The phrase trust fund baby usually comes with a stereotype. People imagine a spoiled rich kid who never works, spends family money without thinking, and lives comfortably because someone else built the wealth. That image makes good movie drama, but it doesn’t explain what a trust fund actually is.

What Is a Trust Fund Baby?

So, what is a trust fund baby in real financial terms? A trust fund baby is simply a beneficiary of a trust fund. That trust may be created by parents, grandparents, or another family member to hold and manage assets for the child. The goal isn’t always luxury. In many families, the goal is protection, privacy, probate avoidance, and disciplined wealth transfer.

A trust fund for kids can hold cash, investments, real estate, business interests, or other assets. The child doesn’t always receive everything at once. In fact, the best trusts are designed to prevent that. A well written trust can release money slowly, set conditions, and protect assets until the child is mature enough to manage them.

Trust Fund Baby: Myth vs. Reality

| Common Myth | Legal Reality |

|---|---|

| Trust funds are only for wealthy families. | Trusts can benefit families of many income levels. They may be used to protect a home, manage life insurance proceeds, or preserve savings for a child. |

| A child can spend trust money whenever they want. | The trustee controls distributions based on the trust’s terms. Funds can be restricted to education, housing, healthcare, business ventures, or specific ages and milestones. |

| The child owns and controls all assets immediately. | The beneficiary may benefit from the trust assets, but the trustee retains legal control and manages distributions according to the trust agreement. |

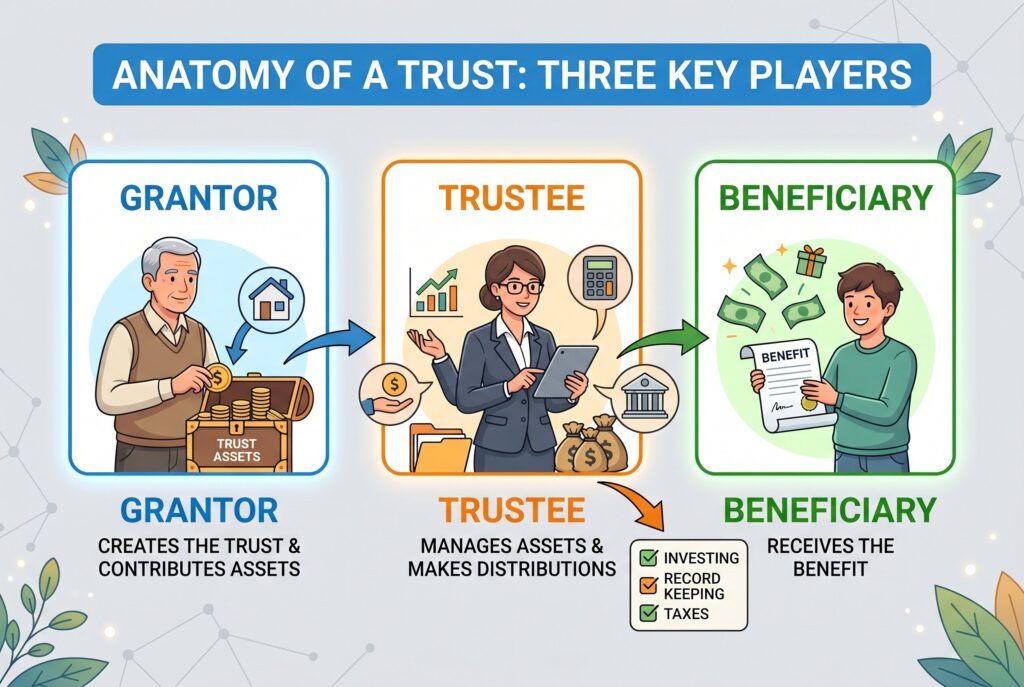

Anatomy of a Trust: The Three Key Players

Every trust has three core roles.

- The first is the grantor. This is the person who creates the trust and contributes assets. In a family plan, the grantor is often a parent or grandparent. The grantor decides the purpose of the trust and writes the rules.

- The second is the trustee. This person or institution manages the assets. The trustee may invest the money, pay bills, file tax documents, keep records, and approve distributions. A trustee can be a trusted relative, attorney, professional fiduciary, or corporate trustee.

- The third is the beneficiary. This is the person who receives the benefit. In this case, the beneficiary is the child people might casually call a trust fund baby.

The trustee role is especially important. A loving family member isn’t always the best trustee if they lack financial discipline or can’t say no. A professional trustee may cost more, but can reduce family conflict and protect the trust from emotional decision making.

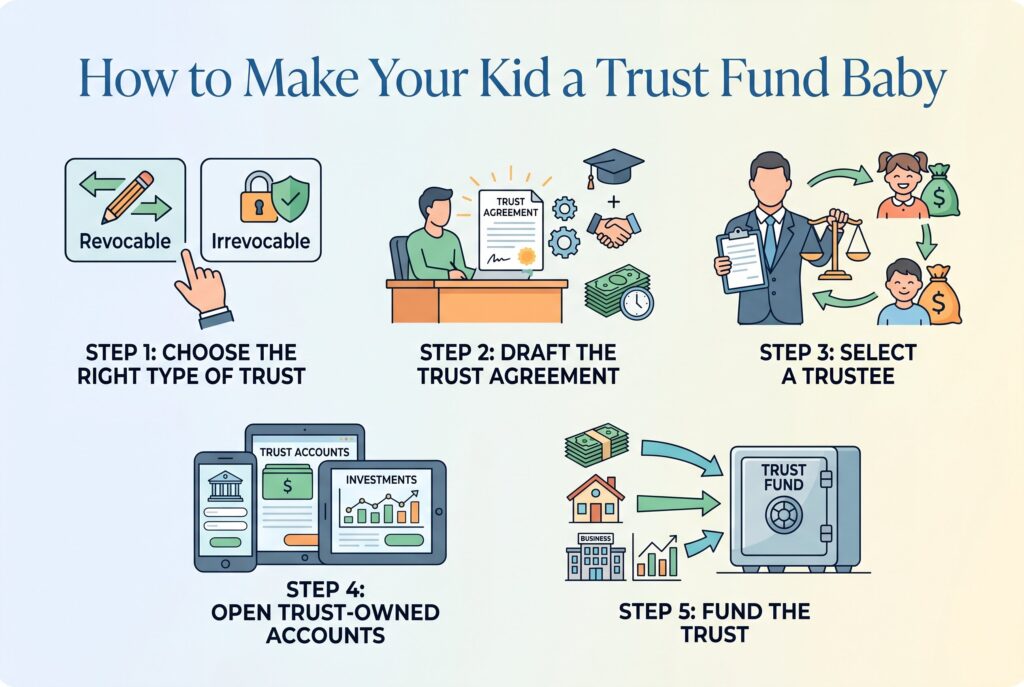

How to Make Your Kid a Trust Fund Baby

Step 1: Choose the Right Type of Trust

The first step is deciding between a revocable trust and an irrevocable trust. A revocable trust can typically be changed during the grantor’s lifetime and offers flexibility, while an irrevocable trust may provide stronger asset protection and estate planning benefits.

Step 2: Draft the Trust Agreement

The trust agreement defines who manages the trust, who benefits from it, and how assets will be distributed. Rather than granting full access at a young age, many parents establish milestones based on age, education, employment, or other achievements.

Step 3: Select a Trustee

Choosing the right trustee is one of the most important decisions in the process. The trustee should be responsible, organized, impartial, and capable of managing family wealth according to the trust’s instructions.

Step 4: Open Trust-Owned Accounts

Once the trust is established, assets must be held in the trust’s name. This may include brokerage accounts, bank accounts, or real estate that has been retitled to the trust.

Step 5: Fund the Trust

A trust only works if assets are transferred into it. Funding may involve moving cash, transferring investments, retitling property, updating beneficiary designations, or assigning business interests. This step transforms the trust from a legal document into a functioning wealth transfer and asset protection strategy.

Trust Funds vs. Other Investment Accounts for Kids

UTMA and UGMA Custodial Accounts

UTMA (Uniform Transfers to Minors Act) and UGMA (Uniform Gifts to Minors Act) accounts allow parents, grandparents, and other adults to invest on behalf of a child. These custodial accounts can hold assets such as stocks, ETFs, mutual funds, bonds, and cash.

The custodian manages the account until the child reaches the age of majority, which varies by state. Once that age is reached, full ownership and control transfer to the beneficiary. Because contributions are considered irrevocable gifts, the assets legally belong to the child from the moment they are deposited into the account.

529 College Savings Plans

A 529 plan is a tax-advantaged investment account designed to help families save for education expenses. Investments grow tax-deferred, and qualified withdrawals are generally tax-free when used for eligible education costs such as tuition, fees, books, supplies, and certain room-and-board expenses. Many states also offer additional tax incentives for residents who contribute to a 529 plan. Recent legislative updates have expanded the flexibility of these accounts, including limited opportunities to roll unused funds into a Roth IRA under specific conditions.

Trust Funds for Kids

A trust fund is a legal arrangement that allows assets to be managed on behalf of a beneficiary according to rules established by the grantor. Parents can specify how and when assets are distributed, creating customized guidelines for education, housing, healthcare, entrepreneurship, or long-term financial support. A trustee oversees the assets and ensures distributions follow the trust’s terms. Trust funds can also provide asset protection, privacy, and greater control over how wealth is transferred across generations. While trusts often involve higher setup and maintenance costs, they offer significant flexibility in estate and wealth planning.

Conclusion

The real lesson behind what a trust fund baby is isn’t about privilege. It’s about responsibility. A well-structured trust can help fund education, protect family assets, and support responsible adulthood. But money alone doesn’t create financial wisdom. Parents still need to teach budgeting, investing, work ethic, and patience.

The best trust fund doesn’t replace ambition. It supports it. If your goal is to build generational wealth, focus on more than the assets you leave behind. Create a clear plan, choose the right trustee, and establish thoughtful distribution rules. A trust should provide opportunity, not dependency.