")

Many people associate family trusts with wealthy families and complex estate plans, but that perception is often misleading. A family trust is a legal structure designed to hold and manage assets for the benefit of family members or other chosen beneficiaries.

The process works by transferring assets, such as real estate, cash, investments, or business interests – into the trust. A trustee is then responsible for managing those assets according to the instructions established by the grantor, while the beneficiaries receive the benefits outlined in the trust agreement. Beyond wealth preservation, a family trust can play an important role in estate planning by helping families avoid probate, maintain privacy, reduce the potential for disputes, and create clear rules for how assets should be managed and distributed over time.

The Reality: “Family Trust” Isn’t a Single Legal Term

A family trust isn’t one exact legal product. It’s a broad phrase used for any trust designed to benefit family members. The structure you choose matters because each type offers different levels of control, protection, flexibility, and cost.

Revocable Living Trust

A revocable living trust is the most common option for many families. You can change it, update it, cancel it, add assets, remove assets, and continue using your property while you are alive. It’s popular because it helps avoid probate while keeping control in your hands. This option is often useful for parents who own a home, have minor children, want privacy, or want their family to avoid court delays after death. The tradeoff is that a revocable trust usually doesn’t provide strong creditor protection while you are alive because you still control the assets.

Irrevocable Trust

An irrevocable trust is more rigid. Once assets are moved into it, you usually can’t take them back or freely change the terms. That loss of control is serious, but it can create stronger asset protection and may support advanced estate tax planning. This structure is usually better for families with larger estates, creditor concerns, Medicaid planning issues, or complex wealth transfer goals. It shouldn’t be created casually.

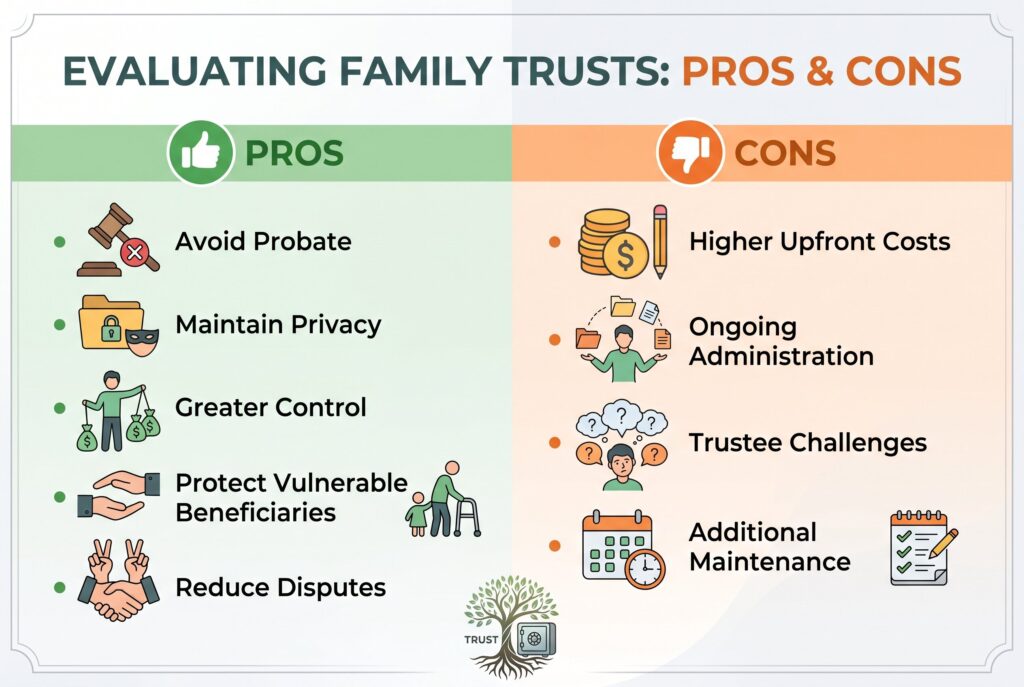

Evaluating the Pros and Cons of a Family Trust

The Pros: Protection, Privacy, and Control

- Avoiding probate: Assets held in a properly funded trust can generally pass to beneficiaries without going through probate, helping families avoid court involvement, reduce delays, and potentially lower administrative costs.

- Maintaining privacy: Unlike a will, which may become part of the public court record during probate, a trust typically remains private. This keeps information about assets, beneficiaries, and distributions out of public view.

- Providing greater control over inheritance: A trust allows you to decide when and how beneficiaries receive assets rather than distributing everything at once. For example, you may choose to release portions of an inheritance at specific ages or after certain milestones are reached.

- Protecting vulnerable beneficiaries: Trusts can include safeguards for beneficiaries who are minors, have special needs, lack financial experience, or may be vulnerable to outside influence, helping ensure assets are managed responsibly over time.

- Reducing the risk of family disputes: By clearly outlining how assets should be managed and distributed, a trust can minimize misunderstandings and conflicts among family members after the grantor’s death.

The Cons: Cost, Complexity, and Maintenance

- Higher upfront costs: Creating a trust is generally more expensive than preparing a basic will. While a simple will may cost only a few hundred dollars, an attorney-drafted trust often ranges from $1,500 to $4,000 or more, depending on the state, the complexity of the estate, and the family’s specific planning goals.

- Ongoing administrative responsibilities: Signing the trust document is only the first step. Assets must be properly transferred into the trust through a process known as funding. If key assets are not retitled in the trust’s name, they may not receive the intended benefits and could still be subject to probate.

- Trustee selection challenges: The effectiveness of a trust often depends on the person chosen to manage it. A trustee should be organized, impartial, financially responsible, and capable of following the trust’s instructions. Selecting the wrong trustee can lead to administrative delays, strained family relationships, and potential disputes among beneficiaries.

- Additional maintenance requirements: Trusts should be reviewed periodically, especially after major life events such as marriage, divorce, the birth of children, or significant changes in assets. Failing to keep the trust updated may reduce its effectiveness over time.

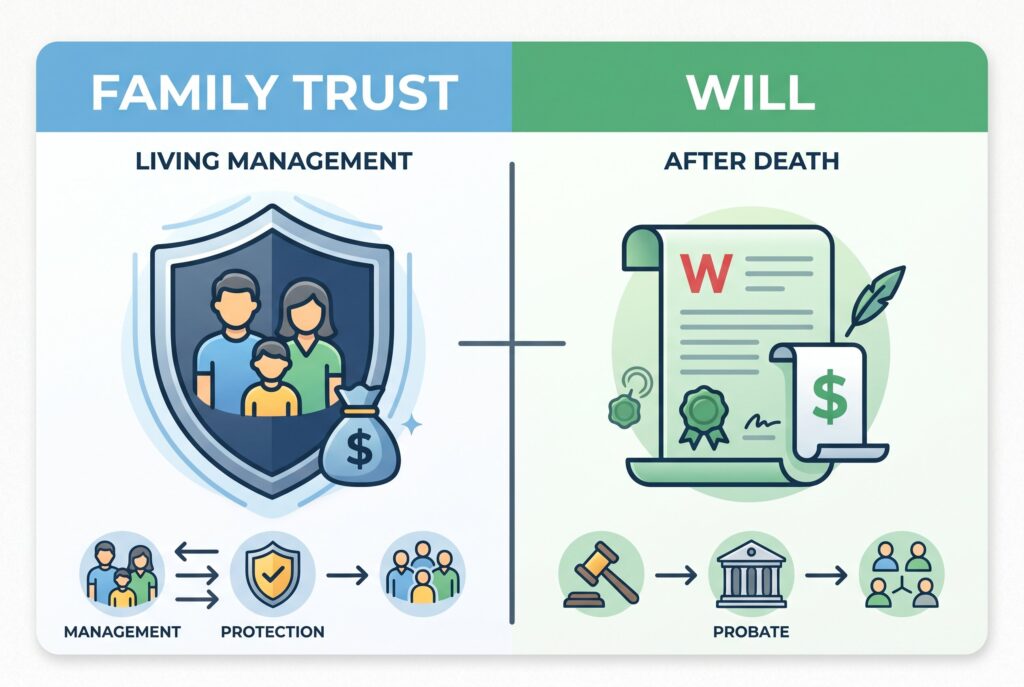

Family Trust vs Will: Which One Is Better?

A will is simpler and cheaper. It lets you name heirs, appoint guardians for minor children, and state your final wishes. For smaller estates with few assets, a will may be enough.

A family trust is usually better when privacy, probate avoidance, asset management, or staged inheritance matters. If you own real estate in more than one state, have a blended family, want to protect minor children, or want smoother administration, a trust may be worth the extra cost.

The best estate plan often uses both. The trust handles major assets, while a pour over will catch anything accidentally left outside the trust.

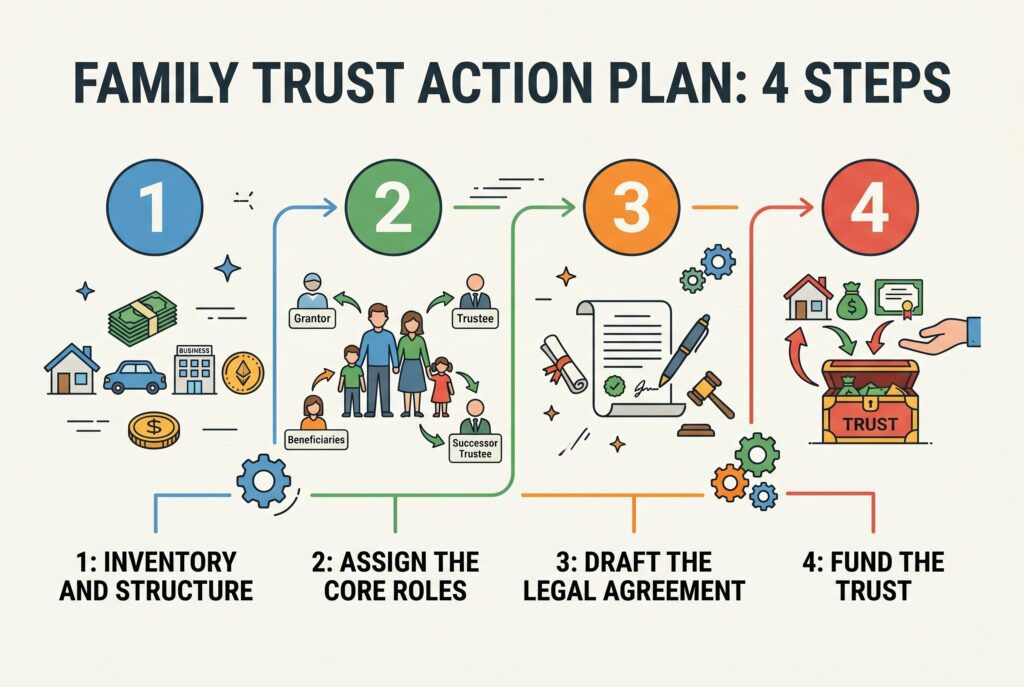

Action Plan: How to Set Up a Family Trust in 4 Steps

Step 1: Inventory and Structure

Start by listing your assets. Include your home, bank accounts, investment accounts, business interests, vehicles, collectibles, and valuable personal property. Then decide whether you need a revocable living trust or an irrevocable trust. Most families begin with a revocable structure unless they have tax, creditor, or long term care planning concerns.

Step 2: Assign the Core Roles

Every trust needs key people. The grantor creates the trust. The trustee manages it. The beneficiaries receive benefits from it. You may serve as your own trustee during life, then name a successor trustee to step in if you die or become incapacitated. Choose beneficiaries carefully and think beyond equal shares. Some families need special rules for minor children, a child with disabilities, a financially irresponsible heir, or a second marriage.

Step 3: Draft the Legal Agreement

You can use DIY software for a very simple estate, but an attorney is usually safer if you own real estate, have blended family issues, run a business, have children from different relationships, expect family conflict, or need tax planning. The trust agreement should clearly explain who manages the assets, who receives them, when distributions happen, and what powers the trustee has.

Step 4: Fund the Trust

Funding is the make or break step. A signed family trust doesn’t protect assets that were never transferred into it. You may need to retitle your home, update bank accounts, transfer taxable investment accounts, and coordinate beneficiary designations. Be careful with retirement accounts. Many families shouldn’t simply retitle retirement accounts into a trust without professional advice because tax rules can be complicated.

Conclusion

A family trust isn’t just a document. It’s a plan for transferring wealth with less confusion, more privacy, and better control. It can help your loved ones avoid probate, protect family instructions, and manage inheritance more thoughtfully than a simple will.

Still, a trust isn’t magic. It costs money, requires careful drafting, and must be funded correctly. The smartest approach is to decide what problem you are solving first: privacy, probate, minor children, blended family planning, taxes, asset protection, or long term control. Once the purpose is clear, the right trust structure becomes much easier to choose.