")

If you’re wondering how does an online savings account work, the simple answer is this: it works like a regular savings account, but without the branch. You deposit money, the bank pays interest, and you manage everything through a website or mobile app.

What’s an Online Savings Account?

So, what is an online savings account? It’s a deposit account offered by a digital bank or an online division of a traditional bank. A clear online savings account description would be: a secure, interest-earning account designed for money you want to save, not spend daily.

The main attraction is yield. Because online banks don’t pay for large branch networks, they can often offer higher APYs and lower fees than a traditional savings account. Your money may still be FDIC-insured up to legal limits if the institution is properly covered. But there’s a catch. Online savings accounts can be excellent for emergency funds, house down payments, and savings goals, but they aren’t always ideal for cash deposits, instant access, or people who need face-to-face banking.

The Core Mechanics: Money In, Money Out

An online savings account is built around digital movement. You usually connect it to an existing checking account, then move money through electronic transfers. Deposits often happen through ACH transfer, direct deposit, mobile check deposit, or a transfer from another bank. Some online banks also allow wire transfers, though fees may apply. If your employer lets you split your paycheck, you can send part of each paycheck directly into savings.

Can you add to balance regularly for online savings account? Yes, and this is one of the strongest features. You can schedule automatic transfers every payday, every week, or every month. This turns saving into a system instead of a decision you have to remake constantly. Withdrawals usually happen by transferring money back to checking. Some online savings accounts offer ATM access, but many don’t. Even when ATM access exists, cash withdrawal options may depend on the bank’s network.

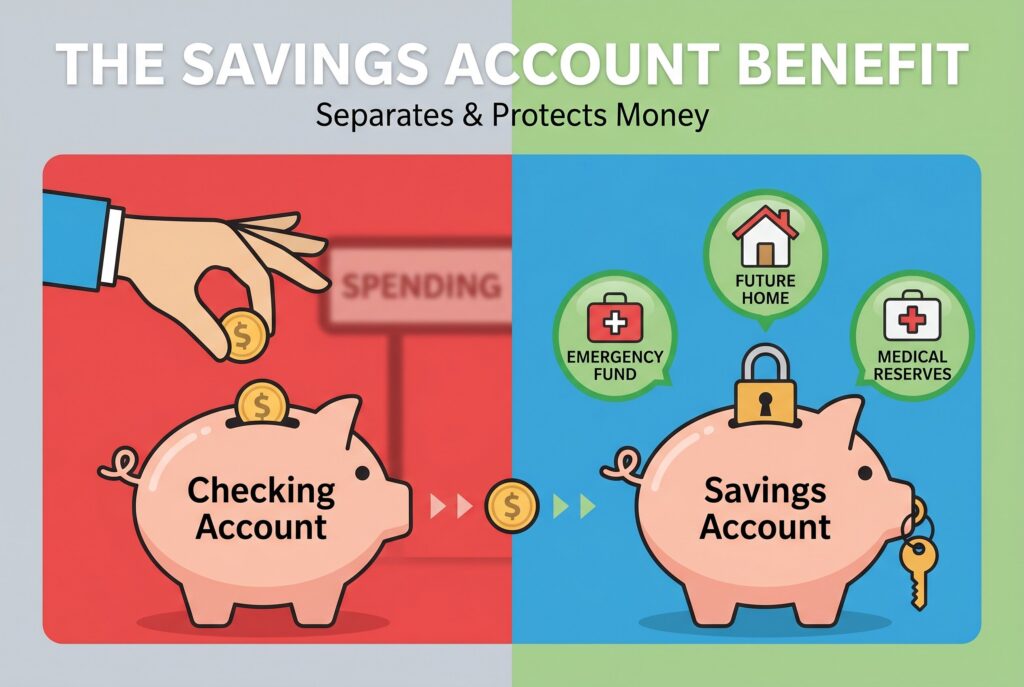

This is where online savings accounts differ from checking accounts. A checking account is built for spending, bills, debit cards, and frequent transactions. A savings account is built to hold money, earn interest, and reduce the temptation to spend.

The Catch: What Online Banks Hide From You

Online savings accounts can be useful, but they aren’t perfect. The higher APY often comes with tradeoffs.

Limited Options for Cash Deposits

Online banks work best for people who primarily move money electronically. If you regularly receive cash from tips, side gigs, or small-business sales, depositing funds can be less convenient. In many cases, you’ll need to deposit cash at a local bank first and then transfer it to your online savings account.

Transfers May Not Be Instant

Unlike money held at your primary bank, funds in an online savings account may take one to three business days to transfer through ACH. While this usually isn’t a problem for long-term savings, it can be inconvenient during a financial emergency. Many savers keep a small cash buffer in a local checking account to bridge that gap.

Interest Rates Can Change

The APY on a high-yield savings account is typically variable rather than fixed. Banks can adjust rates as market conditions and interest-rate policies change. A competitive rate today may look very different a year from now, making it important to review your account periodically.

Customer Service Quality Varies

Not all online banks offer the same level of support. Some provide excellent mobile apps, fast response times, and helpful customer service, while others may be harder to reach when issues arise. Before opening an account, review customer feedback, support options, fee schedules, and account access policies.

Balance Requirements: Do You Need to Be Rich to Start?

A typical minimum balance for online savings account is often low. Many online banks let you open an account with $0 or $1, though some require a higher opening deposit or minimum balance to earn the best APY. This is one reason online savings accounts are beginner-friendly. You don’t need thousands of dollars to start. You can open the account, automate small transfers, and let the balance grow over time.

Still, read the fine print. Some accounts advertise a high APY but require a certain balance, direct deposit, or activity requirement. Others may charge fees for wire transfers, excessive transactions, paper statements, or outgoing transfers. The best account isn’t always the one with the highest headline rate. It’s the one with a strong APY, no monthly maintenance fee, FDIC insurance, easy transfers, useful mobile tools, and rules you can actually live with.

What Is the Benefit of an Online Savings Account?

The biggest benefit of an online savings account is the ability to earn a competitive interest rate while keeping your money accessible. Unlike many traditional savings accounts, online banks often offer higher APYs because they operate with lower overhead costs and fewer physical branches. This makes online savings accounts a popular choice for emergency funds and short-term savings goals. Your money remains relatively liquid, but it can generate more interest while you wait to use it.

Online savings accounts can be particularly useful for goals such as building an emergency fund, saving for a vacation, setting aside money for taxes, planning a home repair, or accumulating a future down payment. They provide a balance between safety, accessibility, and yield that many other cash-management options struggle to match.

When Should You Use an Online Savings Account Instead of Investing?

One of the most common mistakes is using a savings account for money that should be invested, or investing money that should remain in cash. An online savings account is generally appropriate when the money may be needed within the next few months or years. Emergency funds, planned purchases, travel budgets, tax payments, and home repairs are common examples.

For goals that are a decade or more away, such as retirement, long-term wealth building, or a child’s future expenses, investment accounts may offer greater growth potential. The tradeoff is that investment values can fluctuate, while savings account balances don’t. The timeline often matters more than the interest rate. The shorter the timeline, the more useful an online savings account becomes.

Conclusion

Understanding how does an online savings account work helps you avoid leaving cash in the wrong place. The account is simple: deposit digitally, earn interest, transfer when needed, and use automation to build savings consistently. Before opening one, verify FDIC insurance through official channels. Turn on two-factor authentication. Use a strong password. Avoid public Wi-Fi when banking. Compare APY, fees, minimum balance rules, transfer speed, ATM access, and customer support.

If you handle lots of cash or need instant branch service, keep a traditional bank relationship too. If your goal is a higher yield on safe savings, an online savings account can be one of the easiest upgrades you make. The smartest setup may be hybrid: local checking for daily life, online savings for your future, and automatic transfers that move money before you have the chance to spend it.

Related Articles

Different Types of Savings Accounts: Which Pays the Most in 2026?