If you’re deciding between a UTMA vs 529 for your child’s first $1,000, the choice comes down to one question: What is this money meant to do?

What’s a 529 Plan?

A 529 plan is usually the better option when college or education is the primary goal. It offers powerful tax advantages, receives more favorable FAFSA treatment, and allows parents to keep control of the account.

What’s a UTMA Account?

UTMA Account (Uniform Transfers to Minors Act Account) is a custodial account established by an adult on behalf of a minor. The assets held in the account legally belong to the child, while a designated custodian manages and oversees the account until the child reaches the age of majority as defined by state law.

A UTMA account offers far greater flexibility, allowing the money to be used for almost anything that benefits the child, but ownership eventually transfers to the child once they reach the age of majority. Neither account is universally better. The right choice depends on whether you value tax efficiency, financial aid optimization, and control, or whether you prioritize flexibility and broader financial opportunities.

529 vs UTMA Taxes: The Battle of Tax Efficiency

The Tax Advantages That Make 529 Plans So Powerful

When families compare 529 vs UTMA taxes, they’re really comparing two completely different philosophies of wealth building. A 529 college savings plan was specifically designed to encourage education savings. Because lawmakers wanted to incentivize families to save for future educational costs, the account receives significant tax benefits. Investments inside the account grow without generating annual federal taxes, and withdrawals remain tax-free when used for qualified education expenses. Tuition, required fees, books, supplies, certain room-and-board expenses, and various educational programs may all qualify.

How Tax-Free Compounding Creates Long-Term Growth

The value of those tax benefits becomes more apparent when viewed through the lens of time. A child’s first $1,000 may remain invested for fifteen or even eighteen years before it’s needed. During that period, compound growth becomes the most powerful force in the account. Every dollar that remains sheltered from taxes continues working for the child instead of being siphoned away year after year. While the difference may seem small initially, decades of uninterrupted compounding can create a meaningful gap between two otherwise identical investments.

Why 529 Plans Are More Flexible Than Many Parents Think

Many parents hesitate because they’re worried their child might not attend college. That concern used to be one of the strongest arguments against a 529. Today, however, that objection isn’t nearly as powerful as it once was. Recent rule changes have introduced additional flexibility, including the ability to roll certain unused 529 assets into a Roth IRA for the beneficiary, subject to eligibility requirements and lifetime limits. While the account still isn’t as flexible as a custodial account, it isn’t the one-way street many people assume.

The Hidden Tax Costs of UTMA Accounts

The flexibility is attractive, but it comes with a cost. Unlike a 529, a UTMA doesn’t provide a protective tax shelter around investment growth. Interest income, dividends, and capital gains may create tax liabilities along the way. Families must also consider the Kiddie Tax rules, which were specifically created to prevent wealthy households from shifting large amounts of investment income into a child’s lower tax bracket. Depending on the amount of income generated, part of the earnings may eventually be taxed at rates tied to the parents’ income level.

Why Tax Drag Can Reduce Long-Term Wealth

For high-income families, this detail matters. A UTMA may offer broader flexibility, but flexibility alone doesn’t create wealth. Over long periods, tax drag can quietly erode returns and reduce the amount ultimately available to the child.

529 vs UTMA Financial Aid: The FAFSA Impact

How 529 and UTMA Accounts Affect Financial Aid Eligibility

The discussion around 529 vs UTMA financial aid is often overlooked until a child reaches high school. By then, changing course isn’t always easy. One of the most important factors in financial aid calculations is account ownership. FAFSA doesn’t treat all assets equally, and understanding this distinction can have a significant impact on future aid eligibility.

Why Parent-Owned 529 Plans Receive Favorable FAFSA Treatment

A parent-owned 529 is generally treated as a parent asset. Under FAFSA formulas, parent assets receive relatively favorable treatment compared to assets owned directly by the student. As a result, families often preserve more aid eligibility when college savings are held inside a 529 plan.

Why UTMA Accounts Can Have a Greater Impact on Financial Aid

A UTMA works differently because the money legally belongs to the child. Even though a parent acts as custodian during the child’s early years, the account is still classified as a child asset. FAFSA generally assesses student-owned assets more aggressively than parent-owned assets when determining how much a family can contribute toward educational expenses.

Comparing Financial Aid Outcomes: 529 vs UTMA

The practical implication is simple: two families with identical balances may receive different financial aid outcomes depending on where those assets are held. A UTMA doesn’t automatically eliminate aid opportunities, but it can reduce eligibility more quickly than a comparable 529 balance.

Balancing Flexibility and Financial Aid Considerations

This doesn’t mean a custodial account is a poor choice. It simply means families should understand the tradeoff. Greater flexibility today can sometimes create less favorable aid treatment tomorrow.

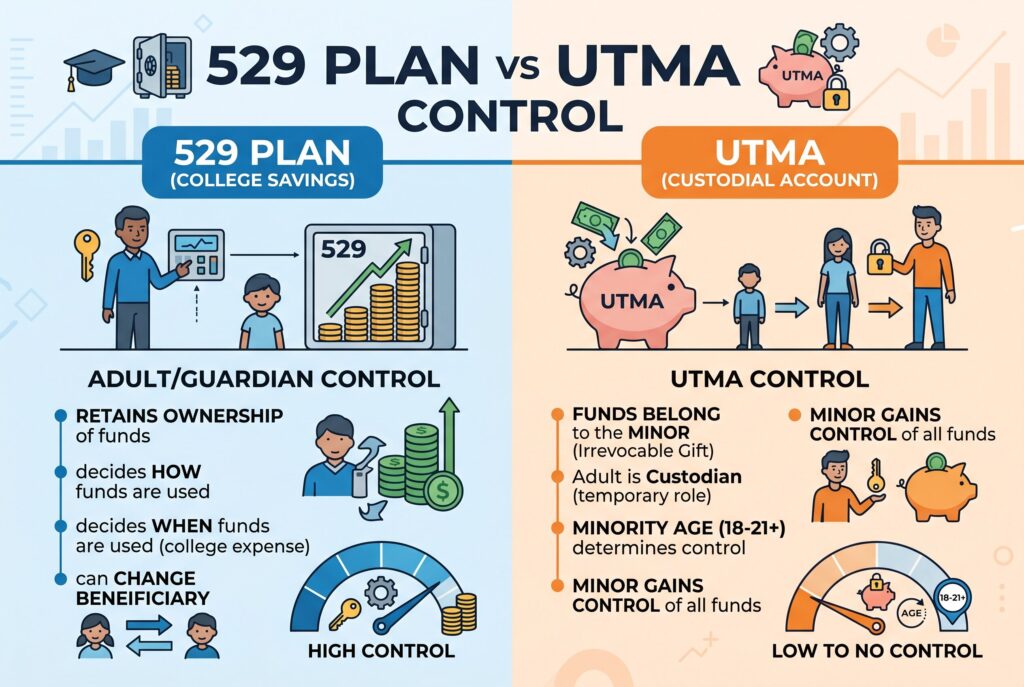

529 vs UTMA Control: Who Holds the Keys at 18?

Who Controls the Money in a 529 Plan vs UTMA Account?

The 529 vs UTMA control question often becomes the deciding factor for parents.

Why 529 Plans Give Parents Greater Long-Term Control

With a 529 plan, the account owner maintains authority over the assets. The child serves as the beneficiary, but ownership remains with the parent or grandparent who established the account. Even after the child reaches adulthood, they can’t independently access the funds. The account owner decides when distributions occur and how the money is used. If circumstances change, the beneficiary can often be changed to another eligible family member.

The Value of Flexibility When Family Plans Change

That level of control provides reassurance because life rarely unfolds exactly as planned. A child who dreams of becoming a physician at age ten may decide to launch a startup at age twenty. Another child may choose a trade school, apprenticeship, or military path instead of a traditional university. Family finances can also change dramatically over two decades. Maintaining ownership allows parents to adapt their strategy as circumstances evolve.

How UTMA Accounts Transfer Ownership to the Child

A UTMA follows a fundamentally different philosophy. Contributions are irrevocable gifts. Once assets enter the account, they belong to the child. While the custodian manages those assets during childhood, ownership eventually transfers to the beneficiary once the age of majority is reached, typically 18 or 21 depending on state law.

What Happens When the Child Reaches the Age of Majority?

At that point, parental preferences no longer control the outcome. The beneficiary may choose to spend the money on education, but they don’t have to. They could use it for travel, housing, investing, entrepreneurship, or purchases that parents might strongly disagree with. Legally, the decision belongs to them.

Choosing Between Independence and Oversight

This is the emotional heart of the custodial account vs 529 decision. Some parents value independence and responsibility enough to accept that risk. Others prefer maintaining oversight until the money fulfills its intended purpose.

| Criteria | 529 Plan | UTMA Account |

| Who owns the assets? | Parent/grandparent (account owner) | Child (beneficiary) |

| Who controls the account during childhood? | Account owner | Custodian |

| Control after child reaches adulthood | Parent retains control | Child gains full control |

| Can child access funds independently at adulthood? | No | Yes |

| Can beneficiary be changed? | Usually yes, to another eligible family member | No |

| Purpose of funds | Primarily education-related expenses | Any purpose benefiting the child |

| Flexibility for changing family circumstances | High | Low |

| Parental oversight | Maintained indefinitely | Ends at age of majority |

| Risk of child using funds differently than intended | Low | High |

| Supports child independence? | Less | More |

| Core philosophy | Parent-directed educational savings | Child-owned wealth transfer |

The Strategic Roadmap: When to Choose Each Account

For most families, the answer isn’t complicated. Choose a 529 if education remains the primary objective. It offers strong tax benefits, favorable financial aid treatment, and ongoing parental control. As a first college savings account, it’s often the most efficient place to begin. Choose a UTMA if flexibility matters more than educational specialization. Families who have already built substantial education savings, grandparents transferring wealth, or parents seeking a broader financial foundation for their children may find a custodial account more appealing.

Many households ultimately discover that the smartest solution isn’t choosing one over the other. It’s using both strategically. A family might place $800 into a 529 to establish a dedicated education fund while directing $200 into a UTMA. This hybrid approach creates a strong educational foundation while also giving the child exposure to investing and long-term wealth building. The 529 serves as the backbone of the plan, while the UTMA provides flexibility and learning opportunities.

Common Mistakes to Avoid

Before making a decision, avoid these common mistakes:

- Assuming a UTMA gift can be reversed later. Once assets are contributed, ownership transfers to the child.

- Believing a 529 only works for traditional four-year universities. Qualified education expenses extend beyond what many families realize.

- Ignoring FAFSA implications until college applications begin.

- Focusing exclusively on taxes while overlooking control and long-term family goals.

- Choosing an account based on what sounds flexible rather than what aligns with the intended purpose of the money.

Conclusion

In the UTMA vs 529 debate, the best choice depends on what you want the money to accomplish. If education is the priority, a 529 plan typically offers better tax benefits, stronger FAFSA treatment, and greater parental control. If flexibility matters more and you’re comfortable transferring ownership to your child in the future, a UTMA may be the better fit. For many families, a 529 serves as the foundation, while a UTMA can play a supporting role.