What is a mega backdoor Roth, and why are high earners so interested in it in 2026? The short answer: it can turn unused 401(k) space into a powerful long-term Roth engine. For professionals who earn too much for direct Roth IRA contributions and already max out standard 401(k) deferrals, the mega backdoor Roth may open the door to tens of thousands of extra Roth dollars each year. The key is understanding the mega backdoor Roth limit 2026, your employer’s plan rules, and the tax steps required to execute it cleanly.

The 2026 Mega Backdoor Roth Limits & The Math

The mega backdoor Roth limit 2026 depends on three numbers: the IRS total plan limit, your regular employee deferral, and your employer contribution.

For 2026:

Employee deferral limit: $24,500

Total plan contribution limit under age 50: $72,000

Total limit age 50+: $80,000

Total limit age 60–63: $83,250

Your mega backdoor space is:

Maximum after-tax contribution = Total plan limit – employee deferral – employer match

Example:

You’re under 50.

You contribute $24,500 to your 401(k).

Your employer contributes $12,000.

Your total 2026 plan limit is $72,000.

$72,000 – $24,500 – $12,000 = $35,500

That means you may have $35,500 of after-tax contribution room if your plan allows the strategy.

This is why the mega backdoor is so valuable. A regular retirement contribution limit can feel small to a high-income saver. But unused space under the total 401(k) limit can become a much larger Roth opportunity.

Interactive Tool: The 2026 Mega Backdoor Space Calculator

To estimate your own space, use this simple calculator logic:

- Start with your age-based total plan limit.

- Subtract your employee 401(k) deferral.

- Subtract your employer match or profit-sharing contribution.

- The remaining amount is your possible after-tax contribution space.

For example, if your total limit is $72,000, your employee deferral is $24,500, and your employer contributes $15,000, your possible space is $32,500. The most important word is “possible.” Your actual ability to use it depends on your plan document, payroll setup, and compliance testing.

2026 Mega Backdoor Space Calculator

Use this calculator to estimate your possible 2026 mega backdoor Roth after-tax contribution space. Start with your age-based total plan limit, then subtract your employee 401(k) deferral and employer match or profit-sharing contribution.

Possible After-Tax Contribution Space = Age-Based Total Plan Limit − Employee 401(k) Deferral − Employer Contribution

Example: $72,000 − $24,500 − $15,000 = $32,500

Note: The most important word is “possible.” Your actual ability to use this space depends on your plan document, payroll setup, after-tax contribution feature, Roth conversion or rollover access, and compliance testing.

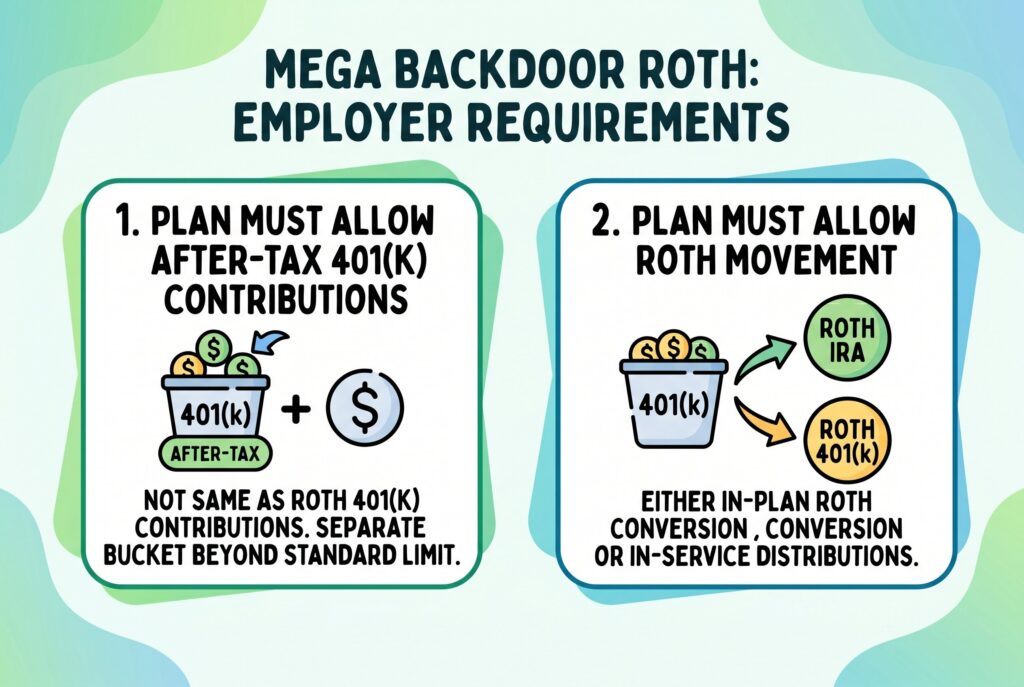

Does Your Employer Allow It? The 2 Strict Requirements

The mega backdoor isn’t something you can create on your own inside a normal IRA. It depends on employer plan design.

Requirement 1: Your plan must allow after-tax 401(k) contributions.

These aren’t the same as Roth 401(k) contributions. Roth 401(k) contributions are part of your normal employee deferral limit. After-tax non-Roth contributions are a separate bucket that may allow you to contribute beyond the standard $24,500 employee deferral limit.

Requirement 2: Your plan must allow Roth movement.

The plan must allow either in-plan Roth conversions or in-service distributions. An in-plan conversion moves the after-tax money into a Roth 401(k). An in-service distribution may let you roll the after-tax money into a Roth IRA while still employed. If your plan allows after-tax contributions but doesn’t allow conversion or distribution, the strategy becomes much less useful because earnings may build up and become taxable later.

Step-by-Step Guide to Executing the Strategy

- Step 1: Max out your standard 401(k) deferral first.

For most high earners, the first move is contributing the full $24,500 employee deferral in 2026, either pre-tax or Roth depending on your tax strategy.

- Step 2: Calculate your remaining annual additions space.

Subtract your employee deferral and employer contributions from the total 2026 plan limit. This tells you how much after-tax contribution room may remain.

- Step 3: Fund the after-tax bucket through payroll.

This usually must be done through your employer’s payroll system. You’ll need to choose after-tax non-Roth contributions, not Roth 401(k) contributions.

- Step 4: Convert quickly.

Many modern plans offer an auto-convert feature that immediately sweeps after-tax contributions into the Roth bucket. This matters because after-tax principal generally isn’t taxed again, but earnings before conversion can be taxable.

- Step 5: Keep records.

You’ll want clear records showing what was after-tax principal, what was converted, and whether any earnings were taxed.

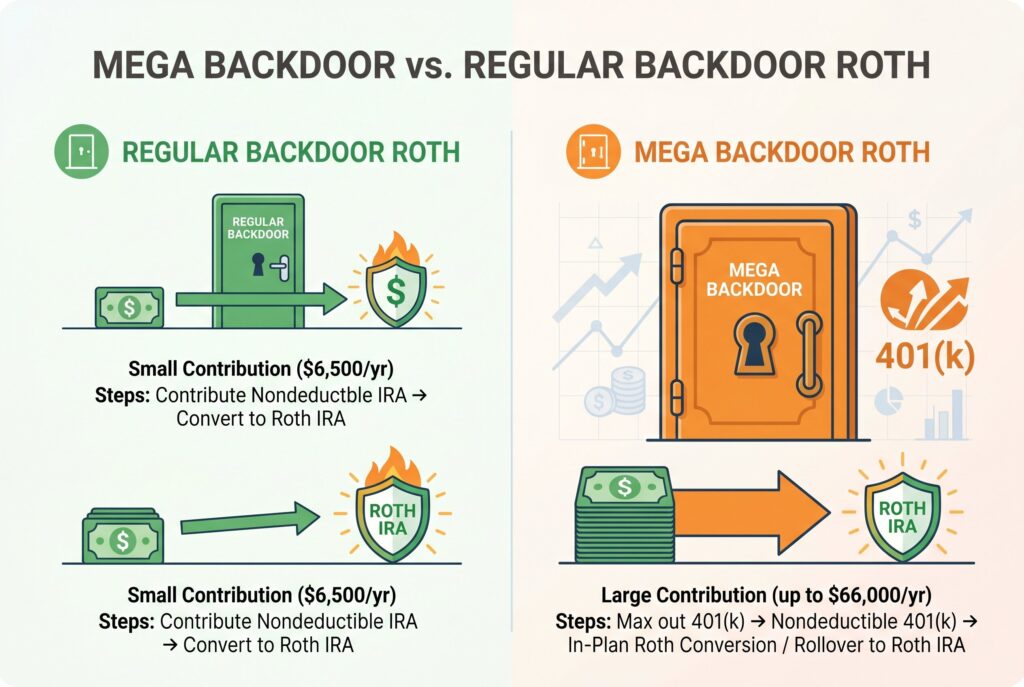

Mega Backdoor vs. Regular Backdoor Roth

A regular backdoor Roth answers a different question: what is a backdoor Roth IRA? It’s an IRA-based strategy where someone makes a nondeductible Traditional IRA contribution and then converts it to a Roth IRA. The regular backdoor Roth is limited by IRA contribution limits, often around $7,000 to $8,000 depending on age and year.

The mega backdoor Roth is much larger because it works through an employer-sponsored plan. Instead of moving only IRA-sized dollars, eligible savers may move tens of thousands into Roth accounts. There is another major difference: the pro-rata rule.

With a regular backdoor Roth, Traditional, SEP, and SIMPLE IRA balances can create taxable complications. With a mega backdoor Roth, 401(k) plans generally maintain separate accounting for contribution types, so existing pre-tax 401(k) assets usually don’t create the same IRA-style pro-rata problem. That said, earnings on after-tax 401(k) contributions may still be taxable if they aren’t converted quickly.

Compliance Traps: Nondiscrimination Testing & Notice 2014-54

The mega backdoor is powerful, but it isn’t frictionless. IRS Notice 2014-54 helped clarify how after-tax 401(k) money can be separated from pre-tax amounts when moved to Roth and traditional destinations. This guidance helped make the strategy more widely understood and accepted.

But highly compensated employees should pay attention to ACP nondiscrimination testing. If mostly high earners use the after-tax contribution feature and the plan fails testing, some after-tax contributions may be refunded.

That can be frustrating. You may think you completed the strategy, only to receive a refund later because the plan didn’t pass required testing. This is why HR and plan administrators matter. The strategy isn’t just about your personal savings capacity. It also depends on plan design, employee participation, and compliance results.

Conclusion

The mega backdoor Roth can be one of the most effective Roth-building strategies available to high earners in 2026. But it only works when three things line up: excess cash flow, enough unused 401(k) annual additions space, and an employer plan that allows after-tax contributions plus Roth conversion access.

Before you start, contact HR or your 401(k) plan administrator and ask for the Summary Plan Description. Confirm whether your plan allows after-tax non-Roth contributions, in-plan Roth conversions, in-service distributions, and auto-conversion. When used correctly, the mega backdoor isn’t just a tax tactic. It’s a disciplined way to move more long-term wealth into a tax-free Roth environment.

Related Articles

Backdoor vs. Mega Backdoor Roth: 2026 Key Differences Explained