vs. Traditional: How to Choose by Your 2026 Income")

Choosing between a Roth 401(k) and Traditional 401(k) can feel like decoding retirement jargon, but the core decision is simple: pay tax now or pay tax later. When comparing traditional 401(k) vs Roth 401(k), a Roth 401(k) uses after-tax contributions. You pay income tax today, then qualified withdrawals can be tax-free later. A Traditional 401(k) uses pre-tax contributions. You reduce taxable income today, then withdrawals are taxed as ordinary income in retirement. The real question isn’t “Which account is better?” It’s “Which tax rate is likely better for me: today’s rate or my future retirement rate?”

Roth vs. Traditional Optimizer

Use this quick framework. Choose Roth if your current tax bracket is lower than the bracket you expect in retirement. Choose Traditional if your current bracket is higher than your expected retirement bracket. If the two are close, consider splitting contributions between both. For example, a young worker in a lower bracket may benefit from Roth because today’s tax cost is relatively small. A peak earner in a high bracket may benefit from Traditional because the current deduction is more valuable. This is the core debate behind traditional vs Roth 401(k) planning strategies.

The Core Concept: Decoding Tax Now vs. Tax Later

Traditional 401(k)

Traditional 401(k) tax benefits happen upfront. Contributions generally reduce taxable income in the year you make them. If you contribute $10,000, you may reduce current taxable income by $10,000. That immediate tax break can be powerful, especially for high earners. But retirement withdrawals are taxable. You’re delaying the tax bill, not avoiding it.

Roth 401(k)

A Roth 401(k) reverses the timing. You contribute after-tax dollars, so your paycheck may feel smaller today. In exchange, qualified withdrawals can be tax-free later. That tax-free growth can be valuable over decades. Roth 401(k) withdrawal rules generally require a qualified distribution, which means meeting the account’s timing rules and age or qualifying event requirements.

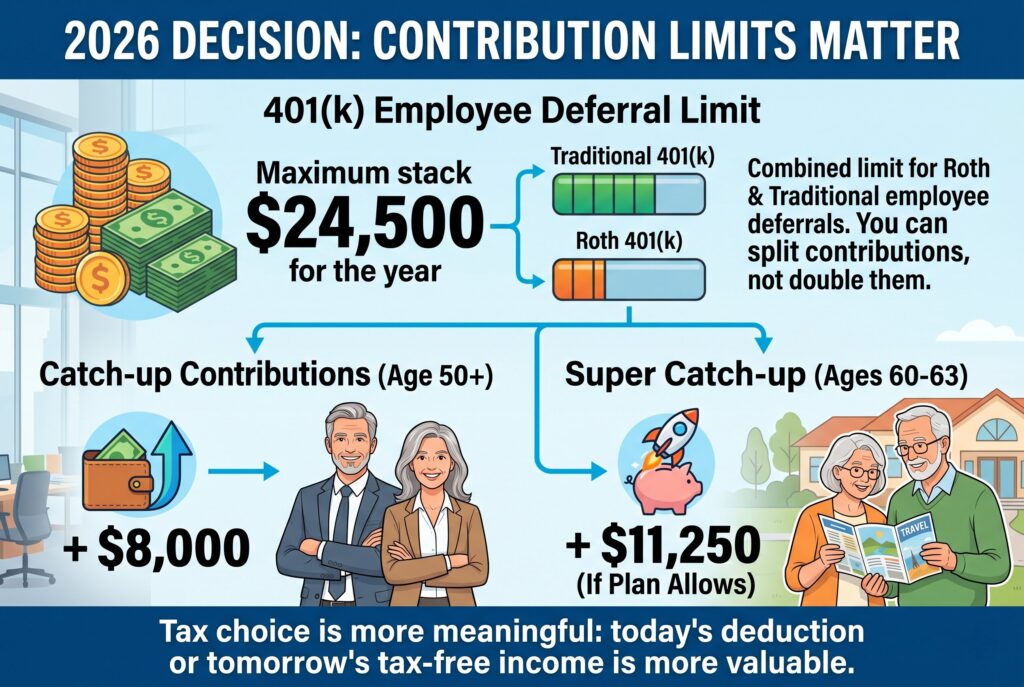

Analyzing the 2026 Decision: Contribution Limits Matter

For 2026, the IRS increased the employee 401(k) contribution limit to $24,500. The catch-up contribution limit for workers age 50 and older is $8,000, while workers ages 60 to 63 may be eligible for an $11,250 “super catch-up” if their plan allows it.

These 401(k) contribution limits apply across Roth and Traditional employee deferrals combined. You can split contributions, but you can’t contribute $24,500 to Roth and another $24,500 to Traditional in the same year. Roth 401(k) contribution limits 2026 matter because higher limits make the tax choice more meaningful. The more you contribute, the more important it becomes to decide whether today’s deduction or tomorrow’s tax-free income is more valuable.

Choosing by Your 2026 Income: The Income Bracket Rules of Thumb

| Current vs. Future Tax Bracket |

General 401(k) Recommendation |

Strategic Rationale |

| Expect higher bracket in retirement | Roth 401(k) | Lock in today’s lower rate and build tax-free growth |

| Expect lower bracket in retirement | Traditional 401(k) | Take the deduction now and pay later at a lower rate |

| Expect similar brackets | Diversify | Split contributions for future flexibility |

Case 1: You’re a low to moderate earner today

If you’re early in your career, in school part-time, building a business, or temporarily earning less than usual, Roth may be attractive. Paying tax now in a lower bracket can be a smart trade for tax-free withdrawals later. This is why Roth 401(k)s often make sense for younger workers. Their income may rise over time, and decades of tax-free growth can become meaningful.

Case 2: You’re a peak earner in 2026

If you’re in your highest earning years, Traditional may be more compelling. A deduction taken in a high marginal tax bracket can be extremely valuable. This is especially true if you expect lower taxable income in retirement. Many retirees spend less, stop earning wages, or use a mix of taxable, tax-deferred, and Roth accounts to manage tax brackets.

Nuances Beginners Miss

Employer Matching Contributions

Employer matching contributions complicate the picture. Even if your personal contributions are Roth, your employer match may be treated differently depending on plan rules. Many matching contributions have historically been pre-tax, meaning they’re taxed when withdrawn. So don’t assume your entire account is Roth. Your statement may show separate Roth, Traditional, and employer match balances.

Required Minimum Distributions

Required Minimum Distributions, or RMDs, used to be a major Roth 401(k) drawback. That changed. The IRS states that account owners aren’t required to take withdrawals from designated Roth accounts in a 401(k) or 403(b) plan while alive, though beneficiaries may still face RMD rules. Traditional 401(k)s generally remain subject to RMD rules. This gives Roth 401(k)s more flexibility for long-term retirement and estate planning.

Roth 401(k) Income Limits vs. Roth IRA Limits

A common misunderstanding is Roth 401(k) income limits. Roth IRAs have income limits, but Roth 401(k)s generally don’t. If your employer plan offers a Roth 401(k), high income alone usually doesn’t block you from contributing. That makes Roth 401(k)s especially useful for high earners who can’t contribute directly to a Roth IRA.

The Roth 401(k) 5-year Rule

The Roth 401(k) 5-year rule matters for qualified withdrawals. To get tax-free treatment on earnings, the account generally must satisfy the five-year period and the distribution must meet a qualifying condition, such as reaching age 59½. This doesn’t mean Roth is bad. It means the account works best when used as a long-term retirement tool, not a short-term savings account.

High-earner Catch-Up Contributions

SECURE 2.0 added another wrinkle. IRS final regulations require catch-up contributions made by certain higher-income participants to be designated as after-tax Roth contributions. That means some high earners may have less choice for catch-up dollars starting under the new rules, making Roth education more important than ever.

Conclusion

Roth 401(k) vs traditional isn’t a universal winner-take-all decision. Roth often shines when your current tax rate is low, your future tax rate may be higher, or you want tax-free retirement income. Traditional often shines when your current tax rate is high and you expect lower taxable income later. The smartest approach may be tax diversification: using both account types so retirement gives you options. Your income, age, state taxes, employer match, and future withdrawal strategy all matter.

The best 401(k) decision isn’t the one that sounds best on paper. It’s the one that fits your 2026 income and the retirement tax picture you’re building toward.