")

One of the easiest ways to think about testamentary trust is as a trust that sits inside your Last Will and Testament, waiting to be activated. It does not exist while you are alive. Instead, it comes into effect only after your death and after your will has gone through the probate process. Unlike a living trust, which can own and manage assets during your lifetime, a testamentary trust is created through your will and becomes operational later. This often makes it less expensive to set up initially because there is no separate trust administration during your life. However, because it must pass through probate, it can take longer to become effective and does not offer the same level of privacy as a living trust.

A testamentary trust can be particularly useful when you want to control how and when beneficiaries receive their inheritance. Many parents use it to protect assets for minor children, while others create one for a beneficiary with special needs or for someone who may not be ready to manage a large sum of money responsibly. Rather than distributing assets all at once, the trust can hold and manage them according to the instructions you leave behind.

The Mechanics: How Does It Work in Reality?

A testamentary trust definition always begins with one fact: the trust is created by your will. While you are alive, there is no separate trust account, no active trustee, and no trust administration. The instructions are waiting inside the will.

The timeline usually works like this. First, you pass away. Then your executor files the will with probate court. The court validates the will, gives authority to the executor, allows creditors to make claims, and supervises payment of debts and expenses. Only after that process is complete can the remaining assets be transferred into the testamentary trust. At that point, the trustee begins managing the money for the beneficiaries. If the trust was written for children, the trustee may pay for housing, school, healthcare, clothing, and daily needs until they reach the ages you selected.

Testamentary Trust vs Living Trust

The difference between a testamentary trust vs living trust is timing. A living trust is created and funded while you are alive. It can help avoid probate, preserve privacy, and allow a successor trustee to step in if you become incapacitated. A testamentary trust is created after death through your will. It doesn’t avoid probate because probate is the doorway that activates it. That is why a testamentary trust is often called the cheaper upfront option. It may cost less to add trust language to a will than to create and fund a full living trust. But the savings today can become delays and court costs for your family later.

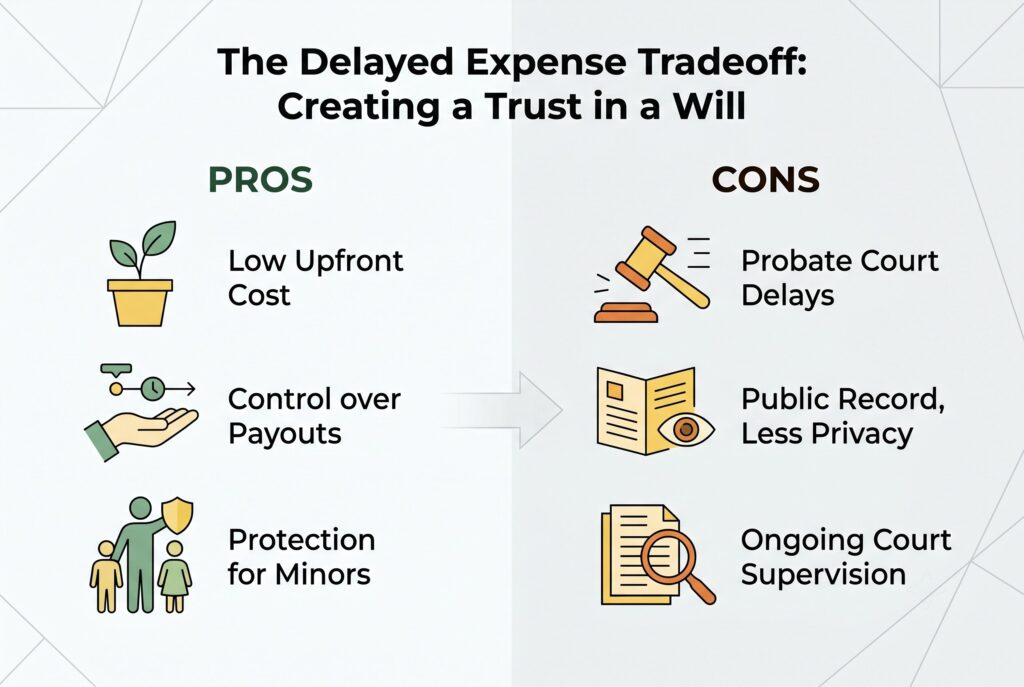

Pros and Cons: The Delayed Expense Tradeoff

The Pros

- The first advantage is low upfront cost. Creating a trust in a will is usually simpler and less expensive than building a full trust plan during life. For young families who are still growing wealth, this can be appealing.

- The second advantage is control. You can decide when and how beneficiaries receive money. Instead of giving a child a large inheritance at 18, you might allow distributions at 25, 30, and 35. You can also permit earlier payments for education, medical care, or housing.

- The third advantage is protection for dependents. A trust for minor children gives an adult trustee legal authority to manage funds until children are mature enough to handle money responsibly.

The Cons

- The biggest disadvantage is probate. Because the trust is inside the will, your estate must go through court before the trust can be funded. That can take months, sometimes longer.

- The second disadvantage is loss of privacy. A will filed in probate can become part of the public record. This may reveal family names, assets, and inheritance terms.

- The third disadvantage is ongoing court supervision. In some situations, the trustee may need to provide accountings or reports to the court, which adds time, paperwork, and expense.

The 2026 Tax Cliff Warning

A testamentary trust can be useful, but it isn’t the right tool for every estate. If you have substantial wealth, business interests, or assets near federal estate tax thresholds, you should be cautious. Estate tax rules can change, and large estates may need planning that happens while you are alive, not after death. A testamentary trust activates too late to handle many advanced tax strategies. If your estate is large enough to face estate tax exposure, you may need lifetime planning tools, irrevocable trusts, gifting strategies, or other advanced structures. This is especially important for families reviewing types of trusts in 2026. The right trust depends on asset size, timing, control, privacy, tax exposure, and beneficiary needs.

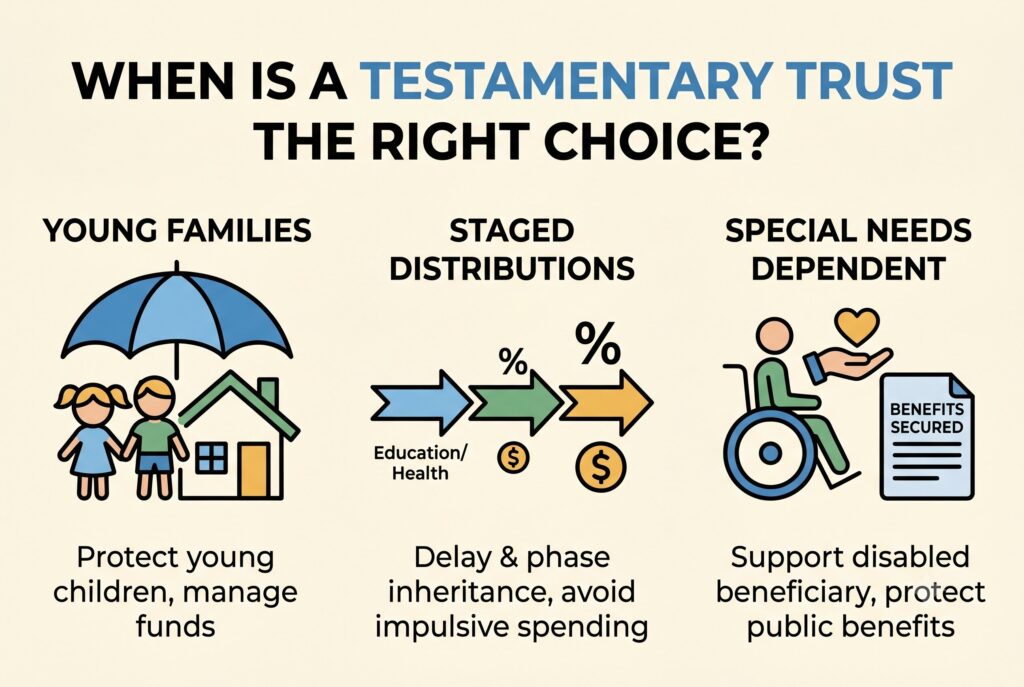

When Is a Testamentary Trust the Right Choice?

1. Young Families with Modest Assets

A testamentary trust can work well for parents with young children who want a safety net. If both parents die unexpectedly, the trust can prevent children from receiving money too early. The trustee can manage funds until the children reach responsible ages. This is often useful when most wealth is tied to life insurance, a home, savings, and retirement accounts.

2. Parents Who Want Staged Distributions

Some beneficiaries need structure. A testamentary trust lets you delay or stage inheritance. You can give the trustee discretion to pay for education and health needs first, then release larger portions later. This protects young adults from sudden wealth mistakes, impulsive spending, creditor issues, or pressure from others.

3. Planning for a Special Needs Dependent

A testamentary trust can also be drafted as a special needs trust. This allows inherited money to support a disabled beneficiary without automatically disrupting important public benefits such as Medicaid or SSI. The wording must be precise. If the trust gives the beneficiary direct control over assets, it may create benefit problems.

Key Rules to Know Before You Choose

- First, the trustee matters. This person may manage money for years, file tax returns, communicate with beneficiaries, keep records, and follow court rules. Choose someone responsible, calm, organized, and financially careful.

- Second, taxes can become an issue. Trusts may pay tax differently from individuals, and long term retained income can become expensive. If money will stay in the trust for many years, get tax advice before finalizing the plan.

- Third, coordinate beneficiary designations. Life insurance and retirement accounts don’t always pass through the will. If your trust plan depends on those assets, the beneficiary forms must match the estate plan.

Conclusion

A testamentary trust is best understood as a fallback structure, not a full lifetime asset protection system. For many families, it offers a practical and affordable way to protect children, manage inheritance, and provide ongoing support for loved ones after death. Understanding what is a testamentary trust also means understanding its limitations. Because it is created through a will, it must go through probate before it becomes active, which can lead to delays, public court filings, and, in some cases, ongoing court supervision.

If your estate is relatively simple and your primary goal is to create a safety net for minor children or other dependents, a testamentary trust may be all you need. However, if privacy, probate avoidance, incapacity planning, or greater control over taxes and asset management are important priorities, a living trust or another estate planning strategy may be a better fit. Ultimately, the right choice depends on your family’s circumstances, the complexity of your assets, and the level of guidance and protection your beneficiaries may need in the future.