")

Most parents spend years thinking about how to help their children build a strong financial future, whether that means paying for college, helping with a first home, or providing a better start in life. Yet one powerful wealth building tool is often overlooked: a brokerage account for kids.

Many families assume investing for children is complicated or requires a large amount of money. In reality, a child’s greatest investing advantage is time. Starting early gives investments decades to benefit from compound growth, allowing even modest contributions to potentially grow into meaningful wealth over time. As a result, more parents are exploring brokerage accounts and other investment options that can help children develop healthy financial habits while building long term wealth.

Guardian vs. Custodial: Understanding the Legal Framework

Understanding Ownership in Kids’ Investment Accounts

Before comparing providers or investment options, it’s important to understand who actually owns the money. This is where many parents become confused. Not every brokerage account for kids works the same way, and the ownership structure can affect taxes, financial aid eligibility, and future control of the assets.

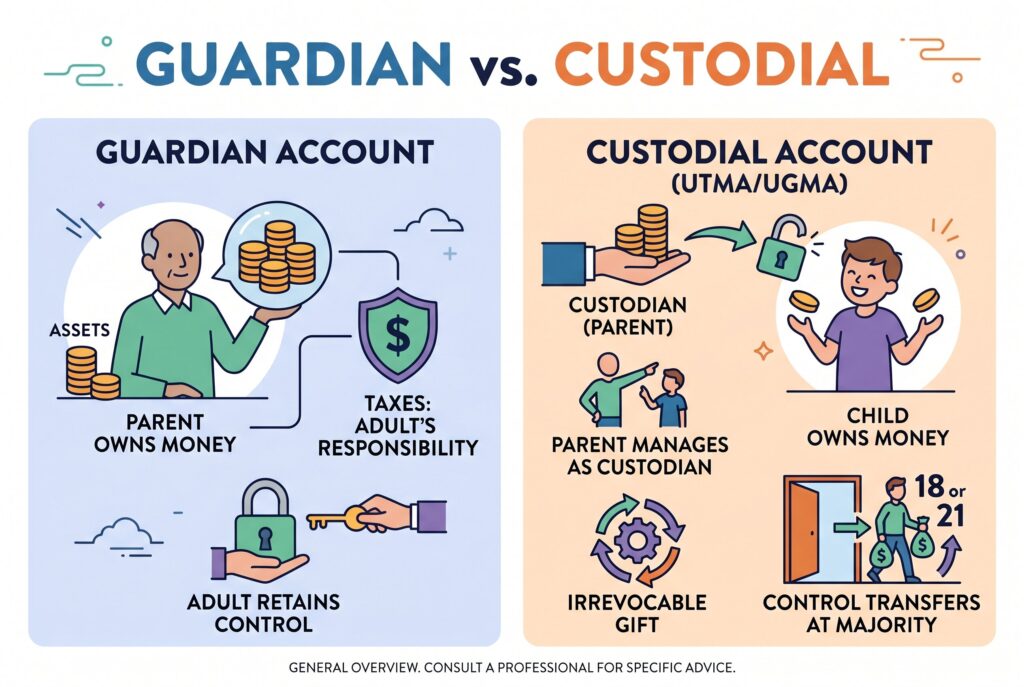

How Guardian Accounts Work

A guardian account keeps ownership with the parent or guardian. The money belongs to the adult, and any tax obligations generally remain with the adult as well.

What Makes a Custodial Account Different?

A custodial account works differently. When money is deposited into a UTMA or UGMA account, those assets legally belong to the child. The parent acts as custodian and manages the account, but ownership transfers immediately when the contribution is made.

Why Custodial Contributions Are Irrevocable

This is a crucial distinction because custodial contributions are considered irrevocable gifts. Once the money enters the account, it can’t simply be taken back because circumstances change.

What Happens When the Child Takes Control of the Account?

Many parents love the flexibility and simplicity of custodial accounts, but they sometimes overlook what happens later. When the child reaches the age of majority, control of the account transfers entirely to them. At that point, the young adult can use the money however they choose. That reality makes it important to think carefully about both the amount you contribute and the financial education you’re providing along the way.

Choosing the Best Investment Account for Kids

The best investment account for kids depends entirely on what you’re trying to accomplish. Some families want to fund education. Others want flexibility. Some want to teach investing habits. Others are focused on long-term tax advantages. Let’s break down the most common options.

UTMA vs 529: Which One Fits Your Goal?

The debate around UTMA vs 529 comes down to flexibility versus tax advantages. A 529 plan is designed for education savings, offering tax-deferred growth and tax-free withdrawals for qualified education expenses. Recent rule changes also allow certain unused funds to be rolled into a Roth IRA under specific conditions.

A UTMA account provides greater flexibility, allowing funds to be used for almost any purpose that benefits the child. However, earnings may be subject to Kiddie Tax rules, and UTMA assets can have a larger impact on financial aid eligibility.

For families focused on education savings, a 529 plan is often the better choice. For those who prioritize flexibility, a UTMA account may be more suitable. The right option depends on your family’s goals and priorities.

Roth IRA for Child: The Hidden Wealth-Building Machine

If your child earns income, there may be an even more powerful option. A Roth IRA for child can become one of the most effective wealth-building tools available. The requirement is straightforward. The child must have legitimate earned income. That could come from part-time employment, babysitting, tutoring, lifeguarding, lawn care, or other documented work activities.

Because contributions are made using after-tax dollars, all future growth can potentially be withdrawn tax-free during retirement if qualification rules are met. Think about what that means. A teenager who contributes a few thousand dollars annually may give those dollars fifty years or more to compound. Few financial strategies offer that kind of long-term advantage. For families whose children have earned income, an IRA for kids deserves serious consideration alongside traditional custodial accounts.

The Rise of Teen Brokerage Accounts

The investing landscape has changed dramatically over the last few years. Historically, investing for minors meant custodial accounts controlled almost entirely by parents. Today, several providers have introduced teen-focused investing accounts designed specifically for young investors. These accounts typically allow teenagers between 13 and 17 to participate more actively in investment decisions while parents maintain oversight and monitoring tools.

The appeal is obvious. Teenagers gain hands-on experience managing real money. Parents maintain visibility into transactions and can establish guardrails around risky behavior. Supporters see these accounts as a natural bridge between financial education and practical investing experience. Critics point out that teenagers can be heavily influenced by social media trends, speculative investments, and short-term thinking. Both perspectives have merit. A teen brokerage account can be a powerful educational tool, but only when investing education remains the primary focus.

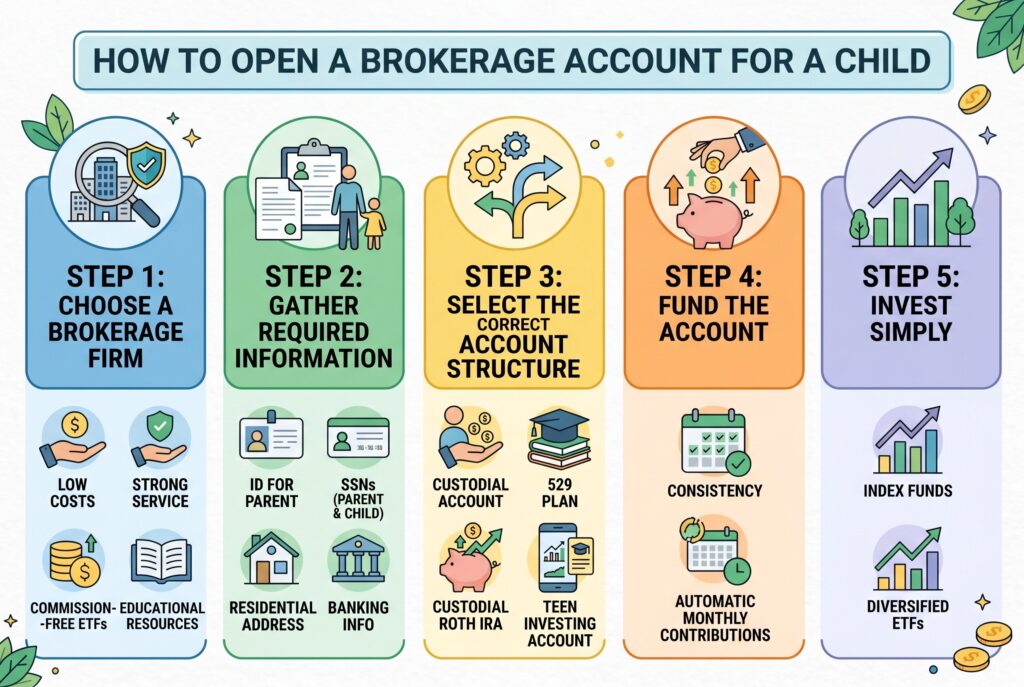

Step-by-Step: How to Open a Brokerage Account for a Child

Once you’ve selected the account type, opening the account is usually straightforward.

Step 1: Choose a Brokerage Firm

Start by looking for brokerages that offer custodial accounts with low costs, strong customer service, commission-free ETF trading, and educational resources. Fees matter more than many parents realize. A small monthly fee may seem insignificant, but over time it can meaningfully reduce returns, especially when account balances are still relatively small.

Step 2: Gather Required Information

Most providers will ask for:

- Parent or guardian identification

- Social Security Number for the parent

- Social Security Number for the child

- Residential address

- Banking information for funding

Having everything ready before you begin can reduce the setup process to just a few minutes.

Step 3: Select the Correct Account Structure

This is the most important decision.

- Choose a custodial brokerage account if flexibility is your priority.

- Choose a 529 plan if education funding is your primary goal.

- Choose a custodial Roth IRA if your child has earned income.

- Choose a teen investing account if hands-on financial education is a major objective.

Step 4: Fund the Account

Many parents make a large initial contribution and then forget about the account. A better approach is consistency. Automatic monthly contributions help build investing discipline while taking emotion out of the process. Even small recurring deposits can grow substantially over long periods of time.

Step 5: Invest Simply

One of the most common mistakes new investors make is trying to find the next winning stock. For most children, broad-market index funds and diversified ETFs offer a more practical starting point. They provide diversification, low costs, and exposure to long-term market growth without requiring constant monitoring.

Investing for Kids Is About More Than Money

Many articles focus entirely on account mechanics. That’s important, but it isn’t the whole story. The real opportunity comes from using investing as a teaching tool. Children who learn about delayed gratification, risk management, diversification, and compound growth gain skills that extend far beyond their investment account.

A monthly family investing discussion can be surprisingly effective. Review performance together. Discuss market ups and downs. Explain why long-term investing differs from speculation. Help children understand that investing isn’t about getting rich quickly. It’s about patience, consistency, and thoughtful decision-making. These lessons often become more valuable than the account balance itself.

Conclusion

Learning how to open a brokerage account for a child isn’t really about paperwork, forms, or choosing a brokerage platform. It’s about creating opportunities. Whether you choose a custodial brokerage account, compare UTMA vs 529 options, open a Roth IRA for child, or explore newer teen investing accounts, the most important step is getting started.

Time is the single asset you can never recover. Every year you wait is one less year of compound growth. More importantly, every year you wait is one less year to teach the habits that often matter more than the money itself. The most successful families don’t simply pass down assets. They pass down knowledge, discipline, and financial confidence. A brokerage account for kids can help build wealth. The conversations that happen around it can help build something even more valuable.