When exploring the different types of trusts, many people make the mistake of focusing on legal terminology before understanding what they actually want to achieve. At its core, a trust is a legal arrangement that allows one party to hold and manage assets for the benefit of another. They are transferred into a trust and managed by a trustee according to instructions set for the beneficiaries.

The key to choosing the right trust isn’t memorizing trust names but identifying your primary objective. In estate planning, different trusts are designed to serve different purposes. Some prioritize flexibility and control, while others help avoid probate, reduce potential tax burdens, protect assets from creditors, preserve family wealth, or provide long-term support for loved ones. Once you understand your goals, it becomes much easier to determine which type of trust may be the best fit for your situation.

The Four Foundational Pillars of Trust Law

Before choosing specialized tools, you need to understand the two core decision axes behind nearly every trust.

Axis 1: Revocable vs. Irrevocable

A revocable trust can be changed, amended, or canceled while you are alive. You usually keep control over the assets, which makes it flexible and practical for many families. The tradeoff is that because you still control the property, those assets may still count as yours for creditor claims, taxes, and eligibility rules.

An irrevocable trust is much more rigid. Once it is created and funded, you usually can’t freely change it or take the assets back. That loss of control can be uncomfortable, but it may offer stronger asset protection, estate tax planning, or long term care planning benefits when structured correctly.

Axis 2: Living vs. Testamentary

A living trust is created while you are alive. It can help manage assets during incapacity and may help your family avoid probate after death. A testamentary trust is created through your will and only comes into effect after you die. Because it depends on the will, it usually still goes through probate before the trust begins operating.

Group 1: Standard Wealth Protection

1. The Revocable Living Trust

The revocable living trust is often the most practical starting point for families that own a home, investment accounts, or property in more than one state. Its main appeal is probate avoidance. If properly funded, assets can pass to beneficiaries without the delays and public process of probate court. It is also useful for incapacity planning. If you become unable to manage your finances, a successor trustee can step in without waiting for a court appointed guardian. This trust is flexible, private, and familiar to many estate planning attorneys.

2. The Standard Family Trust

A family trust isn’t one single legal type. It is a broad phrase for a trust designed to benefit family members. Parents may use one to manage inheritance for children, protect assets for a spouse, or create rules for when beneficiaries receive money. For example, a family trust can distribute funds at certain ages or milestones, such as college graduation, marriage, or buying a first home. This helps prevent a young beneficiary from receiving a large inheritance all at once.

3. The Spendthrift Trust

A spendthrift trust protects beneficiaries from themselves and, in some cases, from outside claims. Instead of giving money outright, the trustee controls distributions according to the trust terms. This can help if a beneficiary has debt issues, addiction concerns, unstable relationships, poor money habits, or exposure to divorce. It isn’t about punishment. It is about preserving wealth so support lasts longer.

Group 2: High Net Worth Tax Planning

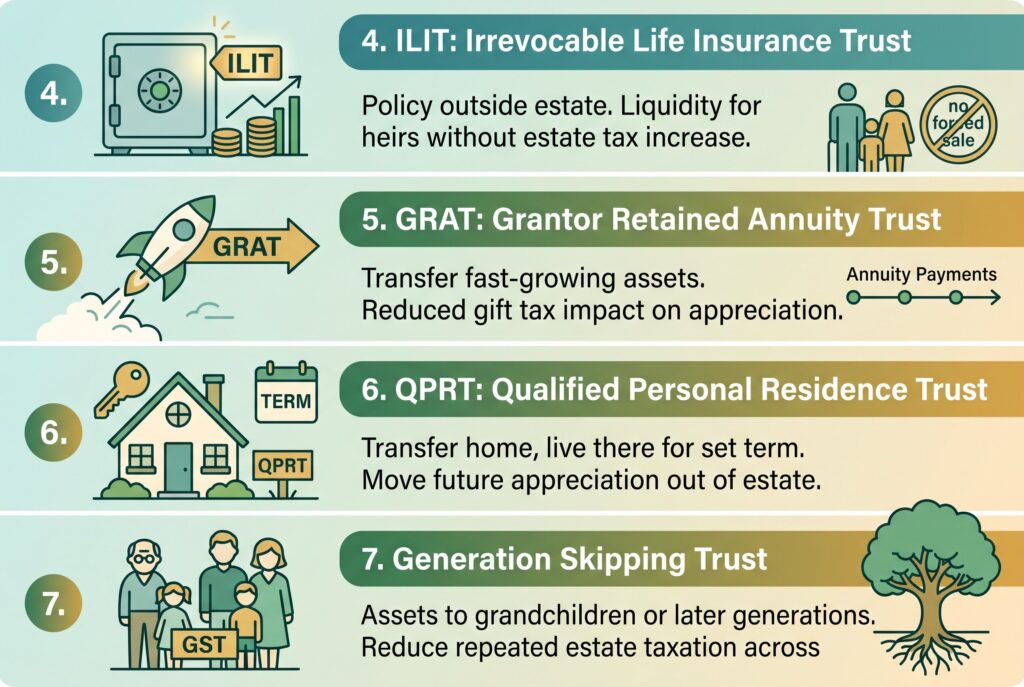

4. ILIT

An irrevocable life insurance trust, often called an ILIT, owns a life insurance policy outside your taxable estate when properly structured. This can help provide liquidity for heirs without increasing estate tax exposure. For wealthy families, this matters because estate settlement can create large tax bills. An ILIT may provide cash to pay those obligations without forcing heirs to sell a business, real estate, or family property.

5. GRAT

A grantor retained annuity trust, or GRAT, is often used to transfer fast growing assets to the next generation. The grantor receives annuity payments for a set period, and future appreciation may pass to beneficiaries with reduced gift tax impact. This strategy is complex, but it can be powerful when assets are expected to rise significantly in value.

6. QPRT

A qualified personal residence trust, or QPRT, lets you transfer a home to beneficiaries while retaining the right to live there for a set term. The goal is to move future appreciation out of your estate. This can be useful for vacation homes or valuable residences, but it requires careful planning because you must survive the trust term for the strategy to fully work.

7. Generation Skipping Trust

A generation skipping trust transfers assets to grandchildren or later generations while reducing repeated estate taxation across generations. It is often used by families with substantial wealth who want to preserve assets beyond children and into a longer family legacy.

Group 3: Special Purpose and Legacy Trusts

8. Special Needs Trust

A special needs trust supports a beneficiary with disabilities without directly giving them assets that could disrupt benefits such as Medicaid or SSI. The trust can pay for supplemental needs, including education, transportation, therapy, equipment, and quality of life expenses. This trust must be drafted carefully because benefit rules are strict.

9. Charitable Remainder Trust

A charitable remainder trust allows you to transfer assets into a trust, receive income for life or a set term, and eventually leave the remainder to charity. It may offer income tax benefits and can be useful for highly appreciated assets. This structure works best when charitable giving is a real goal, not just a tax tactic.

10. Domestic Asset Protection Trust

A domestic asset protection trust is designed to shield assets from certain future creditors while allowing limited benefit to the grantor. It is usually considered by physicians, business owners, real estate investors, and professionals with lawsuit exposure. Rules vary by state, so attorney guidance is essential.

The Blueprint: How to Set Up a Trust Without Pitfalls

Step 1: Define Your Financial Thresholds

Start by listing your assets, debts, family needs, and risk concerns. A simple probate avoidance goal may only require a revocable living trust. Tax minimization, creditor protection, disability planning, or business succession may require a more advanced trust.

Step 2: Select a Fiduciary Trustee

The trustee must manage assets responsibly and follow the trust document. You can choose a trusted family member, a professional trustee, or a corporate trustee. Family members may understand your wishes, but professional trustees may reduce conflict and improve administration.

Step 3: Formalize the Drafting

Online forms may work for very simple situations, but they can be risky for blended families, business owners, high value estates, disabled beneficiaries, real estate in multiple states, or tax planning. A trust is only as strong as its drafting.

Step 4: Follow the Funding Protocol

Funding is the make or break step. An unfunded trust is just paperwork. You must retitle real estate, update taxable accounts, assign certain assets, and coordinate beneficiary designations. Retirement accounts require special care because incorrect transfers can create tax problems.

Conclusion

Choosing among the types of trusts isn’t about collecting legal terms. It is about matching the structure to the problem you want to solve. If you want flexibility and probate avoidance, a revocable living trust may be enough. If you want asset protection, tax planning, or long term legacy control, an irrevocable or specialized trust may be more appropriate. The right trust should protect wealth, reduce confusion, and make life easier for the people you love.