vs. 403(b): 2026 Mandatory vs. Voluntary Rules")

If you work for a public school, university, hospital, nonprofit, or government agency, your retirement benefits package can feel like alphabet soup. You may see a 401(a) plan, a 403(b) plan, a pension, or even a 457(b) plan listed together.

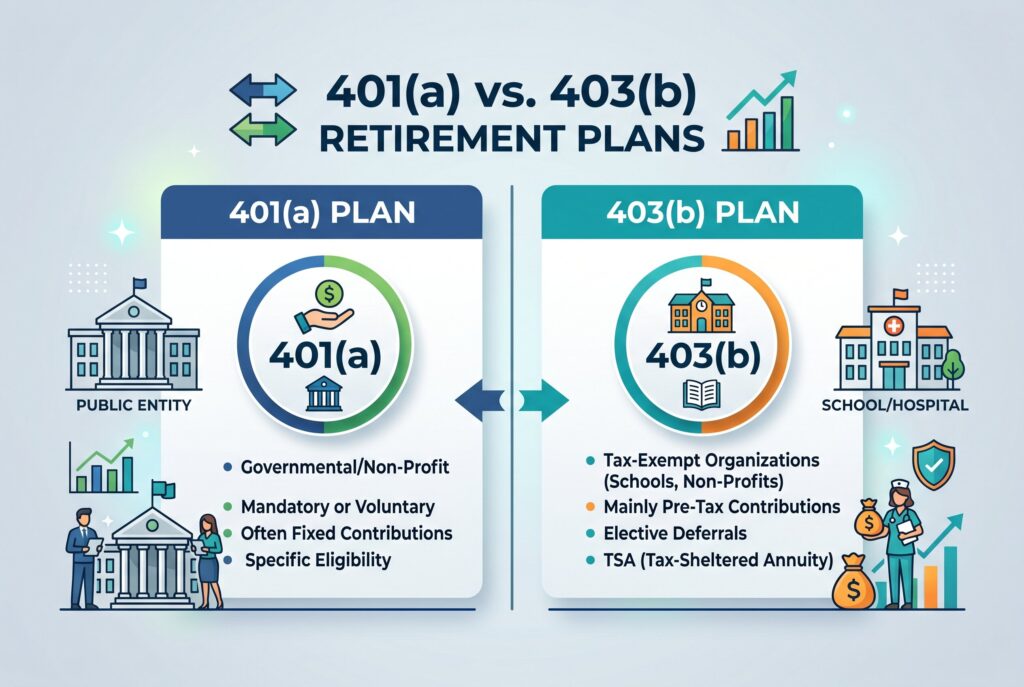

The most confusing pair is often 401(a) vs 403(b) because both can appear in the same workplace. But they aren’t used the same way. The main difference between 401(a) vs 403(b) is control. A 401(a) is usually employer-driven, and contributions may be mandatory or employer-funded. A 403(b) is usually employee-driven, meaning you voluntarily decide how much salary to contribute. Many public-sector and nonprofit workers are offered both plans at the same time.

The Core Difference: Employer Control vs. Employee Flexibility

A 401(a) is highly customizable by the employer. Your employer may decide who participates, how much must be contributed, whether participation is mandatory, and when employer money becomes vested. Some 401(a) plans are funded only by the employer. Others require a fixed employee contribution, such as 5%, 6%, or 8% of salary.

A 403(b) plan is more flexible for employees. It works more like a private-sector 401(k). You choose whether to participate, how much to defer, and whether to use traditional pre-tax or Roth 403(b) contributions if your plan allows it. That is the practical difference: the 401(a) often builds your retirement base automatically, while the 403(b) lets you control your extra savings.

2026 Contribution Limits: 401(a) vs. 403(b)

For 2026, the total defined contribution limit is $72,000. This is the limit that generally matters for combined employer and employee contributions in a 401(a) plan. For 403(b) plans, the employee elective deferral limit is $24,500 in 2026. The standard catch-up contribution for age 50 and older is $8,000, allowing many older workers to contribute up to $32,500. There is also a special age 60 to 63 catch-up limit of $11,250 for eligible participants in 2026. Some long-term 403(b) employees may also qualify for the 15-year catch-up rule, which can allow an extra $3,000 per year, subject to strict lifetime and plan limits.

Plan Stacking: Which Should You Fund First?

If your employer offers both a 401(a) and a 403(b), think in layers.

- First, handle the 401(a). If contributions are mandatory, you likely don’t have a choice. Treat that deduction as your baseline retirement savings.

- Second, capture any employer match. Sometimes employer money is housed in the 401(a). Sometimes a 403(b) match may be available. Either way, don’t ignore matching money if you can afford to contribute.

- Third, use the 403(b) for extra voluntary savings. This is usually where you have more control over your contribution percentage, tax treatment, and sometimes investment provider.

Beware the 403(b) Annuity Trap

A 403(b) can be a powerful plan, but some older or poorly designed 403(b) menus include high-fee annuity contracts. These may have surrender charges, complicated guarantees, and higher expenses than low-cost mutual funds or index funds.

Before increasing contributions, review the investment menu carefully. Look for expense ratios, administrative fees, surrender periods, and whether low-cost target-date funds or index funds are available. A good 403(b) can be excellent. A high-fee 403(b) can quietly weaken your long-term returns.

Leaving Your Job: Vesting and Rollover Rules

Your voluntary 403(b) contributions are generally 100% yours immediately. Employer contributions may follow a vesting schedule. A 401(a) often has stricter vesting rules for employer money. For example, you might need to stay three to five years to keep all employer contributions. If you leave early, you may forfeit the unvested portion. When you leave your job, both 401(a) and 403(b) balances can often be rolled over into a traditional IRA or a new employer’s eligible retirement plan. A direct rollover helps avoid current taxes and early withdrawal penalties.

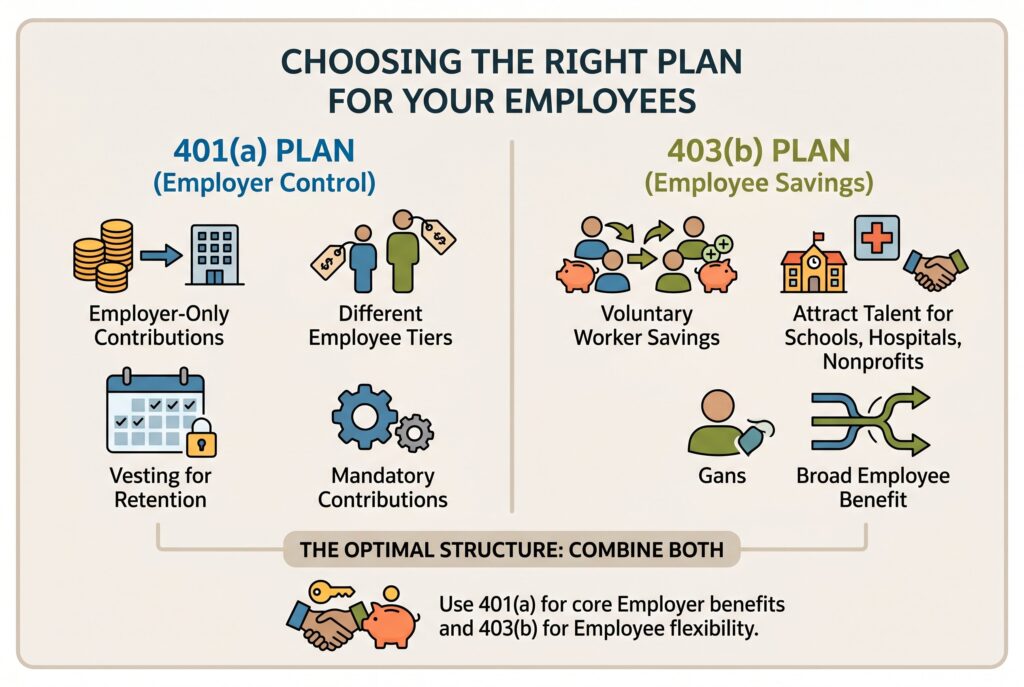

For Employers: Which Plan Should You Offer?

Employers often use 401(a) plans when they want more control. A 401(a) can support mandatory contributions, employer-only contributions, different employee tiers, and retention through vesting schedules. A 403(b) is usually better as a broad employee savings benefit. It lets workers voluntarily save more and can help schools, hospitals, and nonprofits compete for talent. For many organizations, the best structure isn’t either/or. A 401(a) can provide the core employer benefit, while a 403(b) gives employees flexibility.

Conclusion

Having access to both a 401(a) and a 403(b) can be a major wealth-building advantage. The 401(a) may force consistent savings or deliver employer contributions. The 403(b) lets you accelerate retirement savings with voluntary contributions.

The smartest strategy is to understand what each plan is doing. Use the 401(a) as your foundation, capture employer money, review 403(b) fees carefully, and then increase voluntary contributions as your budget allows. When used together, these two plans can turn a confusing benefits package into a powerful retirement system.

Related Articles

401(a) vs 401(k): 2026 Key Differences and Which Plan Is Better?