& Cash)")

If you are turning 30 and wondering whether you are behind, you aren’t alone. The question how much money should I have saved by 30 is one of the most stressful personal finance questions because it feels like a scorecard for adulthood. But the truth is more practical, and less scary, than that.

A common benchmark says you should have about 1x your annual salary saved by age 30. If you earn $55,000 a year, the target would be around $55,000 across cash savings, retirement savings, and investment accounts. That doesn’t mean everyone will be there. Real-world data often shows a much wider gap: average savings by 30 may look higher because of high savers, while median savings by age is usually much lower and more realistic for the typical young adult. A good target is one year of salary saved, but a strong foundation matters more: an emergency fund, no toxic high-interest debt, and consistent retirement contributions.

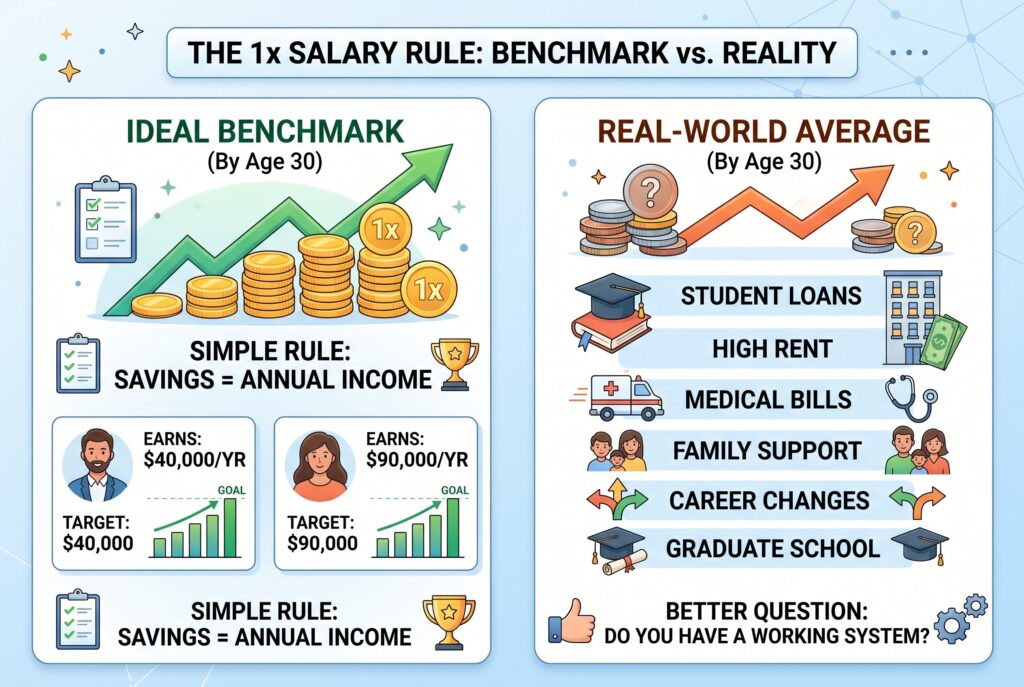

The 1x Salary Rule: Ideal Benchmark vs. Real-World Average

The 1x salary rule is simple: by age 30, aim to have savings equal to your annual income. It’s a useful savings benchmark age 30 because it adjusts to your lifestyle. Someone earning $40,000 would target $40,000. Someone earning $90,000 would target $90,000. But this benchmark is a guidepost, not a judgment. People reach 30 with very different realities: student loans, medical bills, high rent, family support obligations, career changes, or years spent in graduate school. If your money saved by 30 is lower than the ideal number, it doesn’t mean you failed. It means your next steps need to be intentional.

The better question isn’t only “how much is saved by 30?” It is: do you have a working system? Are you saving automatically? Are you paying down expensive debt? Are you building retirement savings before compound interest loses too much time?

The Bucket Strategy: Dividing Your Savings Cash vs. 401(k)

One mistake people make is treating all savings as the same. Cash in a savings account isn’t the same as money in a 401(k), IRA, or Roth IRA. Each has a different job.

Emergency Fund Savings

If you’re wondering how much you should have in savings, start with an emergency fund that covers three to six months of essential expenses. Keep this money in a safe, accessible account so it’s available when unexpected costs arise.

Short-Term Savings Goals

This bucket is for financial goals you plan to reach within the next few years, such as a car purchase, moving expenses, a wedding, travel, or a home down payment. Because you’ll need the money relatively soon, preserving capital is often more important than pursuing higher returns.

Retirement and Long-Term Investments

Your retirement bucket includes accounts such as a 401(k), IRA, or Roth IRA. These long-term investments are designed to grow over decades, allowing compound returns to play a major role in building future wealth and increasing your net worth. At 30, you don’t need every dollar sitting in cash. In fact, holding too much cash can slow long-term growth. A healthy plan balances emergency fund safety with long-term investing.

How Much Should I Have in My 401(k) at 30?

The question of how much should I have in my 401(k) at 30 depends on your salary, when you started working, and whether your employer offers a match. As a broad target, your total retirement savings by age 30 should be moving toward 1x your annual salary, especially if you started saving in your early 20s. If that feels impossible, start with the employer match. An employer match is one of the most powerful benefits available because it’s extra compensation. If your company matches 50% of contributions up to 6% of pay, try to contribute at least enough to get the full match.

A common retirement contribution rate is 15% of annual income, including employer match. If you can’t save 15% yet, start smaller. Even 5% or 8% can build momentum. Increase your contribution by 1% each time you get a raise. A 401(k) isn’t the only option. An IRA or Roth IRA can also help, especially if your workplace plan has high fees or limited investment choices. The main point is consistency. Retirement planning at 30 is about giving compounding decades to work.

Falling Short? 4 Steps to Catch Up by 30

If your savings by age 30 are below the benchmark, don’t panic. You can still build a strong financial life.

Eliminate High-Interest Debt First

High-interest debt can slow wealth building more than most investments can accelerate it. Prioritizing credit card balances and expensive loans often provides the fastest path to improving your financial position.

Automate Saving and Investing

The easiest way to build wealth is to make it automatic. Set up recurring contributions to savings accounts, retirement plans, and investment accounts so that saving happens before spending.

Prevent Lifestyle Inflation

As your income grows, resist the urge to increase your spending at the same pace. Directing a portion of every raise toward savings and investments can significantly accelerate long-term wealth creation.

Build Strong Financial Habits

Financial success is driven more by consistent behavior than by hitting a specific milestone. Saving regularly, living below your means, and investing over time often matter more than any single net worth target.

What Counts Toward Savings by 30?

Your age-30 savings can include emergency savings, retirement accounts, investment accounts, and cash set aside for major goals. But it shouldn’t include money you already need for next month’s rent or bills. Net worth is also useful here. Your net worth includes assets minus liabilities, so it captures savings, investments, home equity, debt, and loans. If your savings look low but you have paid off debt aggressively, your full financial picture may be stronger than it appears. That is why comparing only average savings by age can be misleading. A person with $10,000 in cash and no debt may be safer than someone with $30,000 in cash and $25,000 in credit card debt.

Conclusion

Turning 30 isn’t a deadline, and it’s certainly not a verdict on your financial future. Whether you’ve already reached major savings goals or feel like you’re still catching up, what matters most is the direction you’re moving. Building wealth comes from consistently saving, reducing debt, investing for the future, and making thoughtful financial choices year after year. Small actions repeated over time often have a greater impact than trying to reach a specific number by a certain age.

As your career and income grow, continue reviewing your financial plan regularly. Track your progress, adjust your goals when needed, and focus on creating a system that supports long-term success. Ultimately, the goal isn’t to match someone else’s net worth or retirement timeline. The goal is to build a financial foundation that gives you stability today and more choices tomorrow. Over time, that stability can grow into flexibility, confidence, and the freedom to live life on your own terms.