for short term cash, a 529 plan for education, or an investment account for kids when the goal is long term wealth building.

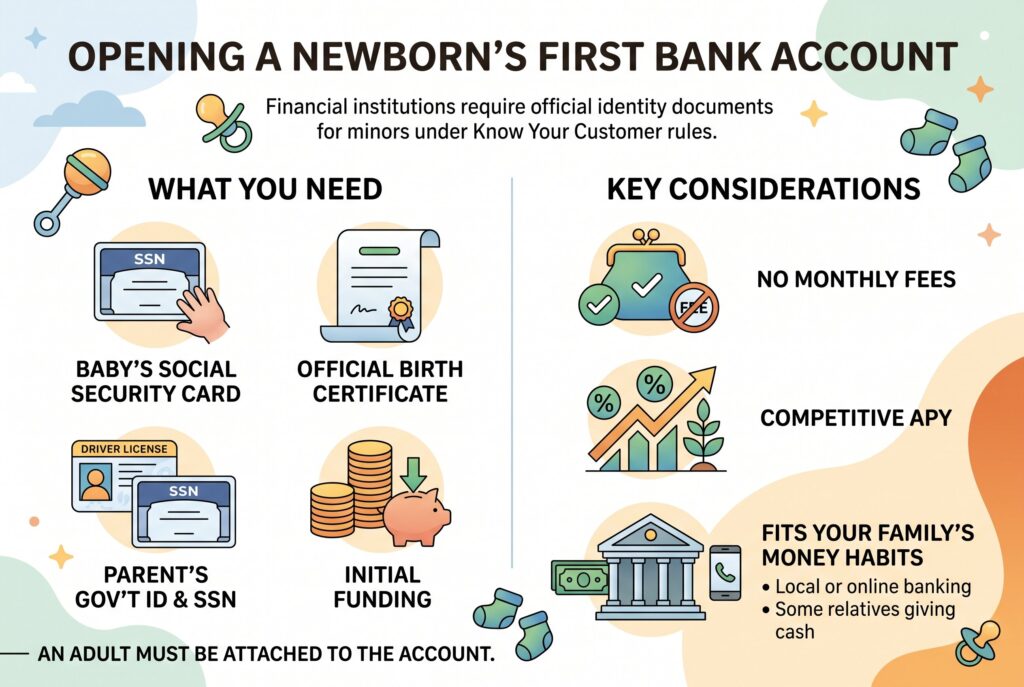

The Logistical Reality: What You Need to Open the Account

Required Documents to Open an Account for a Newborn

You usually can’t open an account for your newborn immediately after leaving the hospital. Financial institutions must follow Know Your Customer rules, which means they need official identity documents before opening an account for a minor.

The biggest requirement is your baby’s Social Security Number. Many parents have to wait a few weeks after birth before the card arrives. You may also need the official birth certificate, your government-issued ID, your Social Security Number, your address, and funding information for the first deposit. This paperwork applies whether you are opening a standard savings account or researching how to open a brokerage account for a child. The account may be for your baby, but an adult must be legally attached to it.

Why You May Need to Wait Before Opening the Account

One of the most common reasons parents cannot open an account immediately after birth is the delay in receiving the baby’s Social Security Number. Since most banks and investment firms require this information to verify identity, account applications often must wait until the necessary documents are issued.

What to Look for When Choosing a Bank

Before choosing a bank, check three things. First, confirm there is no monthly maintenance fee. Second, look for a competitive APY. Third, make sure the account fits how your family actually handles money. For example, online banks may offer better rates, but they can make cash deposits difficult. If relatives give your child physical cash, you may need a local bank or credit union for deposits, then transfer the money into a high-yield account afterward.

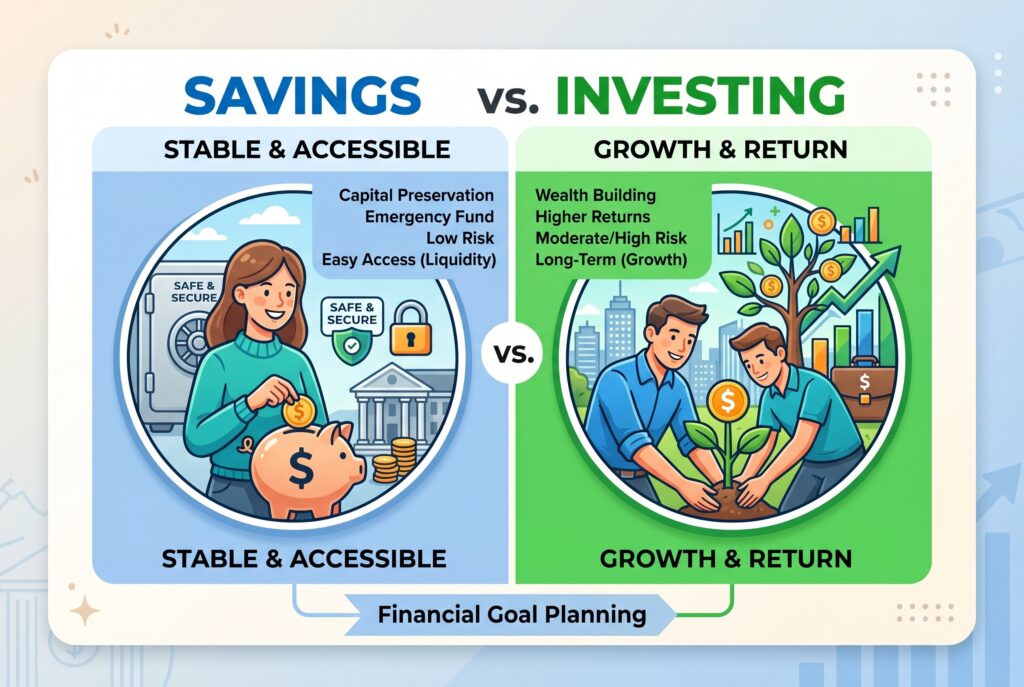

Savings vs. Investing: Choosing the Right Vehicle

A baby has something most adults don’t: decades of time. That time is one of the most powerful financial advantages your child will ever have because it allows savings and investments to benefit from compound growth for many years. Even small contributions made during childhood can grow into substantial amounts by adulthood. Because of this advantage, every dollar gifted to your child should have a specific purpose. Not all money should be treated the same way. A balanced approach often works best. Some funds should remain safe and easily accessible for short-term needs, emergency expenses, or future purchases. These dollars are typically best kept in a high-yield savings account where they can earn interest while remaining available when needed.

Other funds can be invested for long-term growth. Since a newborn may not need the money for many years, parents often have the ability to take a longer investment horizon and potentially accept more market volatility in exchange for higher growth potential. Over time, investments such as broad-market index funds have historically outperformed traditional savings accounts, although they also carry risk. Parents may also want to set aside money specifically for education expenses. College costs continue to rise, making dedicated education savings an important part of many families’ financial plans. Separating education funds from general savings can help ensure that money intended for future tuition and academic expenses is not accidentally used for other purposes.

Ultimately, the best investment account for kids depends on the goal. A high-yield savings account may be ideal for short-term flexibility and security. A custodial brokerage account can help build long-term wealth through investing. A 529 college savings plan may be the most tax-efficient choice for education funding. Many families choose a combination of these accounts so that every dollar has a clear role in supporting their child’s future.

High Yield Savings Accounts for Short Term Cash

A high yield savings account is best for money you may need within the next few years. This includes baby shower cash, holiday gifts, medical savings, childcare costs, preschool expenses, or a small emergency fund for the child.

The advantage is safety. The money is easy to access and usually protected by federal deposit insurance when held at an eligible institution. The downside is limited growth. Even a strong APY may not beat the long term returns of a diversified investment portfolio. That is why a savings account is useful, but it shouldn’t be the only plan for money meant to sit for eighteen years. A smart approach is to keep short term baby money in a high yield savings account, then direct long term contributions into investment accounts for kids.

Custodial Accounts for Long Term Flexibility

If you want flexibility beyond education, a brokerage account for kids may be worth considering. These accounts are often structured as UTMA or UGMA custodial accounts. A custodial account allows an adult to invest on behalf of a child. The money can be invested in stocks, ETFs, mutual funds, and other eligible assets. This gives the funds more growth potential than a savings account.

The tradeoff is control. Money placed into a custodial account is usually considered an irrevocable gift to the child. When the child reaches the age of majority, often eighteen or twenty one depending on state law, they gain full control of the account. That can be wonderful if your child is financially mature. It can be risky if they are impulsive. Parents should think carefully before placing large sums into a custodial account without also teaching financial responsibility.

The 529 Plan for Education Goals

When comparing UTMA vs 529 options, the 529 plan is often the stronger choice for education. A 529 plan is designed for qualified education expenses. The money can grow tax advantaged, and qualified withdrawals may be tax free. This can make it one of the most powerful college savings tools available.

The limitation is purpose. If the money is used for nonqualified expenses, taxes and penalties may apply to earnings. Newer rules have improved flexibility in certain cases, but a 529 is still primarily an education account. If your family is confident the money will be used for school, a 529 deserves serious attention. If you want the child to use the funds for a first business, home purchase, or other adult milestone, a custodial brokerage account may offer more flexibility.

How To Decide Which Account Is Right For Your Child

If you’re unsure whether to choose a 529 plan, a custodial brokerage account, or a simple savings account, work through these questions:

Step 1: Define the Primary Goal for the Money

Start by asking what the funds are intended to accomplish. If the primary goal is paying for college, trade school, or other qualified education expenses, a 529 plan is often the most tax-efficient choice. If the goal is broader, such as helping with a first home purchase, starting a business, or building long-term wealth, a custodial account may be more appropriate.

Step 2: Consider How Much Flexibility You Want

A 529 plan offers valuable tax benefits, but it comes with rules regarding how the money can be used. A custodial brokerage account provides much greater flexibility because the funds can be spent on virtually any purpose that benefits the child once they gain control of the account.

Step 3: Evaluate Your Time Horizon

The longer the money can remain invested, the more opportunity it has to grow. If your child is still very young and the funds will not be needed for many years, investment-based accounts may make sense. If the money may be needed within a few years, keeping a portion in savings can reduce risk.

Step 4: Think About Who Should Control The Money

With a 529 plan, the account owner typically maintains control of the funds. With a UTMA or UGMA custodial account, ownership eventually transfers to the child when they reach the age of majority, which varies by state.

Step 5: Consider Using More Than One Account

Many families do not choose a single account type. Instead, they combine accounts to match different goals. For example, they may use a 529 plan for education savings, a custodial brokerage account for long-term wealth building, and a high-yield savings account for gifts and short-term needs.

Beyond Savings: Avoiding the Trust Fund Baby Trap

As your child’s balance grows, you may start thinking beyond savings accounts and basic investing.

A trust fund baby is often imagined as a spoiled heir who receives too much money too early. In real planning, a trust can do the opposite. It can protect a child from receiving a large sum before they are ready. Unlike a custodial account, a trust can include rules. Parents can decide when money is distributed, what it can be used for, and who manages it. For example, a trust might pay for education at any age, release part of the funds at twenty five, and hold the rest until thirty.

A trust fund for kids is usually more expensive to create than a savings account, 529, or custodial account. But for larger balances, blended families, special needs planning, business ownership, or creditor protection, it can be the most controlled structure. The goal isn’t to create entitlement. The goal is to create guardrails.

Conclusion

Opening a savings account for baby funds is a meaningful first step. It gives your child’s money a home and helps your family build financial habits early.

But don’t stop there. Cash gifts sitting in a low interest account for eighteen years may lose power to inflation. A better strategy is to match each dollar with the right purpose. Use a high yield savings account for short term cash. Use a 529 for education. Use a custodial brokerage account for flexible long term investing. Consider a trust when control and protection matter most. Your baby’s first funds are more than money. They are a chance to build habits, start conversations, and create a foundation for adulthood. The earlier you begin, the more time can work in your child’s favor.