Rule of 55 Explained (2026)")

Can I retire at 55? Yes, but retiring at 55 is very different from retiring at 65. You may gain freedom earlier, but you also create a longer retirement timeline, a bigger healthcare gap, and a more complicated withdrawal plan. The quick answer is this: you can retire at 55 if your savings can support 30 to 40 years of expenses, you have a plan for healthcare before Medicare, and you know how to access retirement money before age 59½. For many people, the key strategy is the rule of 55, also called the 401(k) rule of 55. Can you retire at 55 without this planning? Technically, yes. But doing it without a bridge-income strategy, tax plan, and realistic spending target can put your retirement at risk.

What Is the 401(k) Rule of 55?

The rule of 55 is a retirement account rule that may let you withdraw money from your current employer’s 401(k) or 403(b) without the usual 10% early withdrawal penalty. Here is the basic idea: if you leave your job in or after the year you turn 55, you may be able to take penalty-free withdrawals from that employer’s plan. This can apply whether you retire, resign, or are laid off.

The 401(k) rule of 55 is powerful because most retirement accounts have early withdrawal penalties before age 59½. But there are limits. It usually applies only to the plan from the employer you just left. It typically doesn’t apply to old 401(k)s from previous jobs or to IRAs. That means you need to be careful before rolling old workplace plans into an IRA. A rollover can simplify your finances, but it may remove access to the rule of 55 withdrawals.

Interactive Tool: Early Retirement Target Calculator

Early Retirement Target Calculator

Use this calculator to estimate whether early retirement at 55 may be realistic based on cash flow, not just account balance. Enter spending, healthcare costs, taxes, investment return, inflation, income sources, and account balances to estimate how long your savings may last.

Retirement Timeline

Annual Cash Flow Assumptions

Income Sources

Account Balances

| Milestone | Projected Balance | Status |

|---|---|---|

| At Medicare Age | $0.00 | Not calculated |

| At Social Security Start Age | $0.00 | Not calculated |

| At Planning Age | $0.00 | Not calculated |

Total Starting Savings = Taxable Brokerage + 401(k)/IRA + Roth + Cash Savings

First-Year Withdrawal Need = Annual Spending + Healthcare Before Medicare − Pension/Rental Income − Social Security, if active

Gross Withdrawal Need = Net Withdrawal Need ÷ (1 − Tax Rate)

Starting Withdrawal Rate = First-Year Gross Withdrawal ÷ Total Starting Savings × 100

Each Year: Balance grows by expected return, then inflation-adjusted withdrawal need is subtracted

Note: This is a simplified early retirement planning tool. It does not model market volatility, sequence-of-returns risk, account withdrawal ordering, penalties, Roth conversion ladders, ACA subsidies, required minimum distributions, changing taxes, or one-time expenses.

Before you retire at 55, estimate your annual spending, healthcare costs, taxes, and income sources. A simple early retirement target calculator should include:

- Current savings

- Annual spending

- Expected investment return

- Inflation

- Healthcare cost before Medicare

- Social Security start age

- Pension or rental income

- Taxable brokerage account balance

- 401(k), IRA, and Roth balances

This matters because early retirement at 55 isn’t only about your account balance. It’s about cash flow. A person with $2 million and $150,000 in annual spending may be less secure than someone with $1.5 million and $60,000 in annual spending.

How Much Money Do I Need? $1.5M to $5M Scenarios

So, how much money do I need to retire at 55? A common shortcut is to multiply annual expenses by 25, based on the 4% withdrawal rate. But retiring at 55 may require a more conservative withdrawal rate, such as 3.5%, because your money may need to last longer.

Here is a simple example:

- A $1.5 million portfolio may support about $60,000 per year at 4%, or $52,500 at 3.5%.

- A $2 million portfolio may support about $80,000 per year at 4%, or $70,000 at 3.5%.

- A $3 million portfolio may support about $120,000 per year at 4%, or $105,000 at 3.5%.

- A $5 million portfolio may support about $200,000 per year at 4%, or $175,000 at 3.5%.

These numbers aren’t guarantees. Taxes, market returns, inflation, healthcare, and housing costs can change the outcome. Your expenses matter more than your headline portfolio balance. If your lifestyle costs $50,000 a year, retirement at age 55 may be realistic with a smaller nest egg. If your lifestyle costs $180,000 a year, even a large portfolio needs careful stress testing.

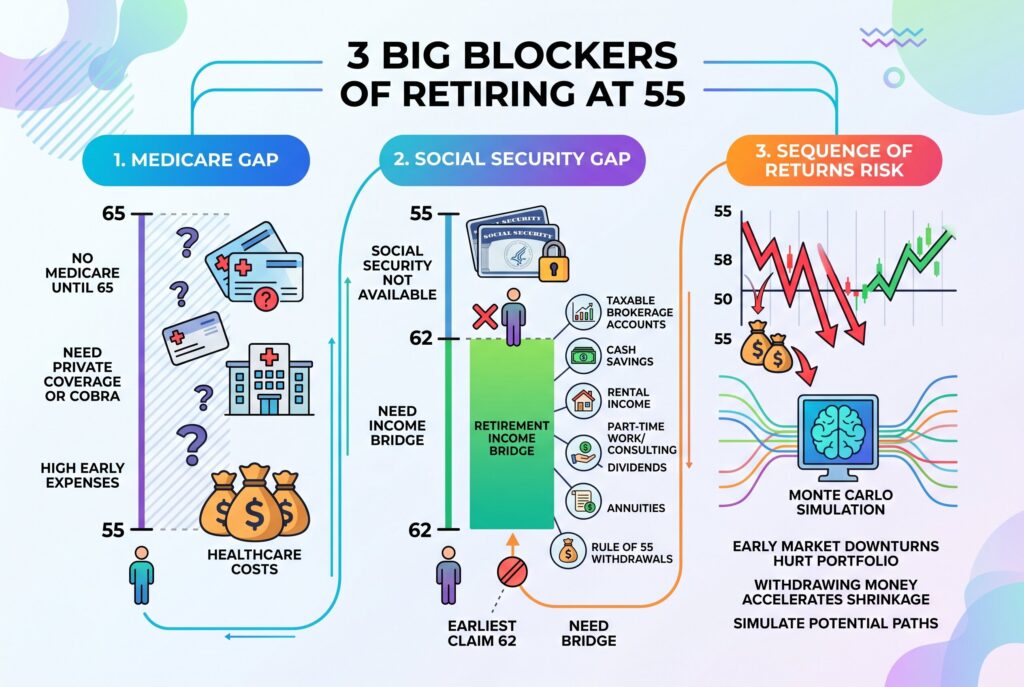

The 3 Big Blockers of Retiring at 55

- The first blocker is the Medicare gap. Medicare generally doesn’t begin until 65, so you may need 10 years of private health insurance, marketplace coverage, COBRA, retiree health benefits, or coverage through a spouse. Retirement healthcare costs can become one of your largest early-retirement expenses.

- The second blocker is the Social Security gap. Social Security at 55 isn’t available. The earliest most people can claim is age 62, and claiming early usually means a reduced benefit. You need a retirement income bridge to cover the years before Social Security begins. Bridge income may come from taxable brokerage accounts, cash savings,rental income, part-time work, consulting, dividends, annuities, or rule of 55 withdrawals.

- The third blocker is sequence of returns risk. If the stock market falls during your first few retirement years while you are withdrawing money, your portfolio may shrink faster than expected. This is why Monte Carlo retirement simulation can be more useful than assuming a straight average return every year.

Rule of 55 vs. Other Early Withdrawals

The rule of 55 isn’t the same as every other 401(k) withdrawal option. For can I cancel my 401(k) and cash out while still employed, the answer is usually no for a full cash-out while still employed, unless your plan allows certain in-service withdrawals, loans, or special exceptions.

A hardship withdrawal from 401(k) is different. It may allow access to funds for specific urgent needs, such as certain medical expenses, avoiding eviction, funeral costs, tuition, or home-related hardship. But hardship withdrawals can create taxes, reduce retirement savings, and may still have strict plan rules. A 401(k) loan is another option, but it isn’t the same as retirement income. You must repay it, and if you leave your job, the unpaid balance may become taxable. An IRA early withdrawal also has separate rules. IRAs usually don’t qualify for the 401(k) rule of 55, although other exceptions may apply.

Should You Retire at 55 or Wait?

Retiring at 55 gives you time while you are still young enough to enjoy it. You may travel, spend time with family, start a small business, volunteer, or leave a stressful career. But waiting even a few years can improve your plan. You may earn more during peak income years, add catch-up contributions, reduce debt, delay withdrawals, and shorten the healthcare bridge. The right answer depends on whether your retirement plan survives bad markets, high inflation, medical costs, and longer life expectancy. Early retirement should feel flexible, not fragile.

Conclusion

So, you can retire at 55 if your spending is controlled, your healthcare bridge is funded, and your withdrawal strategy is built around real rules instead of hope. The rule of 55 can make early retirement at 55 easier, but it isn’t a complete plan by itself. You still need to understand taxes, insurance, inflation, Social Security timing, and investment risk. Before you retire at 55, review every account, estimate every major expense, and test your plan under bad-market scenarios. Freedom at 55 is possible, but the safest version is designed carefully before you hand in your resignation.